Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

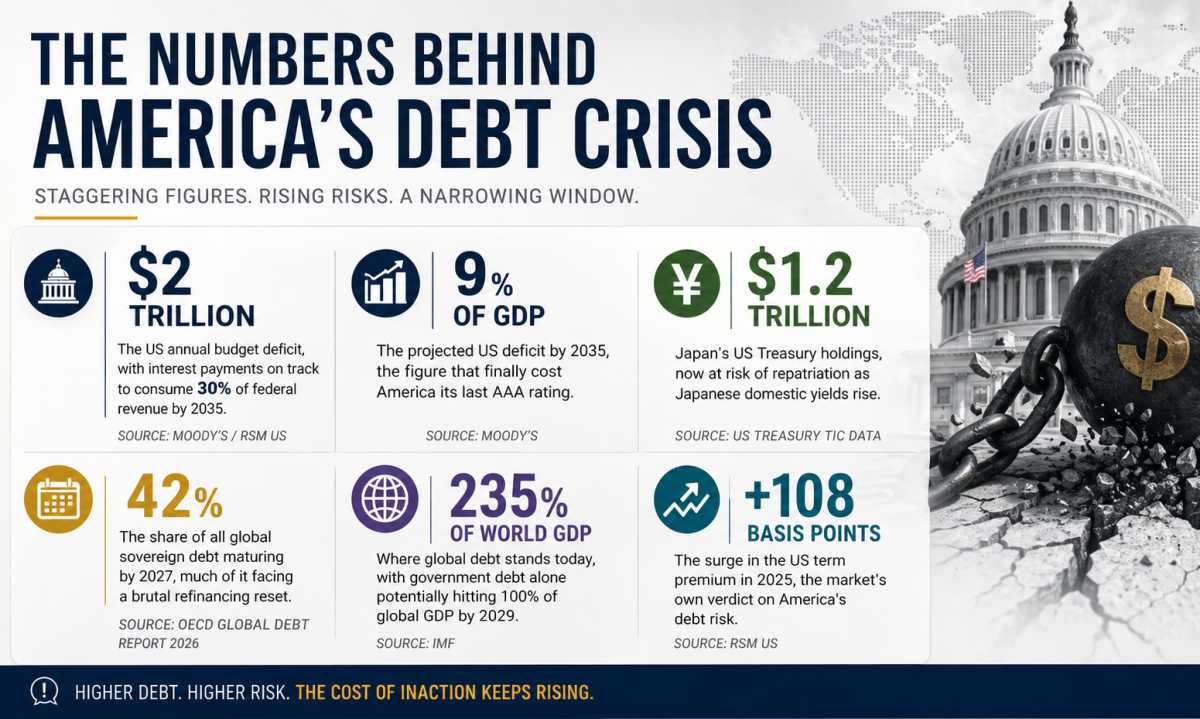

The Fed Study Revealing Tomorrow's Investment Themes

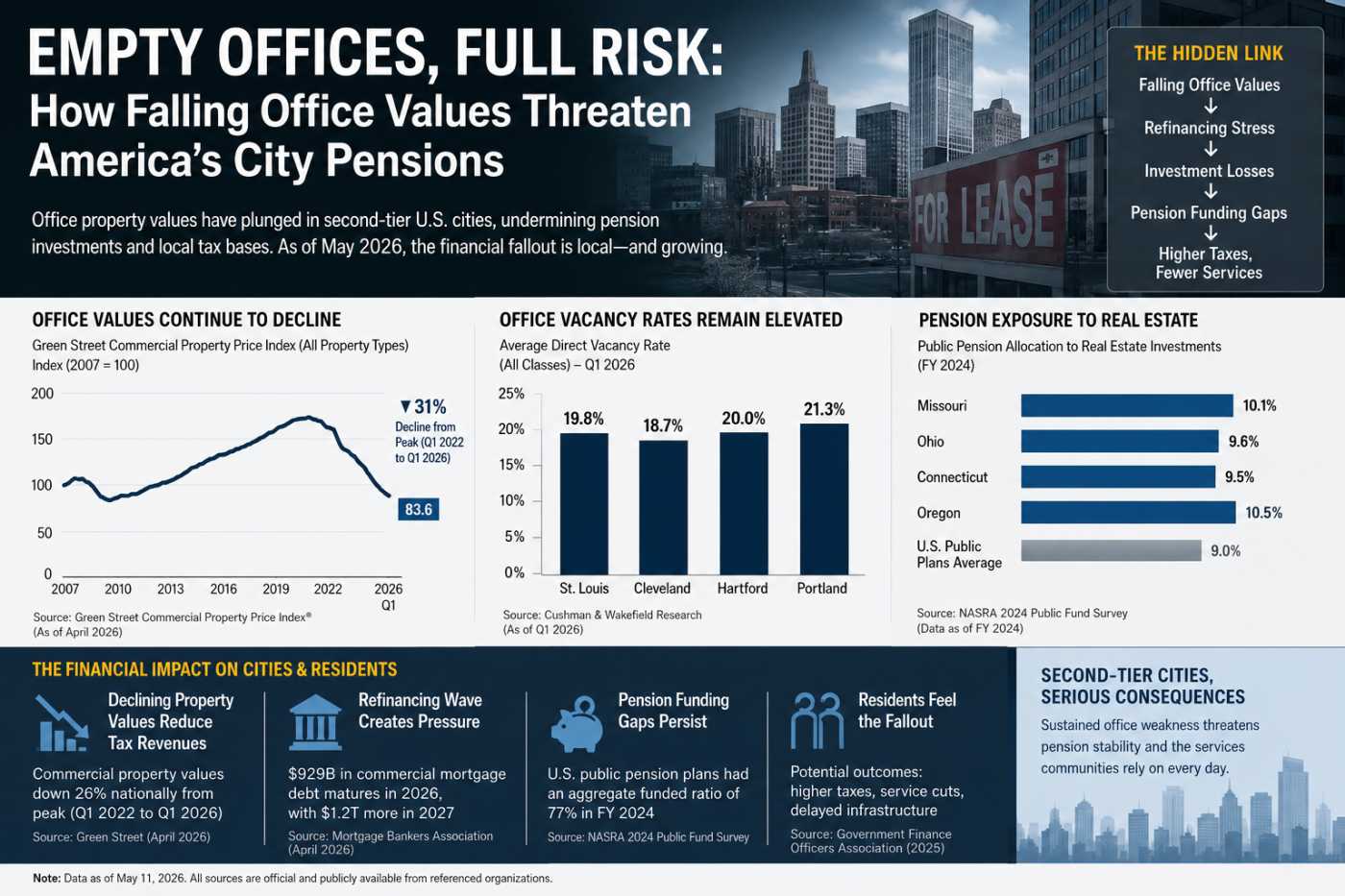

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

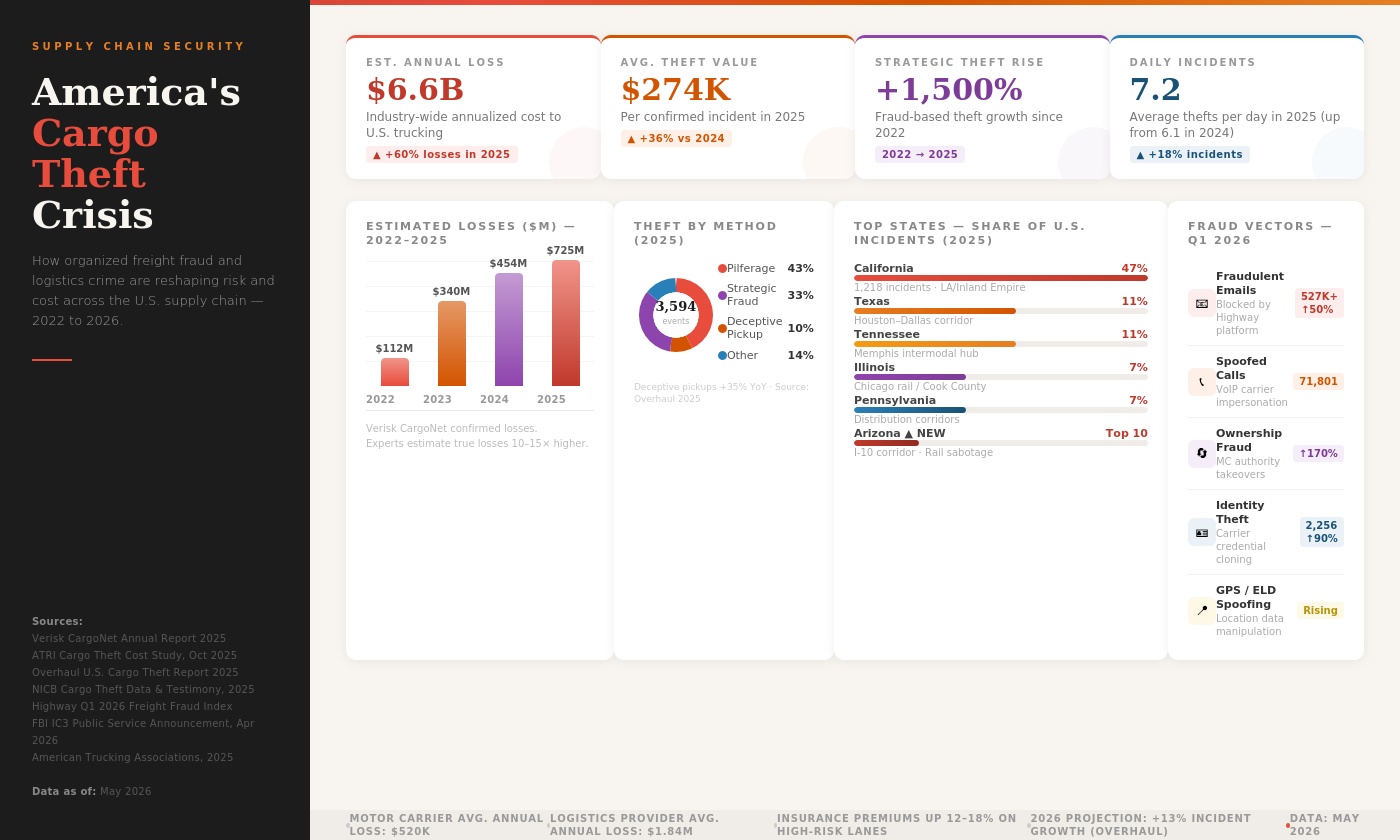

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

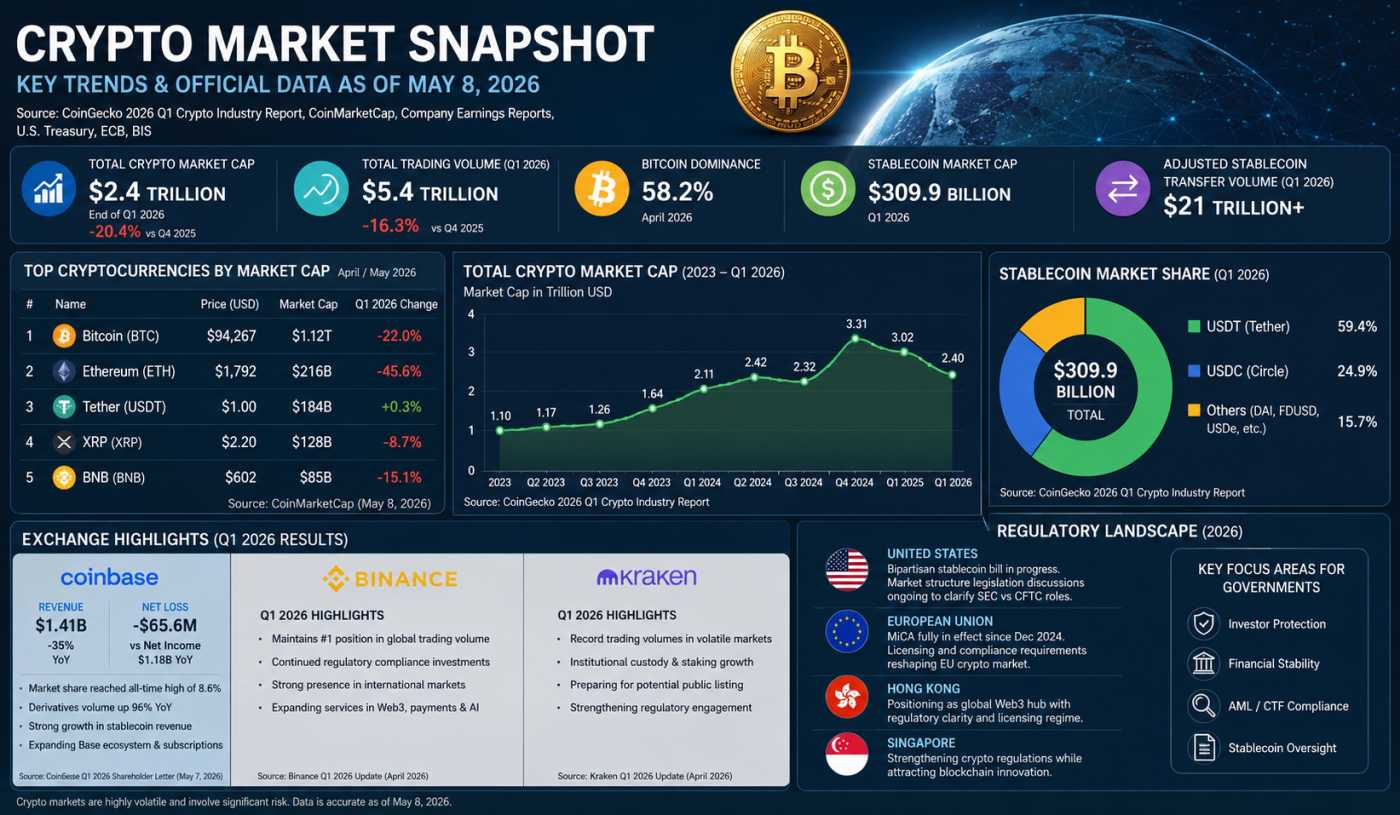

Crypto’s $2.4T Reality Check in 2026

The Jobs Report That Crashed the Rally

For decades, investors operated under a simple assumption: strong economic data was good for financial markets. Robust job growth signaled rising incomes, healthy consumer spending, stronger corporate earnings, and a resilient economy. Wall Street and Main Street generally moved in the same direction.

That relationship appears increasingly inverted in 2026.

When the U.S. Labor Department released its May employment report on June 5, the numbers initially looked like a reason for celebration. Nonfarm payrolls increased by 139,000 jobs, comfortably above many forecasts. The unemployment rate held steady at 4.2%, while labor market conditions remained considerably stronger than economists had anticipated at the start of the year.

Yet instead of rallying, markets sold off. Treasury yields jumped. Rate-cut expectations were pushed further into the future. High-growth technology stocks came under pressure. Several of the market's most richly valued artificial intelligence beneficiaries experienced notable declines as investors reassessed the interest-rate outlook.

The reaction revealed one of the most important and least discussed dynamics shaping financial markets in 2026: a healthy economy has become a threat to asset prices because much of Wall Street's valuation framework now depends on future monetary easing. Strong employment data is no longer merely an economic indicator. It has become a test of whether the Federal Reserve can justify delivering the lower interest rates upon which many of today's elevated equity valuations increasingly depend.

The Jobs Report That Markets Didn't Want

The May employment report delivered a clear message: the labor market remains resilient despite elevated borrowing costs and slowing economic growth.

According to the U.S. Bureau of Labor Statistics, nonfarm payroll employment increased by 139,000 in May while unemployment remained unchanged at 4.2%. Healthcare, leisure and hospitality, and social assistance sectors continued to add jobs, offsetting weakness elsewhere.

The report surprised investors because expectations had gradually shifted toward labor market cooling. For months, financial markets had been pricing in the possibility that slowing employment growth would eventually give the Federal Reserve sufficient confidence to begin cutting rates.

Instead, the labor market once again demonstrated its durability.

The market response was immediate. Treasury yields rose sharply as traders reduced expectations for near-term monetary easing. Higher bond yields simultaneously increased financing costs and reduced the relative attractiveness of future corporate earnings, particularly for high-growth technology companies whose valuations depend heavily on projected profits many years into the future.

As Reuters reported following the employment release, investors viewed the stronger-than-expected payroll figures as evidence that the Federal Reserve would likely maintain restrictive monetary policy for longer than previously anticipated. Reuters' coverage noted that Treasury yields rose while expectations for 2026 rate cuts diminished following the report.

Under ordinary circumstances, strong employment data would support corporate earnings forecasts. In the current market environment, however, the interest-rate implications appear to matter more than the growth implications.

The AI Valuation Machine Runs on Discount Rates

The unusual reaction becomes easier to understand when examining the structure of today's stock market.

The largest contributors to U.S. equity gains over the past two years have overwhelmingly been technology and artificial intelligence-related companies. Investors have poured enormous amounts of capital into businesses expected to benefit from AI infrastructure spending, semiconductor demand, cloud computing expansion, and enterprise software adoption.

Many of these companies possess extraordinary growth prospects. However, they also share another characteristic: a substantial portion of their expected value lies in profits that have not yet materialized.

Modern equity valuation models estimate what future cash flows are worth today. The interest rate used in those calculations commonly known as the discount rate plays a critical role.

When interest rates fall, future earnings become more valuable in present-value terms. When rates remain elevated, those future profits become less valuable. The effect is particularly powerful for companies whose expected earnings are concentrated years or even decades into the future.

This is one reason technology stocks often respond dramatically to changes in bond yields.

The phenomenon has become especially pronounced during the AI investment boom. Investors are effectively paying today for anticipated earnings streams that may not fully emerge until the late 2020s or early 2030s. Such valuations become highly sensitive to assumptions regarding future interest rates.

In practical terms, the market's enthusiasm for AI has become partially intertwined with expectations that the Federal Reserve would eventually reduce borrowing costs. Strong employment data threatens that assumption.

Wall Street's Growing Dependence on Rate Cuts

The market's reaction also reflects a broader structural shift that has occurred since the Global Financial Crisis.

For much of the period between 2009 and 2021, investors operated in an environment characterized by exceptionally low interest rates. Cheap capital encouraged risk-taking, boosted equity valuations, and rewarded growth-oriented investment strategies.

The rapid rate increases implemented by the Federal Reserve beginning in 2022 represented a dramatic departure from that regime. Yet despite those increases, many investors continued to assume that rates would eventually return toward historically lower levels.

That expectation has become deeply embedded in market pricing.

According to CME FedWatch data and various market-implied rate forecasts, investors spent much of late 2025 and early 2026 expecting multiple rate reductions during the year. Those expectations supported risk assets even as inflation remained above the Federal Reserve's 2% target.

The May jobs report challenged that narrative.

If labor market conditions remain strong, wage growth remains stable, and consumer spending continues expanding, Federal Reserve officials have little incentive to rush toward monetary easing. The stronger the economy appears, the weaker the argument for rate cuts becomes.

This creates a paradox that would have seemed unusual in previous economic cycles: positive economic data can generate negative market reactions because it reduces the probability of monetary stimulus.

The Inflation Problem Has Not Disappeared

Another factor behind the selloff is that investors are increasingly concerned about inflation's persistence.

While inflation has declined significantly from the peaks reached during 2022 and 2023, it remains above the Federal Reserve's long-term target. Recent energy market disruptions tied to tensions in the Middle East have introduced additional uncertainty regarding future price pressures.

Federal Reserve officials have repeatedly emphasized the need for greater confidence that inflation is moving sustainably toward 2% before reducing rates.

Speaking after recent policy meetings, Federal Reserve Chair Jerome Powell has consistently highlighted the importance of incoming economic data. Strong employment growth complicates the inflation outlook because robust labor markets can support consumer spending and maintain pricing power throughout the economy.

The Reuters survey of economists published on June 9 found growing skepticism that meaningful rate cuts would occur in 2026. Many respondents cited persistent inflation pressures and unexpectedly strong economic data as reasons for expecting rates to remain unchanged longer than previously forecast.

In effect, the jobs report reinforced fears that inflation may be stabilizing above target rather than continuing its downward trajectory.

The Labor Market's Hidden Signal

An overlooked aspect of the May report is what it suggests about underlying economic demand.

Businesses generally hire when they expect sufficient future demand for their products and services. Sustained employment growth therefore indicates that many employers remain relatively confident about economic conditions despite higher financing costs.

That confidence may appear encouraging, but it also suggests that restrictive monetary policy has not slowed economic activity as much as policymakers expected.

For investors hoping for rapid rate cuts, labor market resilience can therefore be interpreted as evidence that monetary easing is unnecessary.

This helps explain why good news became bad news.

The jobs report did not simply reveal employment strength. It suggested that the economy remains capable of functioning under current interest-rate conditions, reducing pressure on the Federal Reserve to provide relief.

Why Technology Stocks React More Than Other Sectors

The market reaction was not evenly distributed.

Interest-rate-sensitive growth stocks experienced significantly greater volatility than many defensive sectors. Utilities, consumer staples, and certain healthcare companies generally proved more resilient than highly valued technology firms.

This divergence highlights the growing concentration risk within modern equity markets.

A relatively small number of AI-linked companies have accounted for an outsized share of major index performance during recent years. Because these firms command substantial weightings in benchmarks such as the S&P 500 and Nasdaq, changes in their valuations can significantly influence overall market performance.

Goldman Sachs Chief U.S. Equity Strategist David Kostin noted earlier in 2026 that market concentration remains unusually elevated compared with historical norms. Investors have increasingly focused on companies perceived as primary beneficiaries of AI adoption.

When interest-rate expectations shift, those same companies often experience amplified reactions because their valuations incorporate aggressive long-term growth assumptions.

The stronger jobs report therefore triggered a chain reaction: stronger employment reduced rate-cut expectations, higher yields increased discount rates, and higher discount rates reduced the present value of future AI-driven earnings streams.

What initially appeared to be a labor market story quickly became a valuation story.

The Credit Market Is Now Driving Equity Markets

One of the least appreciated developments of 2026 is the growing influence of bond markets over equity markets.

Traditionally, investors often viewed stock markets as primarily driven by corporate earnings and economic growth. Increasingly, however, movements in Treasury yields have become the dominant variable influencing risk assets.

This shift reflects the extraordinary valuation levels reached in portions of the market. When valuations are elevated, small changes in discount-rate assumptions can have outsized effects on asset prices.

Following the May employment report, the rise in Treasury yields became arguably more important than the payroll figure itself. Investors immediately recalculated expected Federal Reserve policy paths, producing repricing across equities, bonds, currencies, and credit markets.

The reaction demonstrated how interconnected modern financial markets have become.

A stronger labor market increased bond yields. Higher bond yields pressured technology valuations. Falling technology shares weakened broader indexes. The resulting market decline occurred despite evidence that the underlying economy remained relatively healthy.

The Emerging Risk for Investors and Policymakers

The unusual market response highlights a deeper tension developing between economic fundamentals and financial market expectations.

For much of 2025 and early 2026, investors became increasingly reliant on the assumption that lower rates would support elevated asset prices. The May jobs report challenged that assumption by demonstrating that the economy may not be weakening fast enough to justify policy easing.

As Fortune observed in its analysis of the employment data, stronger labor market conditions can paradoxically unsettle investors because they delay the monetary relief many market participants have come to expect. In discussing the employment report, the publication quoted market analysts who emphasized that strong data may prolong the Federal Reserve's higher-for-longer stance. Fortune's analysis highlighted the increasingly counterintuitive relationship between economic strength and market sentiment.

Perhaps the most important takeaway from the selloff is not that investors suddenly became pessimistic about the economy. Rather, investors became concerned that the economy remains too healthy.

That distinction may sound absurd, but it captures the reality of modern financial markets. After years of low rates, abundant liquidity, and valuation expansion, many asset prices now depend as much on future monetary policy as they do on current economic performance.

The stronger-than-expected May jobs report exposed that dependence. In doing so, it revealed why a healthy labor market can now threaten financial markets even as it supports workers, businesses, and economic activity. The market's reaction was not a rejection of economic strength. It was a reminder that Wall Street's expectations have become deeply tied to the prospect of future rate cuts and that every strong jobs report pushes that prospect a little further away.

If you have enjoyed reading, spread the word:

The Machines That Ate the Grid: Five Centuries of Power Hunger

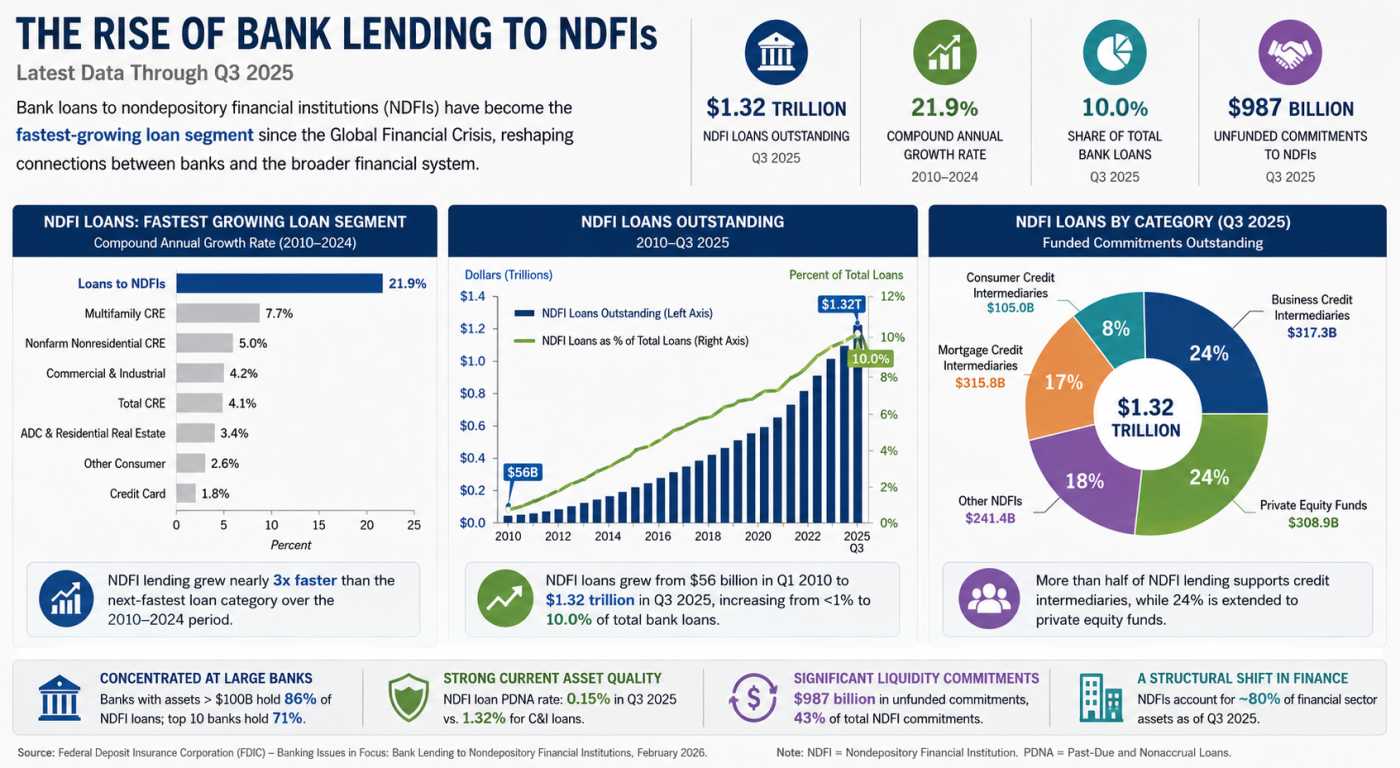

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America