Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

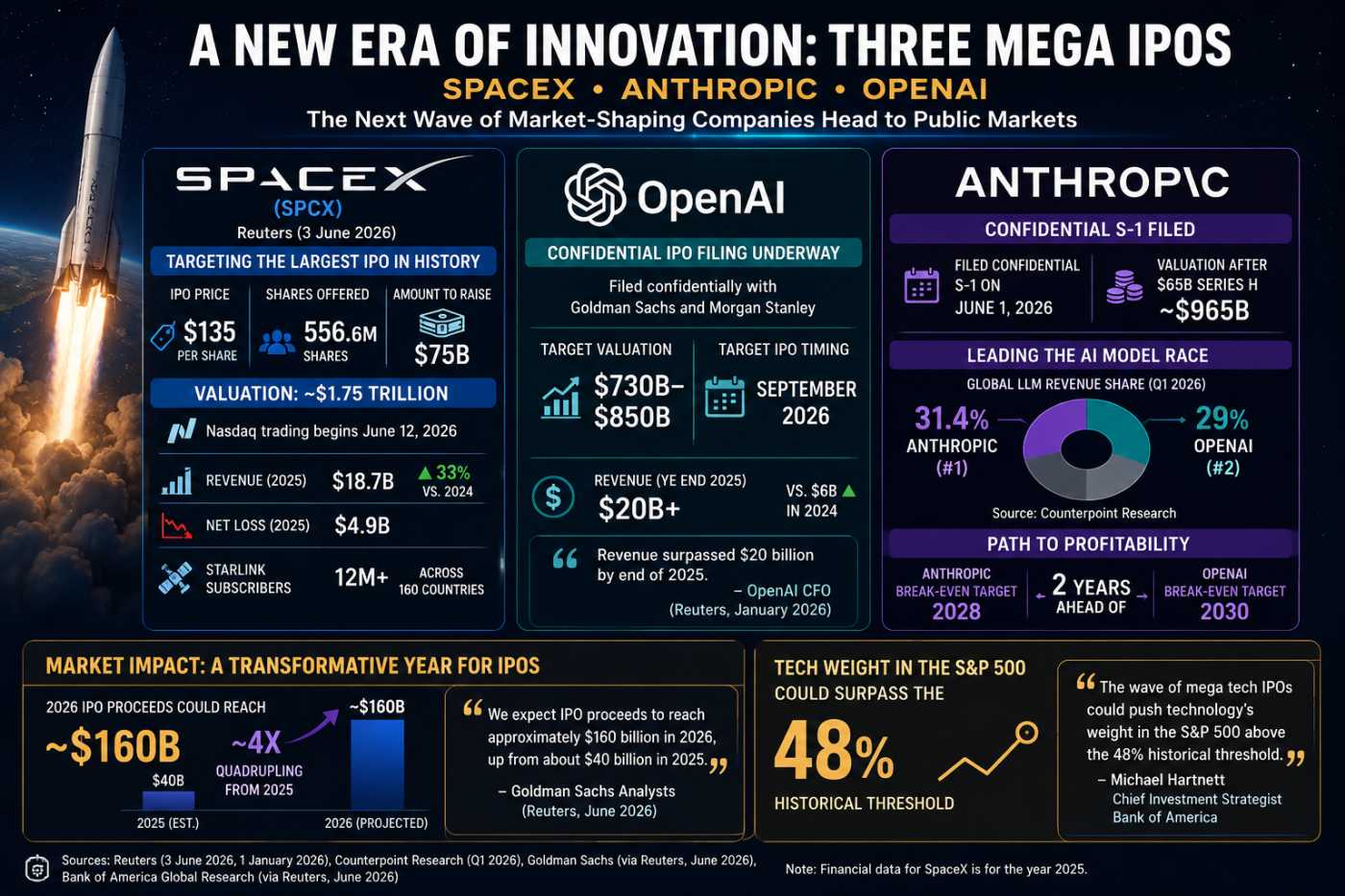

SpaceX IPO Spawned a New Speculation Machine

How SpaceX Gave Main Street a Seat at the IPO

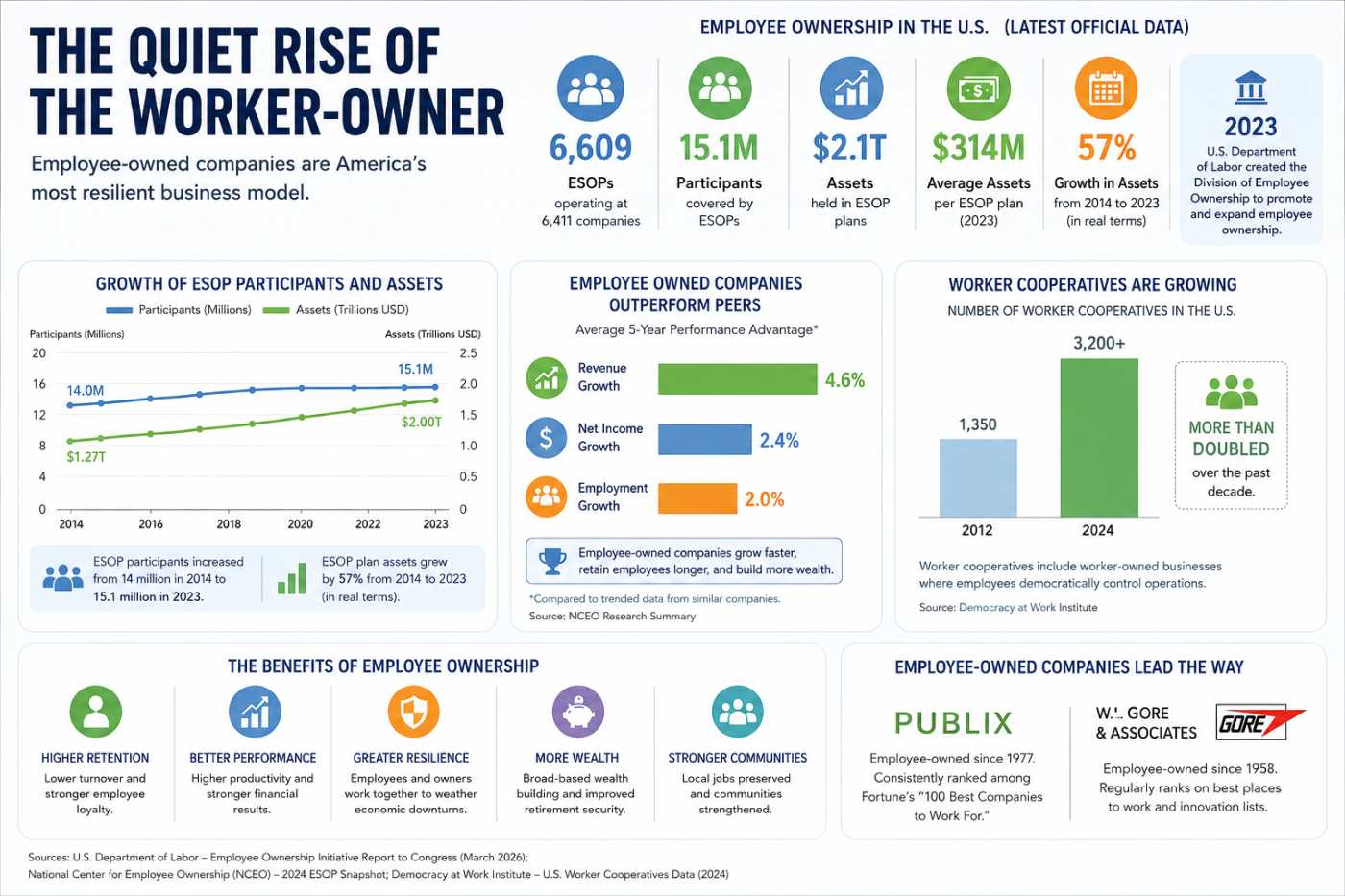

How Workers Became Capitalists

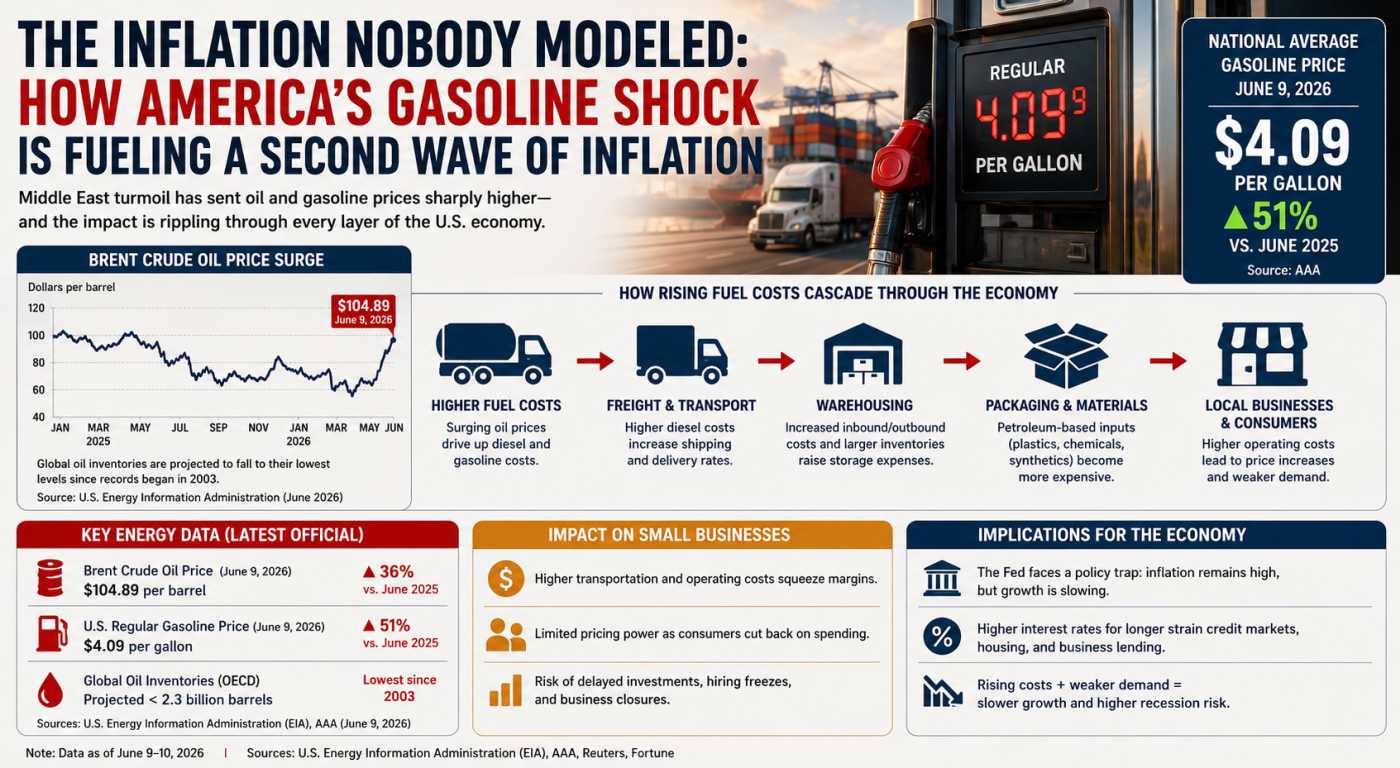

The Inflation Wave the Fed Can't Navigate

The Biggest IPO Year Ever: Can Markets Absorb It?

The Liquidity Trap Hidden Inside Leveraged ETFs

The Quiet Growth Story Nobody Is Stress-Testing

For most investors, leveraged exchange-traded funds (ETFs) remain a niche corner of the market: useful for traders seeking amplified exposure to stock indexes, sectors, commodities or individual stocks. Yet beneath that seemingly straightforward purpose lies a market-structure question that has attracted growing attention from academics, regulators and derivatives professionals.

The question is not whether leveraged ETFs are risky for their holders. That debate has largely been settled. Instead, the more important question is whether the rapid growth of leveraged ETFs is creating hidden liquidity dependencies between equity markets, futures markets, swaps markets and options markets that only become visible during periods of stress.

As of mid-2026, the broader ETF industry continues to expand at a remarkable pace. Citigroup estimated that U.S. ETF assets could reach $25 trillion by 2030, more than double the approximately $10.4 trillion recorded in early 2025. ETF inflows remain exceptionally strong, with hundreds of billions of dollars entering U.S.-domiciled funds annually. While leveraged ETFs represent only a fraction of the overall ETF universe, they have been among the fastest-growing and most innovative segments of the industry.

The recent launch wave surrounding SpaceX's June 2026 IPO highlighted the trend. Roughly two dozen SpaceX-focused ETFs were registered around the listing, many of them leveraged products designed to magnify daily returns. The speed with which leveraged products emerged around a newly public company illustrated how rapidly leverage has become embedded within modern ETF product development. Reuters and Axios both reported significant industry interest in these products immediately following the IPO.

The concern is not necessarily the size of any single leveraged ETF. Rather, it is the increasingly complex web of derivatives, hedging activity and liquidity transfers that these products create across markets.

Why Leveraged ETFs Are Different

Traditional index ETFs generally hold the securities they track. Leveraged ETFs operate differently.

To deliver two-times or three-times the daily return of an index, fund managers typically rely on futures contracts, total-return swaps, options and other derivatives. Because leverage ratios must be maintained daily, these funds frequently rebalance their exposures.

That daily rebalancing process is where the market-structure debate begins.

If a benchmark rises sharply during the trading day, a leveraged ETF often needs to increase exposure before the close in order to maintain its target leverage ratio. Conversely, if the benchmark falls sharply, the fund may need to reduce exposure. In both cases, the fund's trading direction is generally aligned with the market move.

This creates a feedback mechanism that differs from traditional investing. Rather than acting as a stabilizing force by buying weakness and selling strength, leveraged ETF rebalancing can require buying into rallies and selling into declines.

The magnitude of these flows varies considerably, but the mechanism itself is mechanical rather than discretionary.

What Academic Research Actually Found

Some of the most influential research on the topic came from Pauline Shum, Walid Hejazi, Edgar Haryanto and Arthur Rodier in their study, Intraday Share Price Volatility and Leveraged ETF Rebalancing, published in the Review of Finance.

The researchers examined market behavior surrounding the 2006-2011 period and found evidence that end-of-day volatility increased alongside leveraged ETF rebalancing demands.

They wrote that:

"End-of-day volatility was positively and statistically significantly correlated with the ratio of potential rebalancing trades to total trading volume."

Importantly, the authors also noted that the effects were largest during the most volatile trading days rather than during ordinary market conditions.

This distinction matters. Most market participants focus on average conditions. Financial crises, however, are driven by extreme conditions. If leveraged ETF flows become significant precisely when liquidity is scarce, their influence may be disproportionately important during market stress.

The authors additionally explored the possibility that predictable rebalancing flows could attract strategic traders seeking to position ahead of those transactions.

This introduces another layer of complexity: even if leveraged ETF flows themselves are manageable, market participants anticipating those flows could potentially amplify their impact.

The Counterargument Is More Nuanced Than Headlines Suggest

Not all research reaches the same conclusion.

In a widely cited study published in the Journal of Financial Markets, Ivan Ivanov and Stephen Lenkey argued that capital inflows and outflows substantially reduce actual rebalancing needs. Their research found that after accounting for investor flows, the impact of leveraged ETF rebalancing on volatility appeared economically insignificant, even during periods of stress.

Their findings challenge the simplistic narrative that leveraged ETFs automatically destabilize markets.

Instead, the evidence suggests a more nuanced reality. Leveraged ETF rebalancing may not consistently drive volatility on its own. However, under certain conditions involving concentrated positioning, declining liquidity and elevated uncertainty, the effects could become more pronounced.

This distinction is critical because it shifts the debate away from whether leveraged ETFs are inherently dangerous and toward understanding the specific circumstances under which they could contribute to market instability.

The Hidden Liquidity Transfer Problem

One of the least discussed aspects of leveraged ETFs is that they do not simply create leverage. They also create relationships between multiple markets.

A leveraged ETF tracking an equity index may depend on futures markets for exposure. Those futures markets depend on dealers and market makers for liquidity. Dealers often hedge using options or swaps. Banks providing swaps may hedge using futures or cash equities.

The result is an interconnected liquidity ecosystem.

During normal conditions, these linkages improve efficiency. During stressed conditions, they can become channels through which volatility spreads.

A 2026 study by Ryuki Hayase, Takanobu Mizuta and Isao Yagi examined arbitrage relationships between leveraged ETFs and futures markets during simulated market crashes. Their findings suggested that arbitrage activity can effectively transfer liquidity demands from one market to another.

In practical terms, stress originating in a leveraged ETF market can draw liquidity from futures markets. Likewise, disruptions in futures markets can spill into leveraged ETF markets through arbitrage mechanisms.

The significance of this observation lies not in proving that leveraged ETFs cause crashes. Rather, it suggests that leveraged products may alter how liquidity is distributed during crises.

Liquidity may not disappear entirely. Instead, it may migrate from one market to another, leaving unexpected gaps precisely where investors expect depth to exist.

The Derivatives Market Connection

Another underappreciated issue involves derivatives market capacity.

Many leveraged ETFs obtain exposure through total-return swaps negotiated with large banks. Those banks subsequently hedge the resulting exposures.

As leveraged ETF assets expand, the demand for derivatives-based exposure also expands.

This creates concentration risks that are rarely visible to retail investors because much of the activity occurs in institutional markets.

The concern is not simply leverage. The concern is whether increasingly large amounts of systematic exposure are being routed through a relatively concentrated group of dealers, market makers and swap counterparties.

Market history shows that liquidity providers can reduce risk-taking rapidly during periods of uncertainty. When that happens, liquidity that appeared abundant under normal conditions can become unexpectedly scarce.

If leveraged ETFs require significant rebalancing at the same time that dealers are reducing risk exposure, market depth can deteriorate quickly.

Options Markets Are Becoming Part of the Story

Recent research by Andrea Barbon, Heiner Beckmeyer, Andrea Buraschi and Mathis Moerke examined interactions between leveraged ETF rebalancing and options-related hedging flows.

Their work found that leveraged ETF rebalancing and options delta-hedging represent distinct yet economically significant sources of liquidity demand.

What makes this important is the timing.

Both activities tend to intensify during periods of elevated volatility. Both can generate predictable end-of-day trading flows. Both rely heavily on intermediaries willing to absorb risk.

As options volumes continue reaching record levels across U.S. equity markets, the interaction between options hedging and leveraged ETF rebalancing is becoming increasingly relevant.

The market may not be facing a single source of instability. Instead, it may be accumulating multiple sources of predictable liquidity demand that become synchronized during periods of stress.

Why Regulators Keep Returning to the Issue

The SEC's recurring concerns about higher-leverage products provide another clue.

In late 2025, SEC officials publicly questioned whether proposed 3x and 5x leveraged ETF structures would comply with Rule 18f-4, the agency's derivatives risk-management framework.

According to Reuters reporting, some proposed products appeared to exceed leverage thresholds envisioned under the rule.

The concern extends beyond investor protection.

Leveraged ETFs have experienced a history of severe value destruction. Reuters reported that more than half of leveraged ETFs launched more than three years earlier had already closed, while roughly 17% lost over 98% of their value.

Those statistics alone do not imply systemic risk. However, they highlight how aggressively leveraged structures can behave during adverse market conditions.

Regulators appear increasingly focused on whether ever-higher leverage ratios could create unintended consequences for market functioning, particularly when combined with growing retail participation and expanding derivatives exposures.

The Fragility Beneath the Calm

Perhaps the most important insight from the leveraged ETF debate is that systemic fragility rarely emerges from the largest or most obvious source.

The U.S. financial system today is far larger, more liquid and more diversified than it was during previous market crises. Yet modern markets are also increasingly interconnected through derivatives, algorithmic trading and passive investment structures.

Leveraged ETFs sit at the intersection of all three trends.

Academic evidence does not support the simplistic claim that leveraged ETFs inevitably cause market crashes. Several studies suggest their impact may be modest under normal circumstances. However, other research consistently finds that their influence becomes more noticeable during periods of extreme volatility, particularly when rebalancing demands collide with declining liquidity.

The most underreported risk may therefore be neither leverage itself nor volatility decay. It may be the growing dependence on continuous liquidity across futures, swaps and options markets. As leveraged ETF assets continue expanding, those markets become increasingly intertwined.

For years, financial stability discussions have focused on banks, hedge funds and private credit. Meanwhile, leveraged ETFs have quietly become a laboratory for testing how modern markets absorb predictable, rules-based trading flows.

The next major market selloff may not reveal that leveraged ETFs caused the turmoil. It may instead reveal something more subtle: that they helped move stress through the financial system faster than many participants expected.

If you have enjoyed reading, spread the word:

The Jobs Report That Crashed the Rally

The Fed Study Revealing Tomorrow's Investment Themes

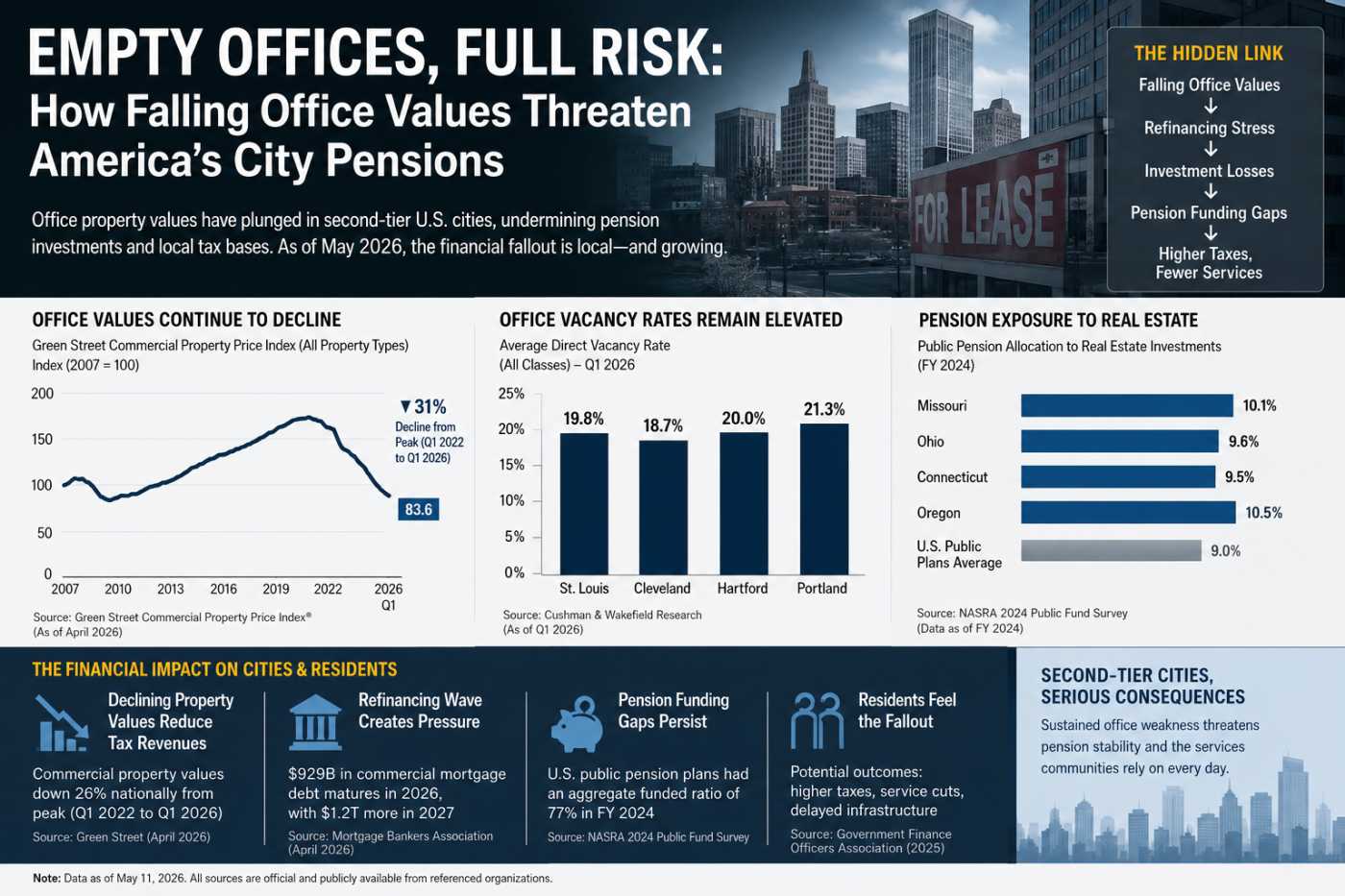

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity