Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

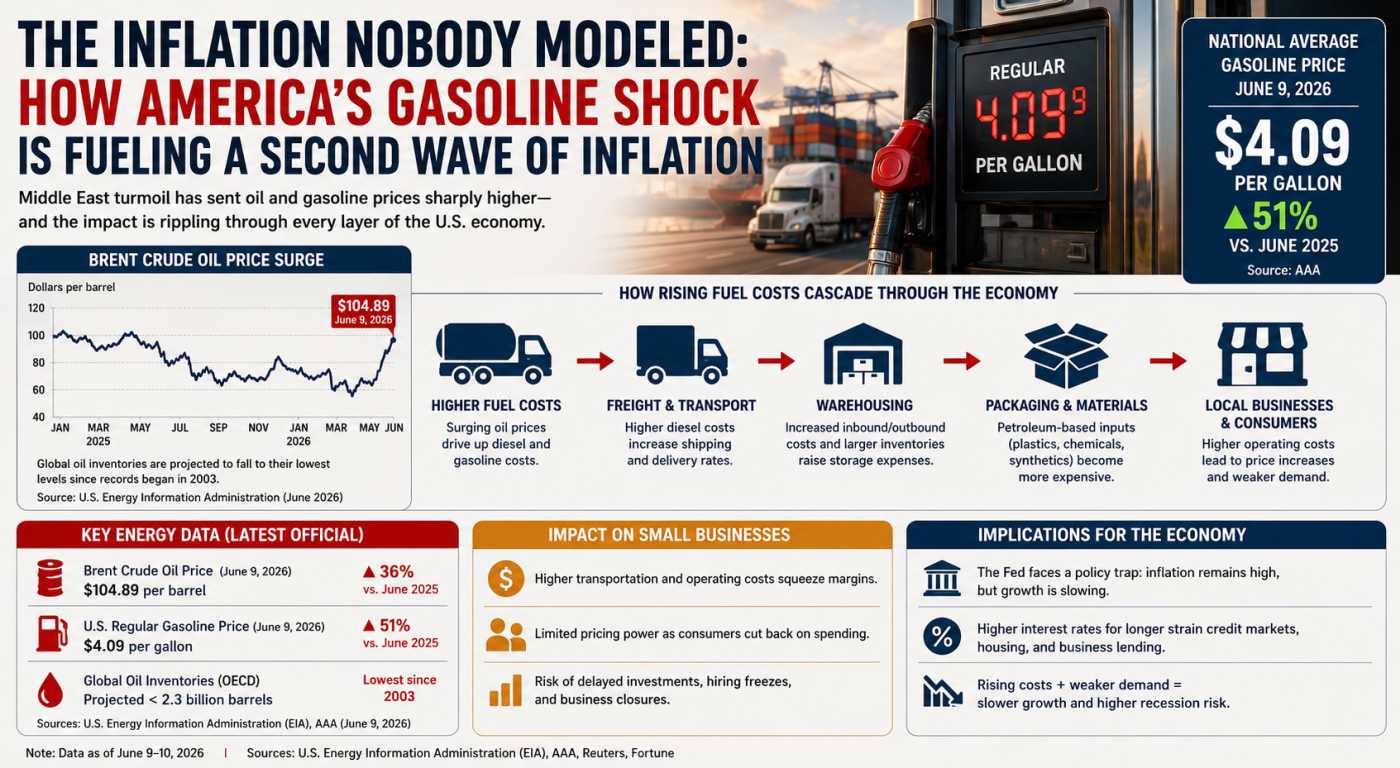

When Losing Money Pays: America's Broken Market Logic

The Hidden Time Bomb in AI Finance

Why Electricians Now Out-Earn Software Engineers

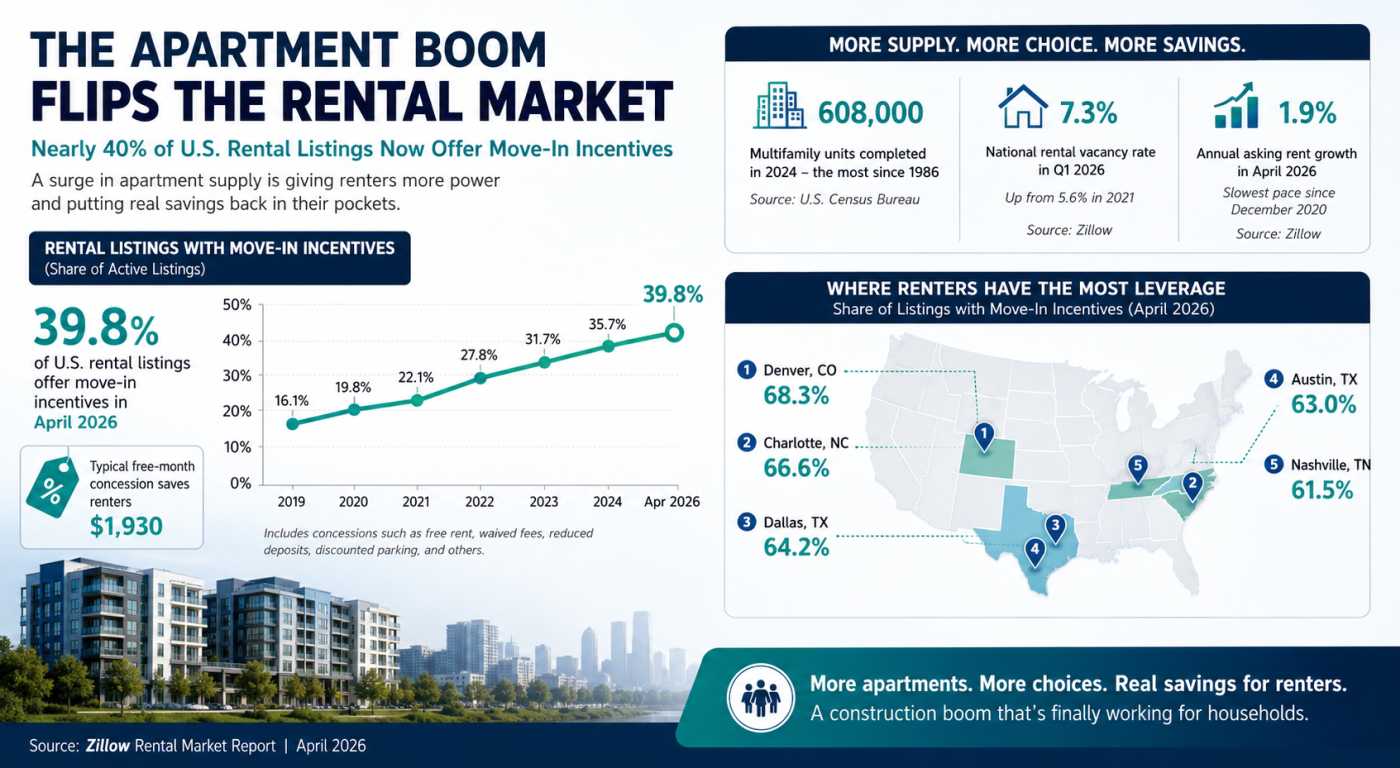

The Apartment Glut Changing America’s Rental Market

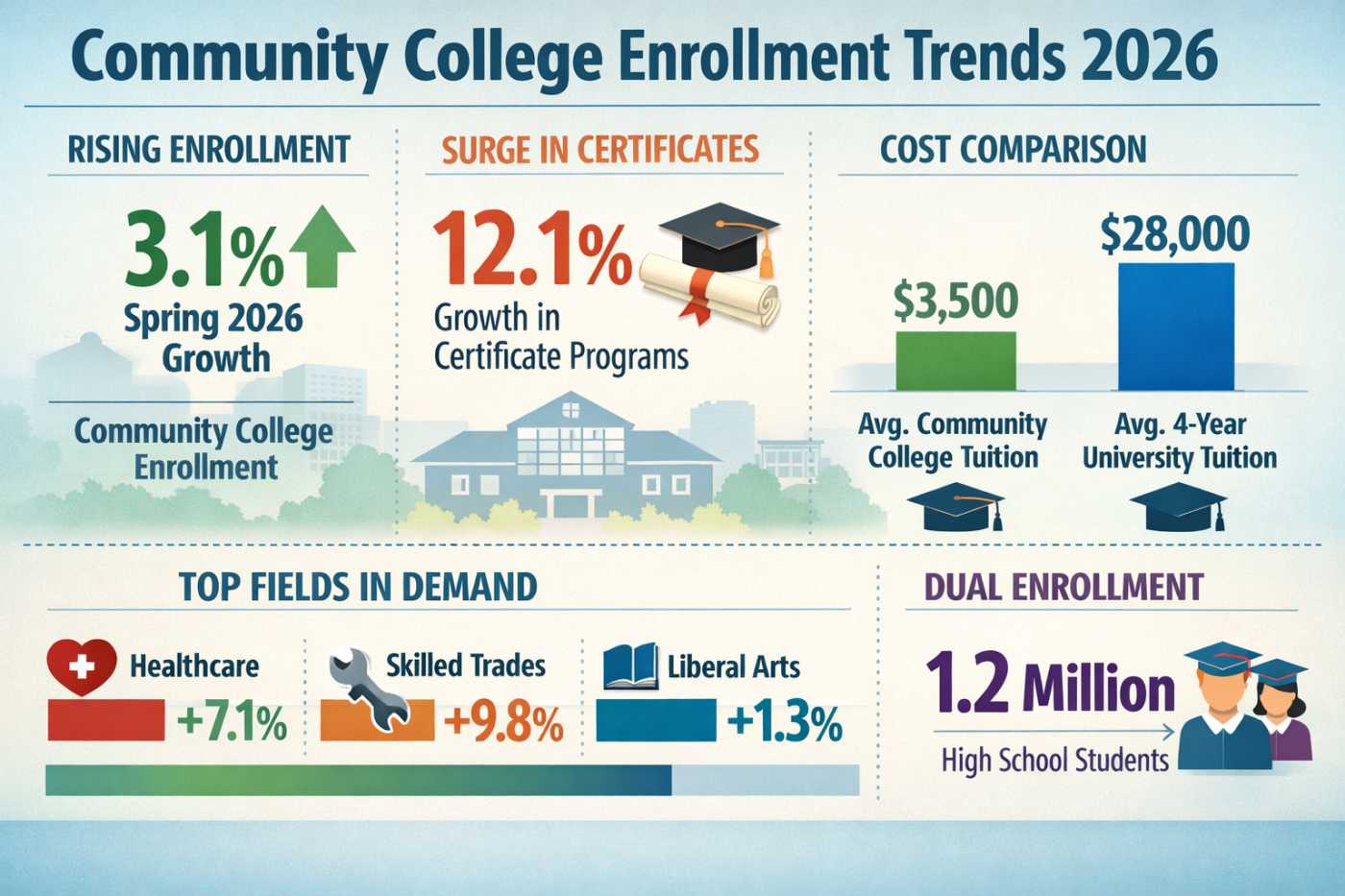

Why Community Colleges Are Winning Again

Repo, Debt and Risk: The Fed's Untold Warning for 2026

Washington's fiscal arithmetic has crossed a threshold that used to exist only in stress-test scenarios. The Congressional Budget Office's February 2026 baseline shows net interest outlays exceeding 3.2 percent of GDP in every year of the projection window, a level not recorded since at least 1940. In dollar terms, net interest payments are on track to more than double, from roughly $970 billion in 2025 to $2.1 trillion by 2036. CBO Director Phillip Swagel put it bluntly in testimony accompanying the release: "Our budget projections continue to indicate that the fiscal trajectory is not sustainable." Most commentary on this trajectory stops at the deficit arithmetic bigger borrowing needs, higher debt-to-GDP, eventual credit-rating pressure. That framing misses a quieter and arguably more immediate channel: the way escalating Treasury issuance is reshaping the balance sheets of banks, money-market funds, and repo intermediaries in ways that are already narrowing credit availability for small and mid-sized businesses, long before any headline sovereign-debt crisis becomes visible.

The mechanical starting point: issuance has to go somewhere

Debt held by the public stood at over $31 trillion as of February 2026, according to the Government Accountability Office's review of Treasury debt management, and CBO projects deficits will average more than $2 trillion annually through 2036. Every dollar of that borrowing has to be absorbed by the private financial system's balance sheet capacity banks, dealers, money-market funds, and increasingly, leveraged nonbank investors. That absorption is not neutral. It changes what those institutions can and will do with the rest of their balance sheets.

Banks themselves are part of the story. St. Louis Fed supervisory data show U.S. banks added $65 billion in Treasury securities in the first quarter of 2026 alone, pushing total holdings to $1.8 trillion, up from about $700 billion before the pandemic. At the largest, globally systemic banks, Treasuries now make up 7.5 percent of assets. Holding more government paper is not inherently destabilizing Treasuries are the textbook high-quality liquid asset but it does mean that a growing share of bank balance-sheet capacity, capital, and liquidity buffers is being allocated toward absorbing federal financing needs rather than expanding commercial and industrial lending capacity, at the margin, for smaller borrowers who compete for the same balance-sheet room.

Money-market funds: a parallel channel draining bank-adjacent funding

A second, less-discussed transmission mechanism runs through money-market funds. GAO's March 2026 debt-management report found money-market fund assets at an all-time high of $8.3 trillion as of February 2026, with more than 80 percent $6.8 trillion invested in funds holding only Treasury securities. That growth has been structurally reinforced by heavy Treasury bill issuance, which gives cash investors a safe, liquid, government-guaranteed alternative to bank deposits or commercial paper. Every dollar that migrates from a bank deposit into a Treasury-only money-market fund is a dollar that no longer directly funds bank loan books including the working-capital lines and term loans that small and mid-sized firms rely on. This is not deposit flight in a crisis sense; it is a slow, structural reallocation driven by heavy bill supply and attractive short-term yields, and it quietly tightens the deposit funding base available for SME lending even as headline financial conditions look calm.

Repo and the leverage layer that intermediates the Treasury glut

The system absorbs the remaining issuance largely through leveraged intermediation in the repo market, and this is where the Federal Reserve's May 2026 Financial Stability Report and its accompanying research flag the sharpest build-up of fragility. Large hedge funds' gross Treasury exposures doubled between 2023 and September 2025 to roughly $4.0 trillion $2.4 trillion long and $1.6 trillion short a pace of growth that outstripped the broader Treasury market itself, lifting hedge funds' share of outstanding Treasuries from about 4.5 percent to roughly 8.5 percent. Much of this exposure is financed through repo borrowing at very thin haircuts, with academic and regulatory estimates showing large shares of hedge fund Treasury repo occurring at zero or near-zero haircuts, producing leverage ratios that in some segments have exceeded 50-to-1. The Fed's own framework document for the Financial Stability Report explains why this matters for credit availability well beyond the Treasury market itself: institutions engaged in liquidity and maturity transformation can face sudden withdrawal pressure, and facing such pressure, they may need to sell assets quickly at "fire sale" prices, transmitting stress across markets and institutions that had no direct exposure to the original shock. A Treasury-financed deleveraging event in the basis trade does not stay contained to hedge funds and dealers; it forces banks that provide repo financing and prime brokerage to pull back risk capacity system-wide, and SME credit lines are typically among the first things trimmed when balance sheets tighten defensively.

Where this shows up first: the SME lending channel

This is not a hypothetical. The Federal Reserve's Senior Loan Officer Opinion Survey has recorded consecutive quarters Q4 2025 and Q1 2026 in which modest net shares of banks tightened commercial and industrial lending standards to firms of all sizes, including small firms specifically, alongside tighter collateralization requirements and lower maximum credit-line sizes for small borrowers. Banks cited a less favorable or more uncertain economic outlook and reduced risk tolerance as the dominant reasons. Crucially, these are not distress signals from a credit event; they are pre-emptive balance-sheet management decisions occurring while headline market functioning still looks orderly precisely the dynamic that should concern anyone watching for early warning signs rather than waiting for a visible sovereign-debt event. Small firms, unlike large and middle-market borrowers, have essentially no alternative financing channel when banks pull back: they cannot tap the bond market, and access to private credit is limited and increasingly itself under regulatory scrutiny for underwriting quality. When bank balance-sheet capacity is being reallocated toward absorbing Treasury issuance and toward repo intermediation of leveraged nonbank Treasury positions, SME lending is the residual claimant that absorbs the squeeze.

The BIS framework: fiscal space is now a financial-stability variable

The Bank for International Settlements has formalized this transmission logic in its 2026 Annual Economic Report and an accompanying working paper on financial stability limits to fiscal space. The BIS argues that a genuinely new "fiscal-financial stability nexus" has emerged, distinct from the traditional bank-sovereign doom loop of the euro-area crisis years. Because non-bank intermediaries, including highly leveraged hedge funds, now play an outsized role in absorbing sovereign issuance, stress can propagate through funding markets and across borders far faster than balance-of-payments-style debt dynamics would suggest. As the BIS puts it, fiscal space may shrink well before any limit implied by long-run fundamentals is reached. The accompanying BIS working paper models four specific amplification channels the bank-sovereign nexus, "original sin redux," duration mismatch, and repo-market deleveraging and shows that fiscal space becomes state-contingent: identical yield shocks compress available fiscal room more severely the closer an economy sits to its debt limit, and financial amplification can generate an effective debt ceiling even in the complete absence of default risk. Applied to the U.S. case, with net interest already the fastest-growing line item in the federal budget and CBO projecting ten-year Treasury yields averaging around 4.3 percent through 2036, this framework implies that the relevant constraint on U.S. fiscal space is not simply the interest rate-growth differential emphasized in conventional debt sustainability analysis, but the risk-bearing capacity of the banks, money-market funds, and leveraged repo intermediaries that must absorb ever-larger issuance flows.

Why this stays hidden until it doesn't

The reason this feedback loop is easy to miss is structural: each link in the chain looks individually benign. Banks holding more Treasuries is prudent liquidity management. Money-market fund growth reflects rational cash management by depositors chasing safe yield. Hedge fund basis trades are, in normal times, a liquidity-providing arbitrage that keeps futures and cash Treasury prices aligned. SLOOS tightening of a few percentage points looks like routine cyclical caution. None of these, viewed in isolation, resembles a crisis. But taken together, they describe a system in which an increasing share of aggregate balance-sheet capacity across banks, money funds, and leveraged intermediaries is being organized around financing the federal government, with private SME credit occupying the thinning residual space and with a leveraged repo layer sitting on top that the Fed itself now monitors as a funding-risk vulnerability rather than a settled feature of market plumbing. Systemic stress in this configuration would not necessarily announce itself as a failed Treasury auction or a spiking sovereign spread; it is more likely to first appear as a repo-rate spike during a heavy settlement period, a further quiet tightening in SLOOS small-firm figures, or a basis-trade unwind that forces dealers to restrict balance-sheet access more broadly. Those are the indicators worth tracking closely over the remainder of 2026, well ahead of any dramatic sovereign-debt narrative.

If you have enjoyed reading, spread the word:

The Liquidity Trap Hidden Inside Leveraged ETFs

SpaceX IPO Spawned a New Speculation Machine

How SpaceX Gave Main Street a Seat at the IPO

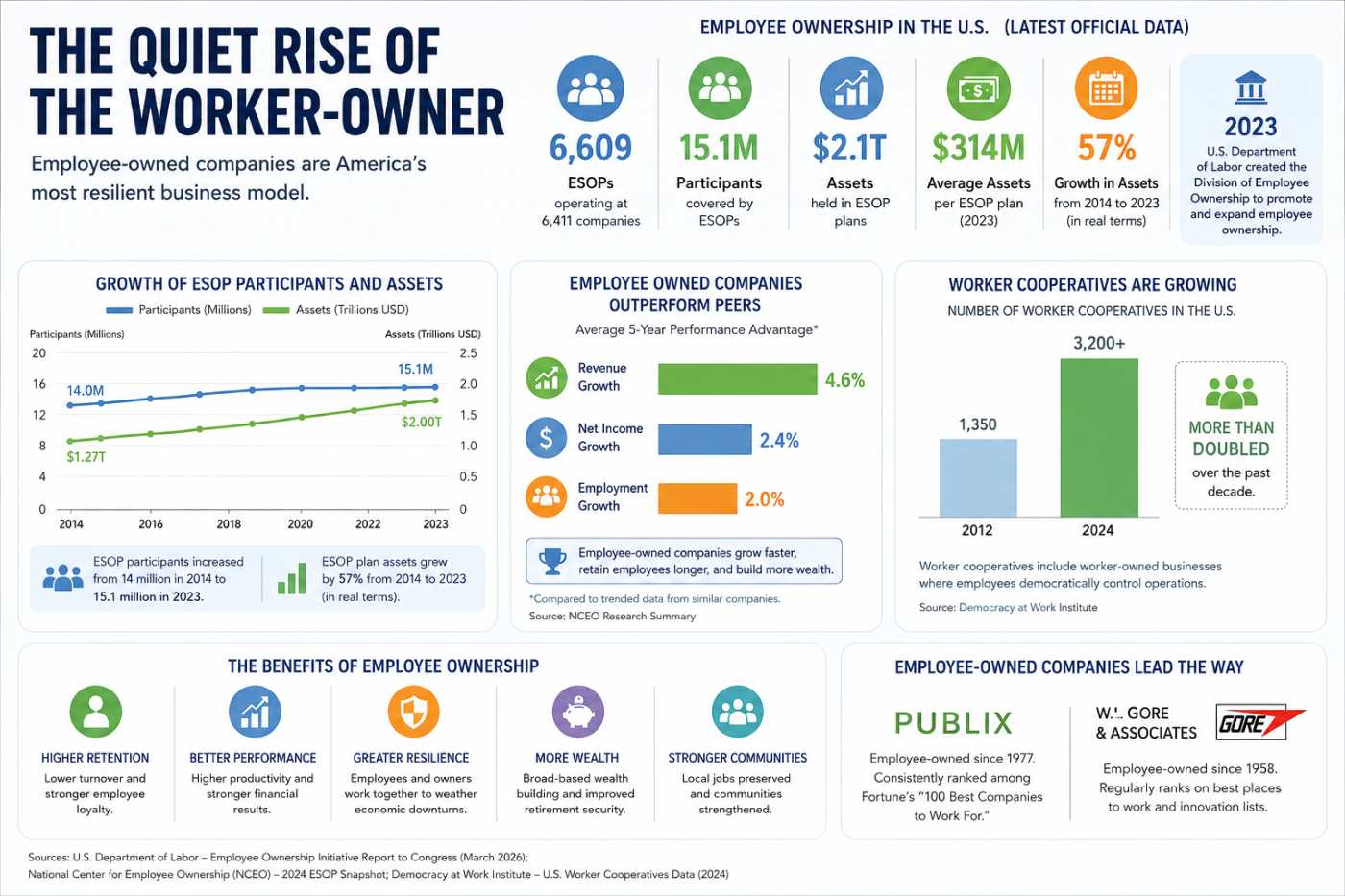

How Workers Became Capitalists