Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

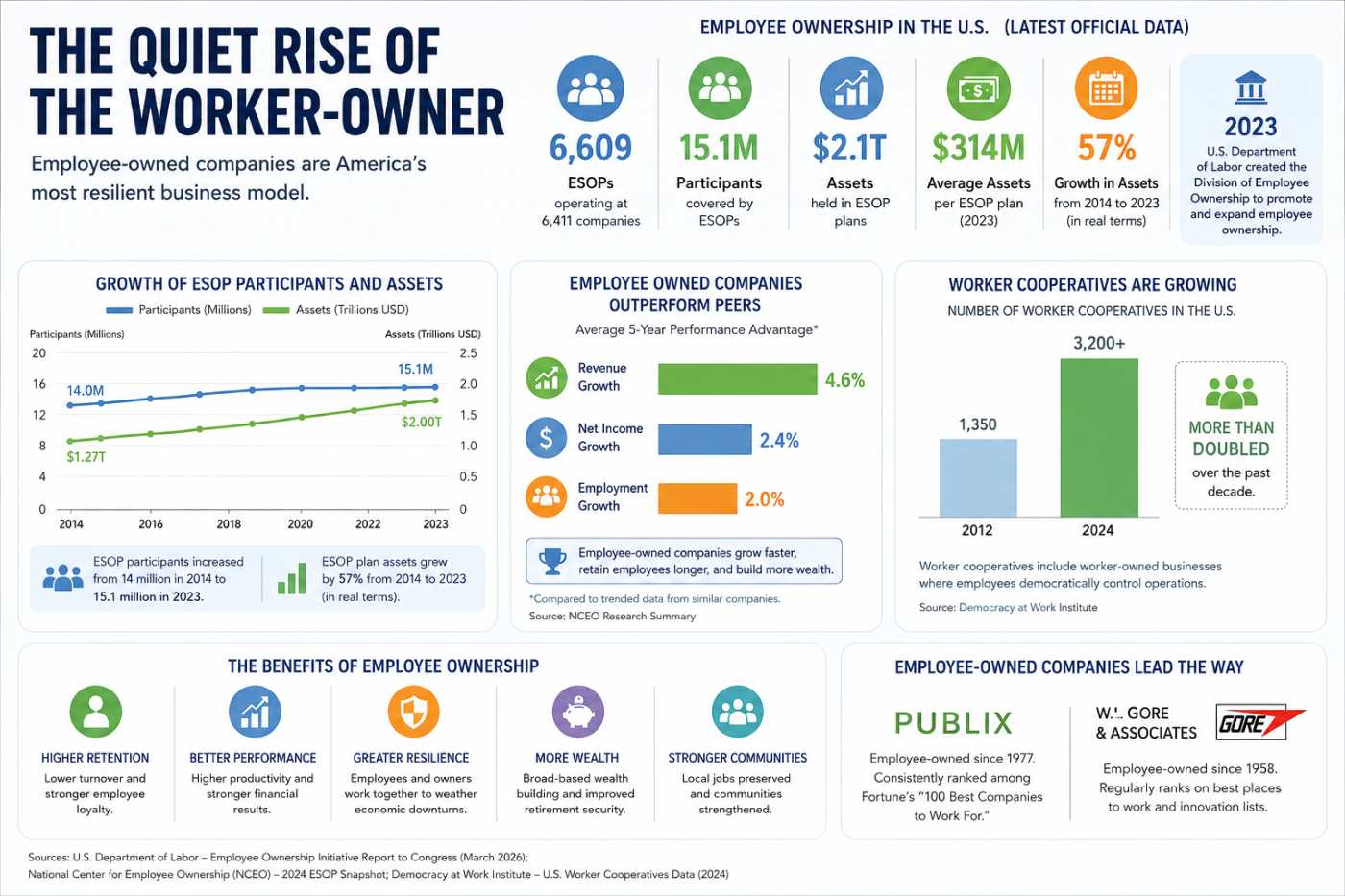

How Workers Became Capitalists

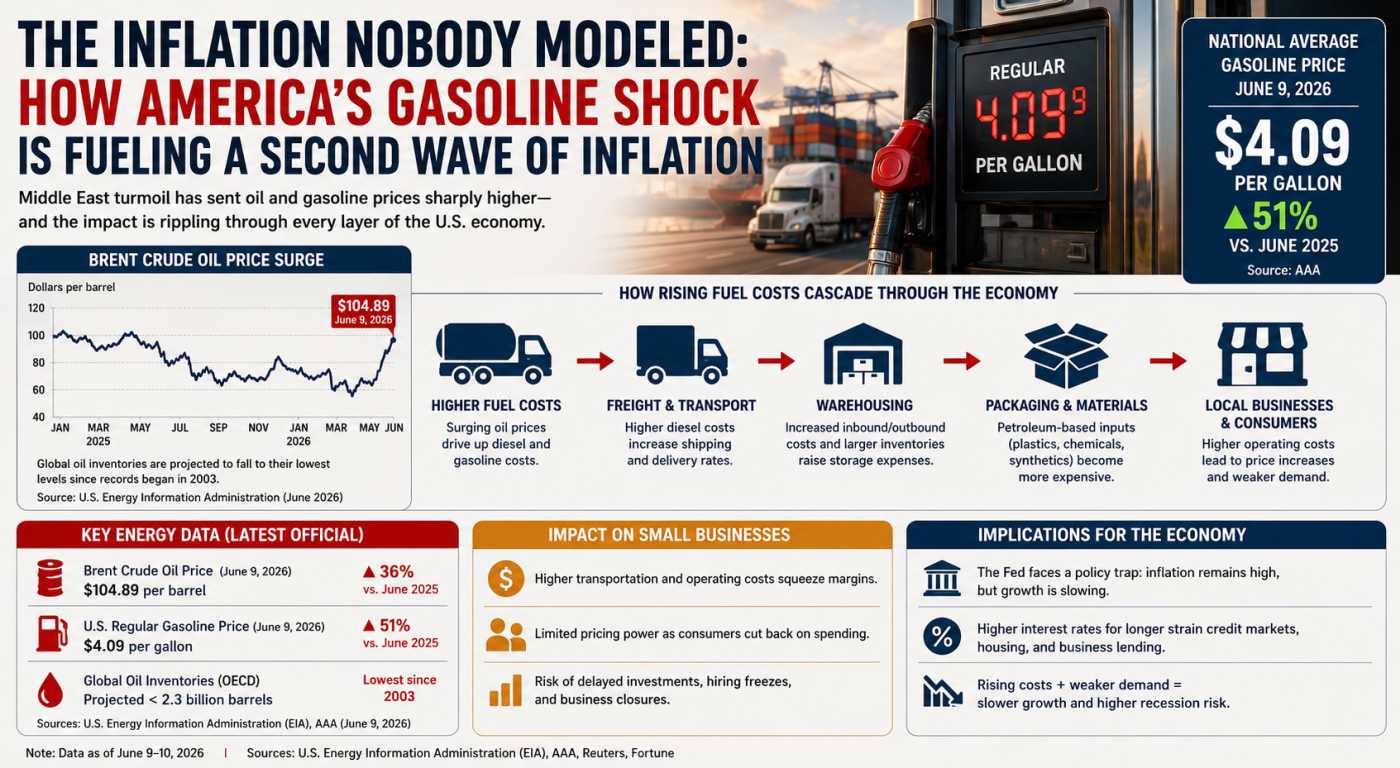

The Inflation Wave the Fed Can't Navigate

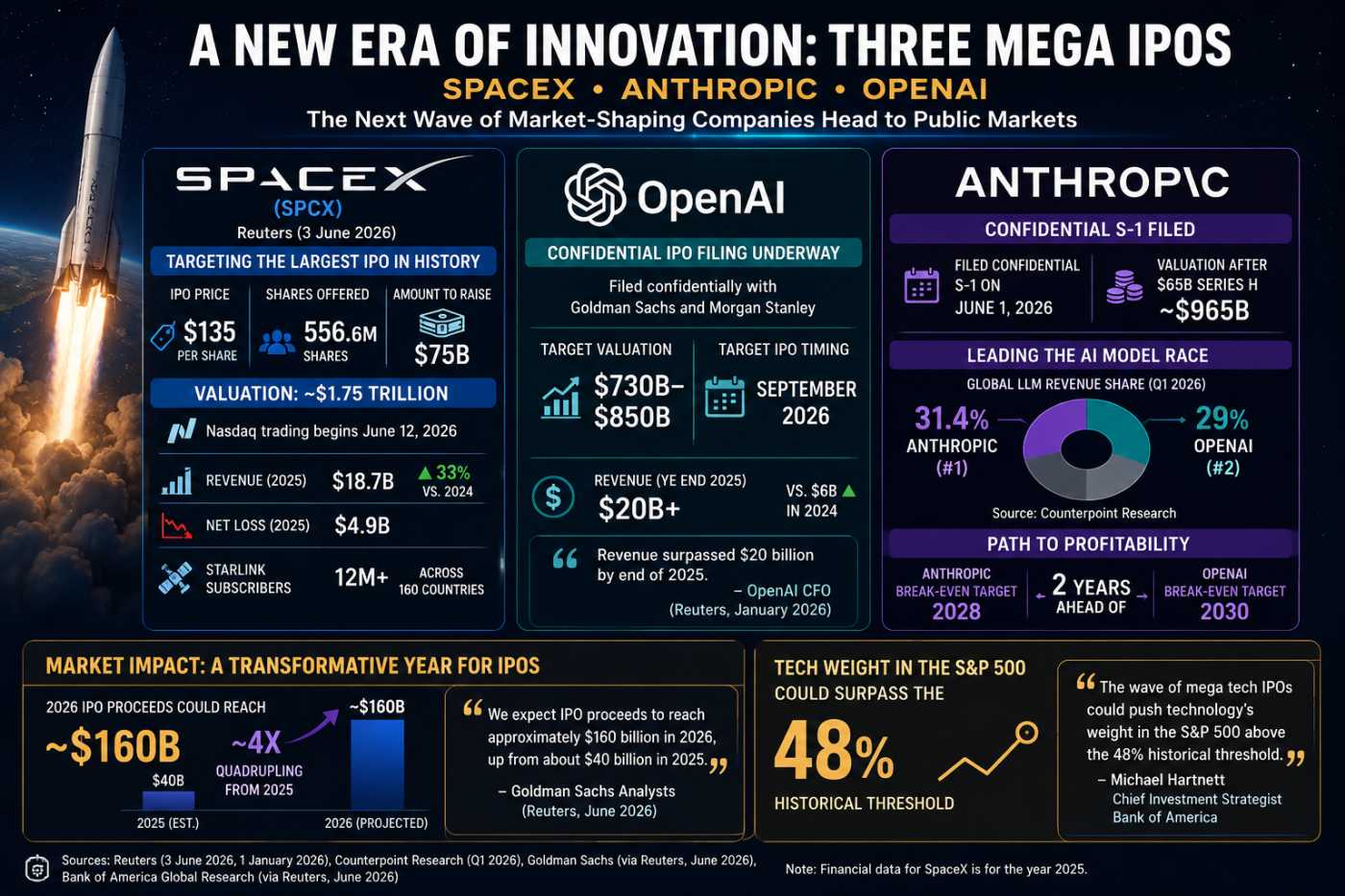

The Biggest IPO Year Ever: Can Markets Absorb It?

The Jobs Report That Crashed the Rally

The Fed Study Revealing Tomorrow's Investment Themes

How SpaceX Gave Main Street a Seat at the IPO

A Record-Breaking IPO That Changed More Than the Record Books

When SpaceX debuted on the Nasdaq on June 12, 2026, it achieved something Wall Street had never seen before. The company raised approximately $75 billion at an IPO price of $135 per share, valuing the space, satellite, and artificial intelligence company at roughly $1.77 trillion. The transaction eclipsed Saudi Aramco's previous record as the largest initial public offering in history and immediately placed SpaceX among the most valuable publicly traded companies in the world.

Yet the most consequential aspect of the IPO was not the amount raised, the valuation achieved, or even the first-day surge in trading. Instead, it was a structural decision that challenged decades of Wall Street convention: SpaceX deliberately reserved an unprecedented share of the offering for everyday investors.

According to Reuters reporting by Echo Wang and Milana Vinn, SpaceX considered allocating as much as 30% of the IPO to retail investors, far above the typical 5% to 10% allocation seen in most major offerings. The move represented one of the most ambitious attempts in modern capital markets to broaden access to a highly sought-after public listing.

For a company whose mission is built around expanding humanity's reach beyond Earth, the decision reflected a broader philosophy: if the future of space is meant to belong to everyone, perhaps ownership should as well.

The Traditional IPO Model Has Long Favored Institutions

For decades, the mechanics of IPO allocation have remained largely unchanged. Investment banks conducting public offerings typically distribute the majority of shares to institutional investors such as mutual funds, pension funds, hedge funds, sovereign wealth funds, and large asset managers.

The rationale is straightforward. Institutions can commit large amounts of capital, provide liquidity, and are often viewed as more stable long-term holders. Retail investors generally receive only a small portion of the shares, and in many cases gain access only after trading begins.

This system has created a persistent criticism of public markets: by the time ordinary investors are able to buy shares, much of the early upside has already been captured by institutions and insiders.

Several high-profile IPOs over the past decade demonstrated this imbalance. Companies such as Facebook, Airbnb, Snowflake, and others generated enormous investor demand, yet most retail participants had little opportunity to participate at the offering price.

SpaceX's leadership appeared willing to challenge that assumption.

From Mission Statement to Capital Markets Strategy

Although Elon Musk remains the dominant public face of SpaceX, company President Gwynne Shotwell has long played a central role in translating SpaceX's ambitions into operational reality. Over two decades, she helped transform a startup rocket company into a global aerospace, communications, and infrastructure giant.

Throughout that journey, Shotwell repeatedly emphasized making space more accessible. While the phrase was initially applied to launch costs, satellite connectivity, and future space infrastructure, the IPO suggested a broader interpretation.

Reuters reported that SpaceX's retail allocation strategy was specifically designed to capitalize on enormous demand from individual investors while departing from traditional Wall Street norms. The company was effectively arguing that retail participation should not be an afterthought but a core component of ownership.

That philosophy resonated immediately.

The Retail Demand Was Extraordinary

Even before trading began, evidence emerged that retail appetite for SpaceX stock was unlike anything markets had previously experienced.

Reuters reported on June 11 that retail investors had submitted more than $70 billion in orders for SpaceX shares ahead of the offering. The report cited people familiar with the process and noted that the company was considering a retail allocation of up to 30% of the IPO. Total demand for the offering reportedly exceeded $250 billion.

Those numbers are remarkable when viewed in context. If approximately 20% to 30% of the $75 billion offering ultimately flowed to retail participants, that would imply between $15 billion and $22.5 billion of direct participation by everyday investors on day one.

The scale matters because it demonstrates something many institutional investors have historically underestimated: retail investors are no longer a marginal force in capital formation.

The rise of commission-free trading, fractional shares, mobile brokerage platforms, social investing communities, and widespread financial education has fundamentally changed market participation. Millions of investors who once lacked access to IPO allocations can now mobilize capital at a scale previously associated only with large institutions.

Technology Democratized Access Before SpaceX Did

The SpaceX IPO did not emerge in isolation. It arrived after years of structural change in retail investing.

Platforms such as Robinhood, Fidelity, Charles Schwab, SoFi, and E*TRADE expanded access to IPO participation programs. Meanwhile, the pandemic-era surge in retail investing demonstrated that individuals were willing to actively engage with financial markets rather than merely invest through retirement accounts.

The so-called 'meme stock' era often drew criticism, but it also revealed an important reality: retail investors collectively possess substantial buying power when given access.

SpaceX's management appears to have recognized that reality and incorporated it into the IPO structure rather than resisting it.

In effect, SpaceX treated retail investors as stakeholders worthy of direct participation rather than passive observers expected to buy later in the secondary market.

Why This Matters Beyond SpaceX

The significance of the retail allocation extends beyond a single IPO.

Historically, IPOs have served two purposes. First, they raise capital. Second, they establish a shareholder base. The second objective is often overlooked, but it can influence corporate governance, market perception, and long-term investor loyalty.

By allocating a substantial portion of shares to individuals, SpaceX effectively created millions of potential brand ambassadors. Many retail investors were already customers of Starlink, followers of the company's missions, or supporters of its long-term vision.

Ownership deepens engagement. A customer who becomes a shareholder often develops a stronger interest in a company's success.

In that sense, the retail allocation was not merely a financing decision. It was also a strategic community-building exercise.

A New Form of Shareholder Capitalism?

The broader implication is that mega-IPOs may increasingly view retail participation as an advantage rather than a concession.

Traditional IPO allocation models evolved during an era when institutions dominated market access and information flow. Today's environment is different.

Retail investors now consume earnings calls, SEC filings, analyst reports, and financial media in real time. Social platforms can amplify investment narratives globally within hours. Individual investors collectively represent a significant source of liquidity.

Future issuers may observe the success of the SpaceX offering and ask an important question: if retail demand is already enormous, why allocate only a token percentage of shares?

The economics may become increasingly compelling for companies with strong consumer brands or passionate user communities.

The Risks of the Model Should Not Be Ignored

Despite its appeal, the SpaceX approach is unlikely to become universal.

Institutional investors still provide valuable functions. They conduct extensive due diligence, support secondary offerings, participate in governance discussions, and often maintain positions through periods of volatility.

A shareholder base dominated by retail investors can also create challenges. Individual investors may be more sensitive to headlines, social-media narratives, and short-term price movements.

Moreover, not every company commands the level of public enthusiasm that SpaceX enjoys. The combination of reusable rockets, Starlink's global network, artificial intelligence ambitions, and Elon Musk's celebrity status created conditions that are difficult to replicate.

What worked for SpaceX may not work for an industrial supplier, regional bank, or enterprise software company.

The Symbolism May Outlast the Structure

Even if future IPOs do not match SpaceX's retail allocation percentage, the symbolism of the offering may prove influential.

The IPO effectively challenged one of Wall Street's longest-standing assumptions: that institutions should receive the overwhelming majority of the most desirable public offerings.

By demonstrating that retail investors could absorb billions of dollars in shares while helping support one of the largest capital raises ever attempted, SpaceX provided evidence that the traditional allocation model is not the only viable option.

Markets often evolve gradually until a single event accelerates change. Electronic trading, commission-free brokerage accounts, direct listings, and SPACs all altered market structures after reaching critical mass.

The SpaceX IPO may ultimately be remembered as a similar inflection point.

Who Gets to Own the Future?

The most enduring legacy of the SpaceX IPO may not be its valuation, the first-day trading performance, or even its place in the record books. Instead, it may be the question it forced markets to confront.

If transformative companies increasingly shape the future of transportation, communications, artificial intelligence, biotechnology, and space exploration, who should be allowed to participate in their growth?

For decades, the answer largely favored institutions. SpaceX offered a different vision one in which ordinary investors were invited into the story from the beginning rather than after the fact.

Whether other companies follow the same path remains uncertain. But for one historic day in June 2026, the largest IPO in history suggested that ownership of the future might not belong exclusively to Wall Street anymore. It might increasingly belong to Main Street as well.

Sources: Reuters reporting by Echo Wang, Milana Vinn, Manya Saini and Niket Nishant; Nasdaq IPO filings; market trading data through June 15, 2026. Quotes and figures referenced from Reuters coverage of the SpaceX IPO. Links: Reuters June 12, 2026, Reuters, Nasdaq.

If you have enjoyed reading, spread the word:

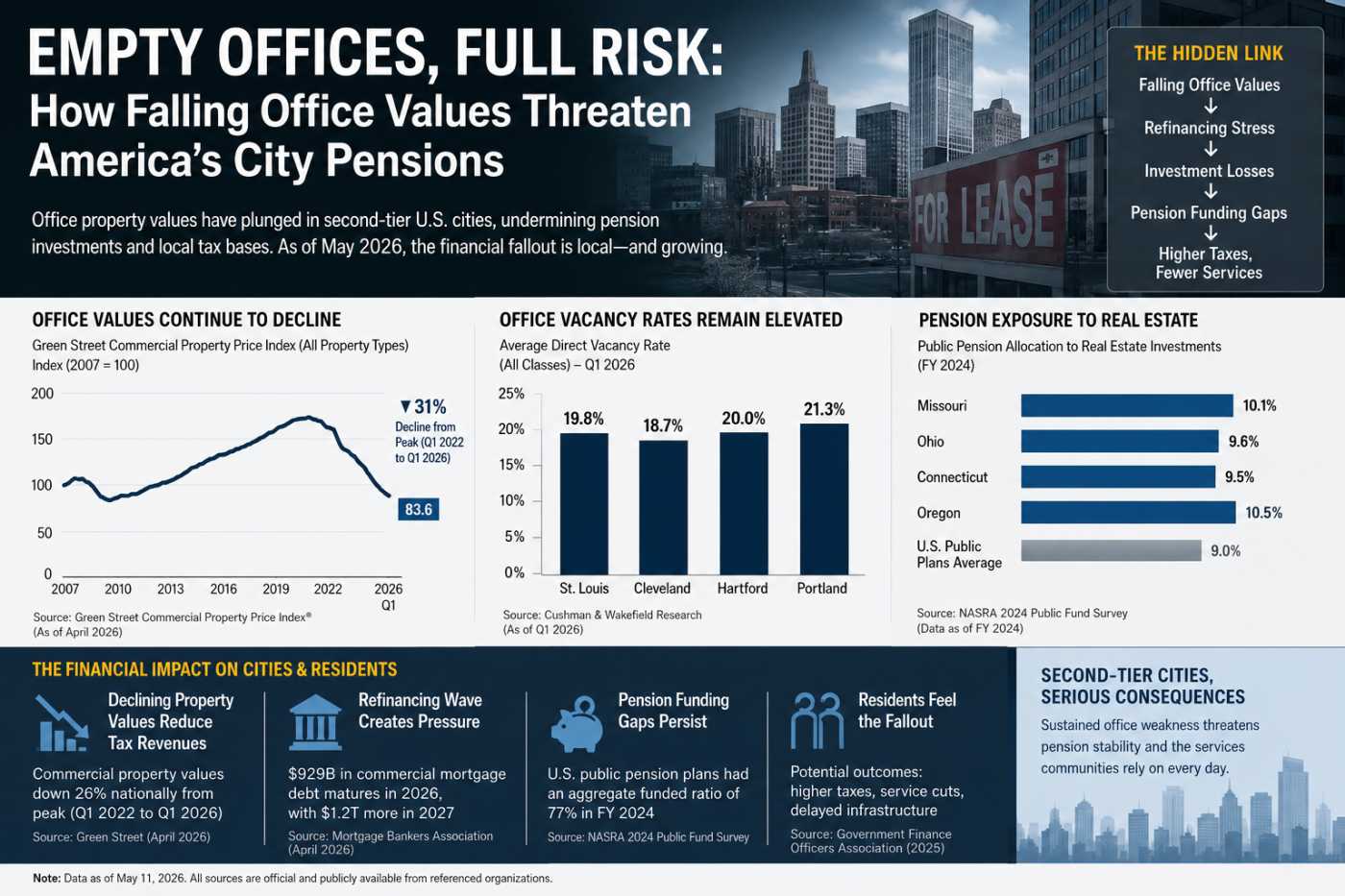

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

Crypto’s $2.4T Reality Check in 2026