Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

The Jobs Report That Crashed the Rally

The Fed Study Revealing Tomorrow's Investment Themes

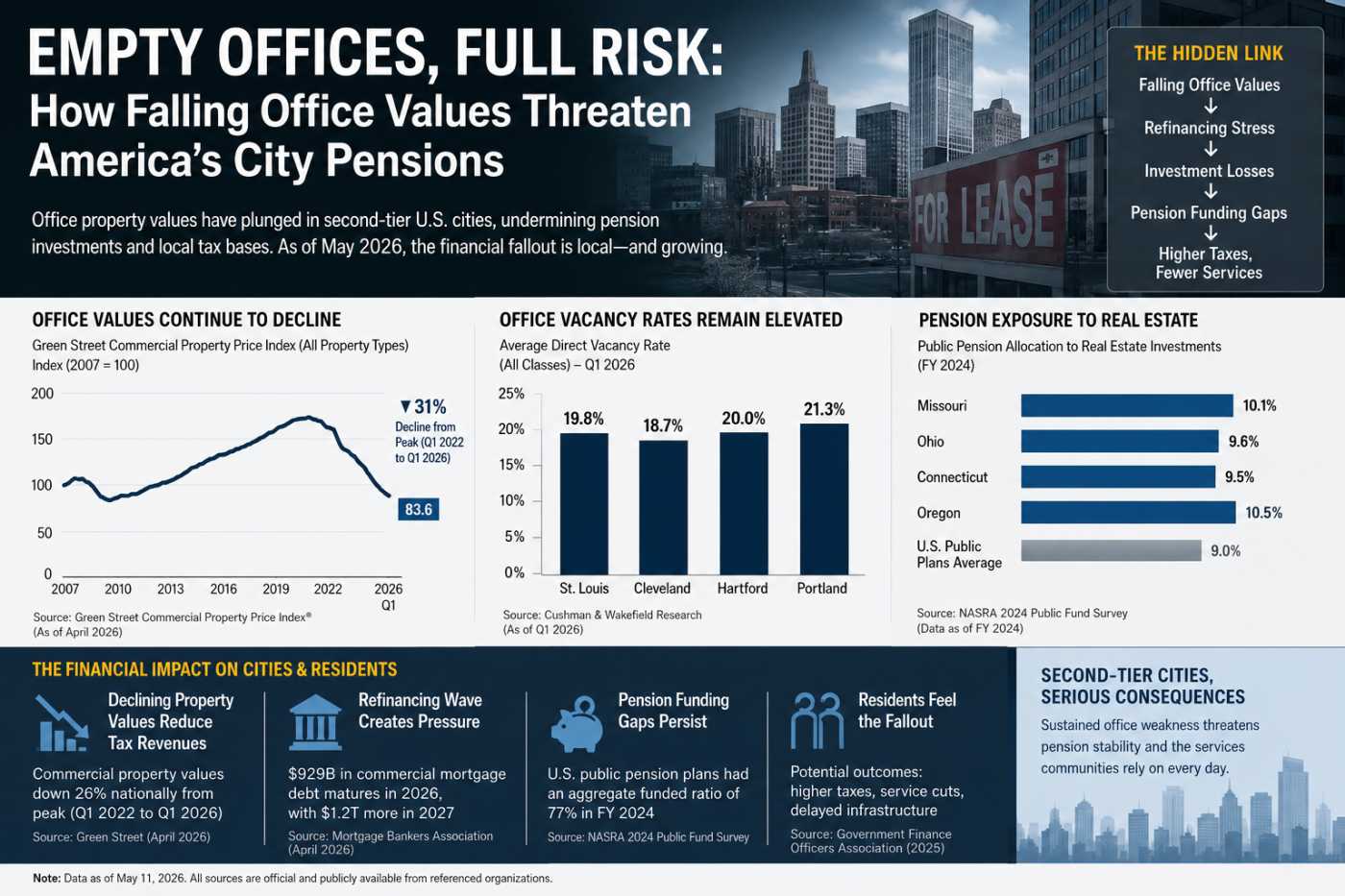

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

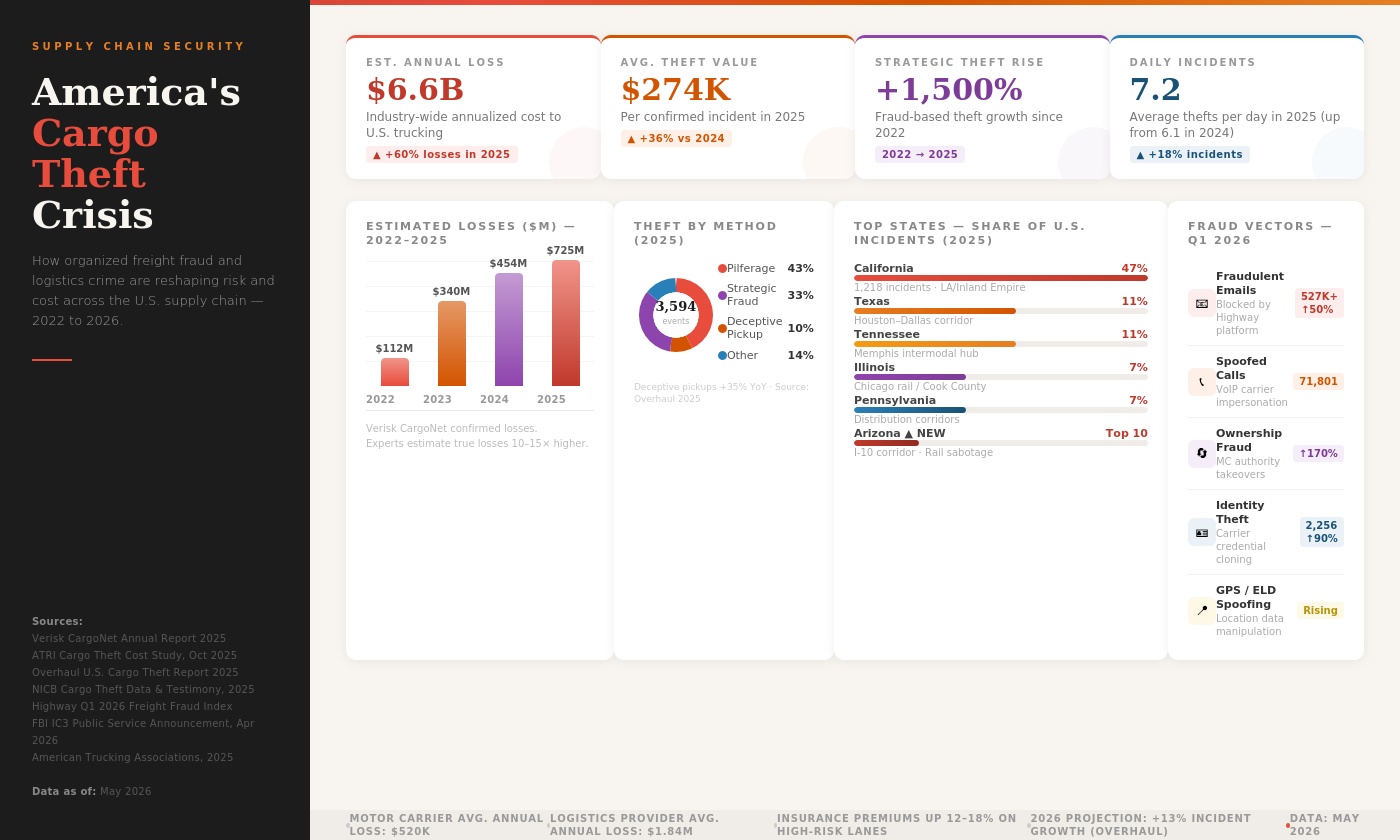

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

The Biggest IPO Year Ever: Can Markets Absorb It?

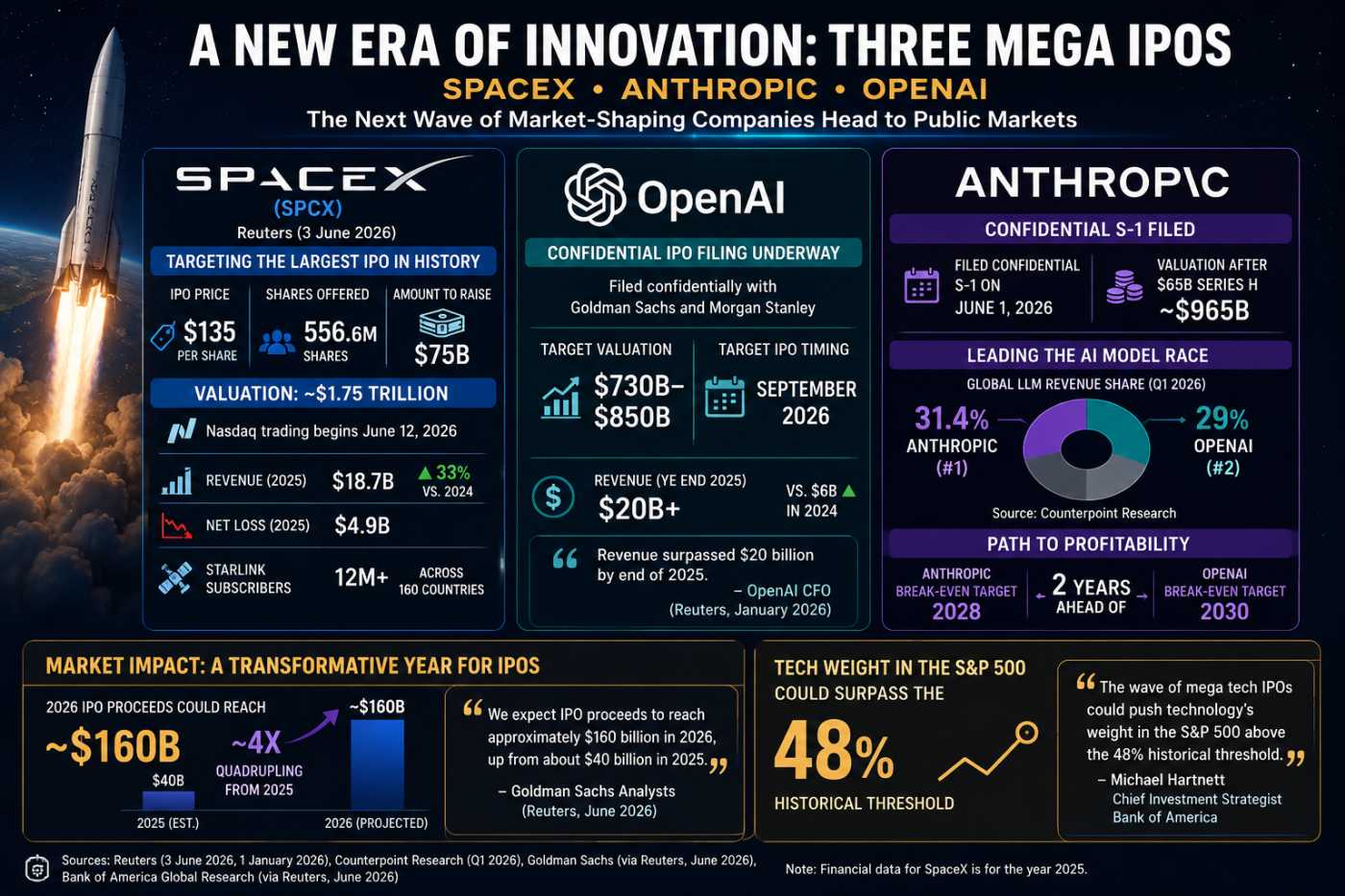

The Year Markets Changed Forever: SpaceX, OpenAI, and Anthropic Go Public

In the annals of financial history, 2026 is shaping up to be the year when three of the most consequential private companies ever created SpaceX, OpenAI, and Anthropic simultaneously converge on public markets. Together, they represent a combined targeted valuation of nearly $3.7 trillion and are collectively expected to raise well over $200 billion in fresh capital. No IPO window in history has ever concentrated this much transformative technology, narrative ambition, and outright financial risk into a single calendar year. For investors, market watchers, and the broader technology ecosystem, the implications are profound and far from settled.

SpaceX: The Largest IPO in History, Already Priced and Ready

Of the three listings, SpaceX's is the most immediately concrete. According to Reuters (3 June 2026), SpaceX is targeting an IPO price of $135 per share for an offering of 556.6 million shares, aiming to raise approximately $75 billion at a valuation of roughly $1.75–$1.77 trillion the largest initial public offering in stock market history. Trading is expected to begin on the Nasdaq on June 12, 2026, under the ticker SPCX. The company confidentially filed its S-1 with the SEC on April 1, 2026, publicly circulated the prospectus on May 20, and launched its roadshow on June 4 ahead of earlier estimates, driven by a faster-than-expected SEC review.

The financial picture SpaceX disclosed is a study in contrasts. Revenue climbed 33% year-over-year to $18.67 billion in 2025, but the company simultaneously recorded a $4.94 billion GAAP net loss a reversal from roughly $791 million in profit in 2024. The swing is directly attributable to SpaceX's February 2026 all-stock acquisition of Elon Musk's xAI, which added a new AI segment to its financials along with significant integration costs. Yet buried within those numbers is a compelling cash engine: Starlink, the satellite broadband division, generated $11.4 billion in 2025 revenue with approximately $4.4 billion in operating profit, representing roughly 60% of total company revenue. By Q1 2026, connectivity revenue had reached $3.26 billion, accounting for about 69% of total company revenue of $4.69 billion for the quarter.

The strengths are formidable. SpaceX controls more than 80% of U.S. rocket launches and operates the world's largest satellite constellation with over 12 million Starlink subscribers across 160 countries. Starlink's subscriber base roughly doubled year-over-year by March 2026, generating high-margin recurring revenue that public markets are willing to value generously. The acquisition of xAI adds an artificial intelligence narrative layer that, for better or worse, broadens the company's addressable market story.

The weaknesses are equally real. At $1.77 trillion and approximately 94.7 times annual sales, the pricing is extraordinarily demanding. The S-1 includes a 38-page risk-factor section. Elon Musk retains approximately 79% voting control, meaning public shareholders have almost no governance voice. A 366-day insider lockup means significant post-IPO supply pressure will arrive in mid-2027. The Starship program SpaceX's next-generation heavy-lift rocket that spent nearly $3 billion in R&D in 2025 alone has yet to reach regular commercial cadence, and whether it does so by 2028 is arguably the most consequential variable for the long-term investment case. One notable structural move: Nasdaq loosened its rules to allow SpaceX to join the Nasdaq-100 faster than the standard eligibility timeline would permit, a concession that underscores both the company's outsized importance and the index's competitive interest in landing the listing.

SpaceX CFO Bret Johnsen has emphasized an unusual retail-investor strategy. Musk reportedly wants to reserve up to 30% of the offering for retail investors three to six times the industry norm of 5–10% framing it as a reward to long-term supporters while simultaneously broadening the demand base for what is an enormous float to absorb.

OpenAI: A $1 Trillion Bet on ChatGPT's Enterprise Dominance

OpenAI, the company behind ChatGPT, has confidentially filed for an IPO with Goldman Sachs and Morgan Stanley as lead underwriters, alongside JPMorgan Chase. The filing sets up a potential public debut between September and November 2026, targeting a valuation of $730 billion to $850 billion with some scenarios projecting above $1 trillion if market conditions permit. The company plans to raise at least $60 billion in the offering, which would independently rank among the largest IPOs ever attempted.

OpenAI's revenue growth has been nothing short of extraordinary. The company's CFO Sarah Friar confirmed that annualised revenue surpassed $20 billion by the end of 2025, up from roughly $6 billion in 2024 and just $2 billion at the close of 2023. Enterprise adoption, paid ChatGPT subscriptions, and API usage are the three pillars driving this growth. OpenAI also serves as the operational lead for Stargate, a $500 billion joint venture targeting 10 gigawatts of AI data centre capacity across the United States and internationally by 2029 a commitment that both validates the capital intensity of its ambitions and locks in significant future infrastructure costs.

The company's structural history is more complex than its rivals. Founded in 2015 as a non-profit research lab, OpenAI has since restructured into a for-profit public benefit corporation, with the original non-profit foundation retaining a 26% equity stake. Microsoft, which has invested approximately $13 billion, holds roughly 27% of the company. SoftBank, Thrive Capital, and Abu Dhabi's MGX are also major shareholders. This ownership structure, while less concentrated than SpaceX's, still leaves meaningful governance questions for public investors. An additional legal overhang from Elon Musk's lawsuit alleging OpenAI had drifted from its founding mission was largely resolved in May 2026 when a jury verdict dismissed all claims under California's statute of limitations, reducing one significant uncertainty ahead of the listing.

OpenAI's central strength is brand and scale: ChatGPT had approximately 900 million monthly active users as of mid-2026, dwarfing every competitor in consumer AI reach. The challenge is profitability. Despite its revenue growth, OpenAI is operating at a loss, with its own internal timeline reportedly targeting profitability by 2030 a four-year runway that public markets will need to fund. The $20 billion revenue base, while impressive, is growing within a fiercely competitive landscape where both Anthropic and Google DeepMind are closing ground rapidly. Whether OpenAI's disclosed revenue and margin structure will support valuations in the $730 billion to $1 trillion range when the SEC registration statement becomes fully public is a question analysts and institutional investors are actively debating.

Anthropic: The Safety-First Challenger With the Fastest Revenue Ramp

Anthropic occupies a distinctly different position in this IPO race. The company confidentially filed its S-1 with the SEC on June 1, 2026, following a $65 billion Series H funding round that lifted its pre-IPO valuation to approximately $965 billion putting a debut above the $1 trillion mark within reach if markets cooperate. TradingView's data indicates Anthropic's IPO is currently planned for October 23, 2026, and the company has retained Wilson Sonsini as legal counsel with Goldman Sachs and JPMorgan reportedly advising on the offering.

The revenue trajectory is the most dramatic of the three. Anthropic's annualised revenue run rate sat at roughly $9 billion at the end of 2025. By February 2026, the company's Series G announcement led by GIC and Coatue, with participation from Accel, BlackRock-affiliated funds, Fidelity, General Catalyst, Goldman Sachs Alternatives, JPMorganChase, Lightspeed, Menlo Ventures, Morgan Stanley Investment Management, QIA, Sequoia, and Temasek disclosed a $14 billion run rate. By April 2026, that figure had surpassed $30 billion. By May 2026, CEO Dario Amodei himself described the trajectory as "crazy." A May 2026 compute agreement with SpaceX gives Anthropic access to over 300 megawatts of capacity and more than 220,000 NVIDIA GPUs, directly addressing one of the key constraints on AI model scaling.

According to data from Counterpoint Research, Anthropic led global large language model revenue share in Q1 2026 at 31.4%, narrowly ahead of OpenAI at 29% a data point that, if sustained, fundamentally reframes the competitive narrative. Approximately 80% of Anthropic's revenue comes from enterprise clients, giving it a qualitatively different and arguably more durable customer mix than consumer-oriented competitors. The company is backed by Amazon, which has deployed $13 billion in equity to date, and Alphabet, which holds a 14% equity stake contractually capped at 15%. According to the Wall Street Journal, Anthropic projects breaking even by 2028 two years ahead of OpenAI's 2030 target a distinction that public market investors are expected to value as a meaningful premium.

Anthropic's primary weakness is also its defining characteristic: the public benefit corporation structure, safety-first product philosophy, and governance model are less familiar to traditional equity markets than SpaceX's hardware-driven revenue or OpenAI's consumer brand. Its monthly active user base of approximately 134 million is a fraction of OpenAI's 900 million. The company is asking investors to bet on enterprise AI adoption continuing at current velocity and on its constitutional AI safety framework representing a durable competitive moat rather than a cost centre.

How Investors Are Preparing

Institutional preparation for this IPO wave has been underway for years, though the channel has historically been indirect. Investors seeking AI exposure have been forced to buy Nvidia for chip exposure, Microsoft for its OpenAI stake, and Alphabet for its Anthropic and DeepMind positions. The arrival of pure-play public listings unlocks pent-up demand that has no clean current outlet.

According to analysts at Goldman Sachs, as cited by Reuters and Nasdaq, total U.S. IPO proceeds in 2026 could reach approximately $160 billion a quadrupling from 2025 and that projection was made before this current wave fully materialised. The liquidity backdrop is supportive: there is an estimated $8 trillion sitting in U.S. money market funds. SpaceX's $75 billion raise represents roughly 1% of that pool. Crunchbase data shows global investors poured approximately $300 billion into roughly 6,000 startups in Q1 2026 alone, setting a single-quarter venture capital record, with roughly 80% of that capital flowing into AI-related fields. Institutional portfolios have spent years building AI-adjacent positions and are now actively modelling pure-play allocations.

At the retail level, the demand signals are already visible. Market strategist Ed Yardeni has noted that retail investors are receiving direct IPO invitations from their brokers for SpaceX. With 62% of American adults owning equities and retirement assets exceeding $20 trillion, Yardeni believes demand could prove deeper than many bears expect. SpaceX's unusually large retail allocation up to 30% is explicitly designed to absorb that demand. Pre-IPO secondary markets are also active: Anthropic shares were trading at approximately $1,447 per share on Hiive as of mid-2026, available to accredited investors, while Forge Global has been facilitating pre-IPO transactions in OpenAI shares for institutional clients.

Market Liquidity, the Magnificent Seven, and the Bull-Bear Debate

The central market-structure concern is not whether demand exists but where the capital comes from. Capital allocated to SPCX, OpenAI, or Anthropic must rotate out of existing positions. The most likely source is the current Magnificent Seven. Bank of America's Chief Investment Strategist Michael Hartnett has drawn comparisons between current market concentration and historical bubble extremes, warning that successful listings would push technology's weight in the S&P 500 above the 48% threshold surpassing concentration peaks seen during the 1990s dot-com era, the Japanese equity bubble of the 1980s, and the Nifty Fifty of the 1970s.

The complexity deepens with simultaneous equity issuance from existing mega-caps. Alphabet has announced an $80 billion equity issuance to fund AI computing infrastructure, consisting of a $30 billion concurrent underwritten public offering and a further $40 billion at-the-market offering starting in Q3 2026, alongside a $10 billion private placement with Berkshire Hathaway. The aggregate supply of new equity hitting markets in the second half of 2026 across SpaceX, OpenAI, Anthropic, and Alphabet could exceed $300 billion, a genuine test of institutional absorption capacity.

The counter-argument from the bulls is equally structured. Investment banks including JPMorgan, Goldman Sachs, and Morgan Stanley, all of which are directly involved in underwriting these listings, argue that the liquidity impact is manageable. They note that the AI infrastructure investment cycle is fundamentally different from the dot-com era: it is underpinned by long-term hyperscaler purchase commitments locking in real cash flows, not speculative revenue projections. If SpaceX, OpenAI, and Anthropic debut at or above their latest private valuations, the consequences extend beyond Silicon Valley: valuations above $1 trillion would immediately place each company among the ten largest S&P 500 constituents, triggering massive passive-fund rebalancing that would require index trackers to buy these names and reduce existing positions in current large-cap technology holdings. Over the medium term, as lockup periods expire and free float expands, the $466 billion Invesco QQQ ETF and similar Nasdaq-100 trackers would face mandatory rebalancing flows, redistributing capital in ways that could benefit the new listings at the expense of existing index heavyweights.

One dimension that separates this wave from prior IPO cycles is the sheer breadth of the artificial intelligence theme. The three companies are not competitors in a conventional sense: SpaceX is primarily an aerospace and satellite infrastructure company with an AI overlay through xAI; OpenAI is a consumer and enterprise AI platform built around the world's most recognised chatbot; Anthropic is an enterprise-focused frontier AI lab with a safety differentiation strategy. Investors can buy all three without duplicating their thesis. That diversification within the AI theme may ease the capital rotation concerns somewhat, as portfolio managers can justifiably build positions in all three without concentrated sector bets.

What the market cannot yet know is how post-listing performance will influence sentiment for the companies in the IPO pipeline behind these three. Bank of America has described this epic IPO cycle as essentially a large-scale transfer of accumulated risk from early private investors to the public market. Public investors who buy at or after IPO pricing are not capturing the same return profile as early backers; the private market has already done the bulk of the appreciation work. That dynamic does not make these bad investments, but it demands that post-IPO performance be evaluated against the entry price, not the founding-era narrative.

If you have enjoyed reading, spread the word:

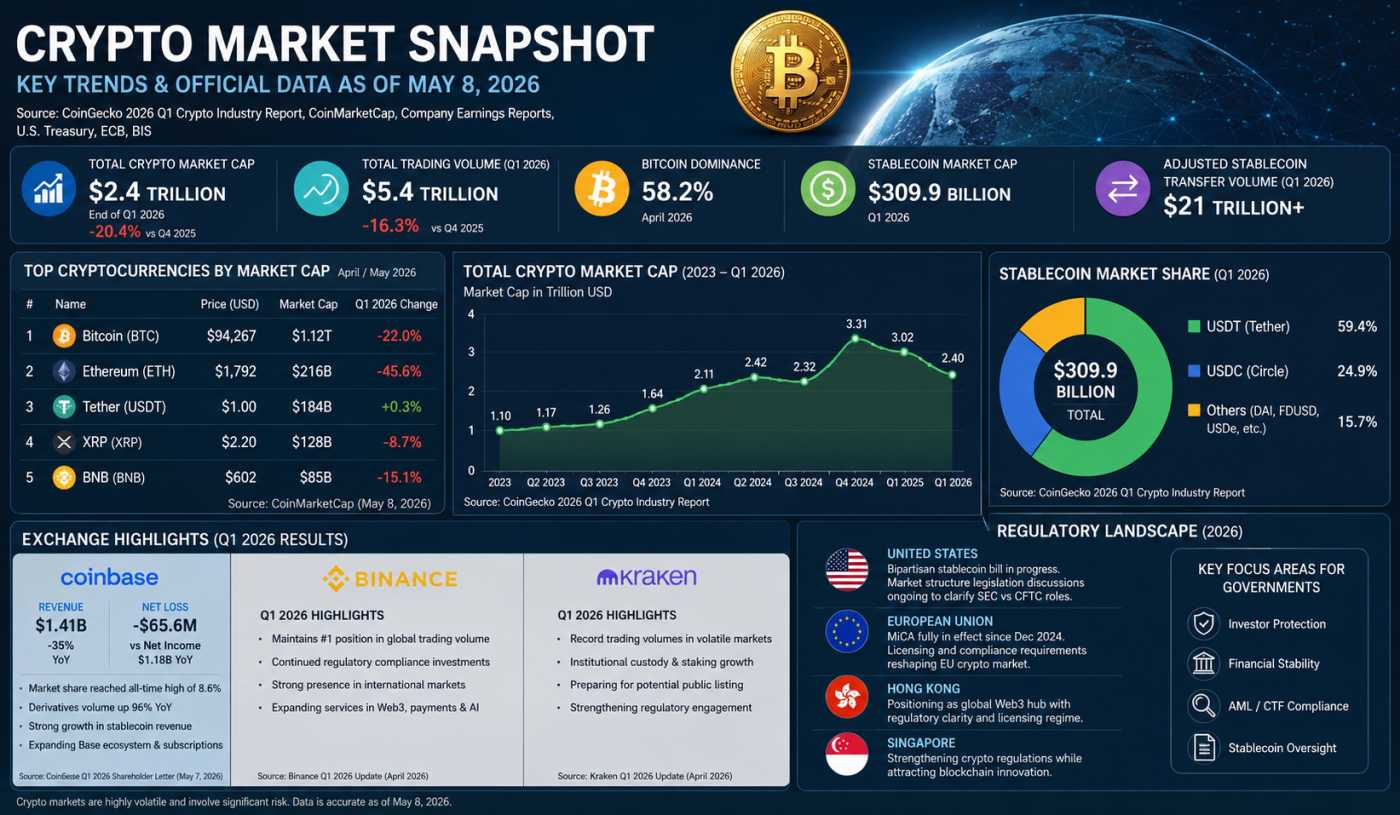

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

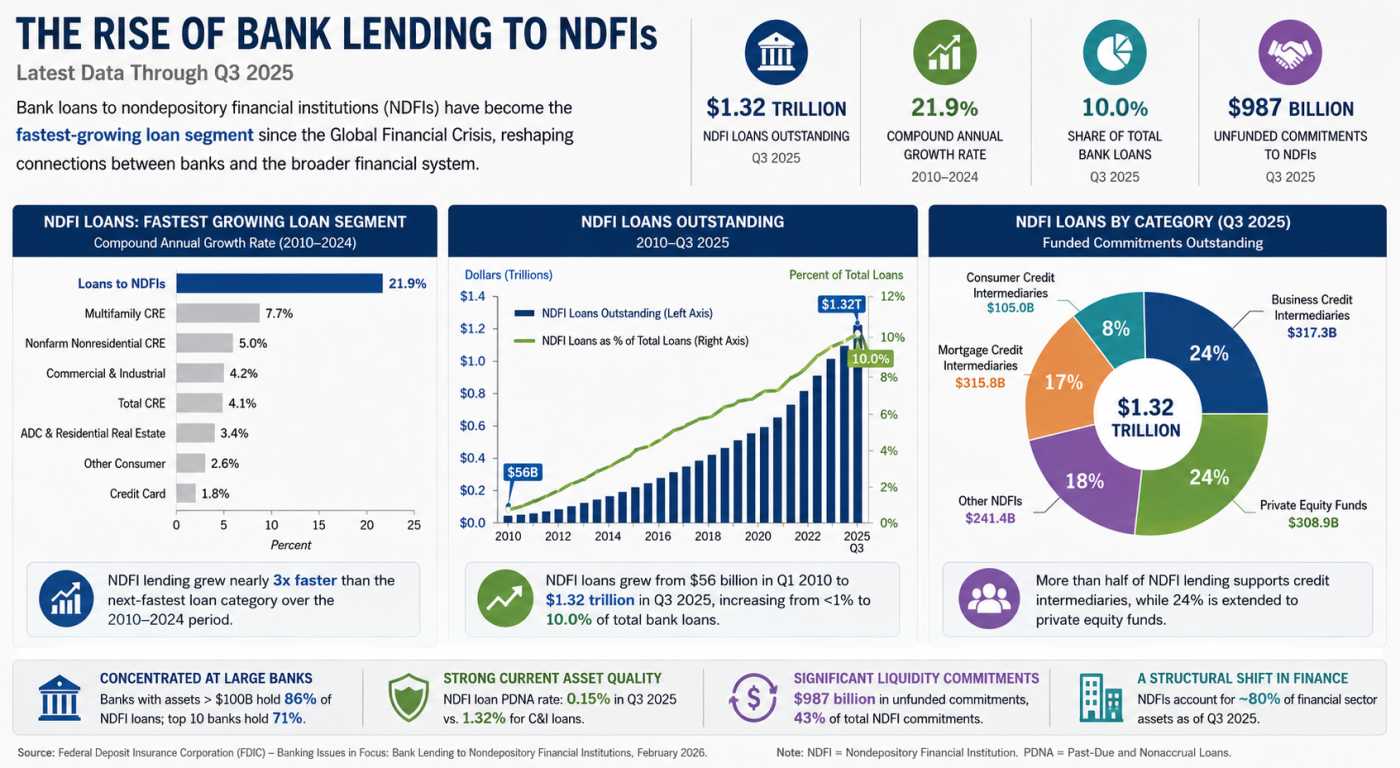

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun