Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

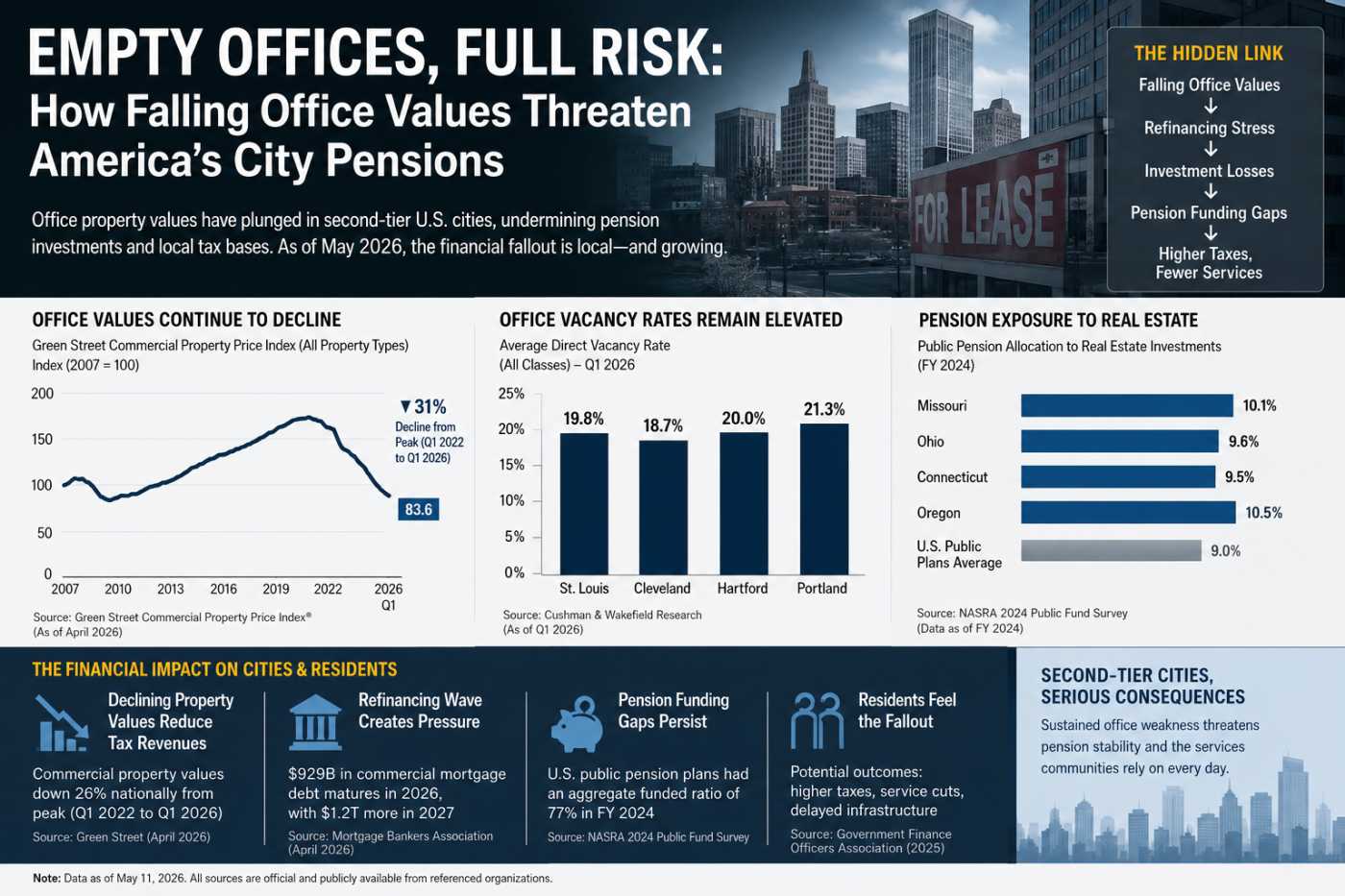

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

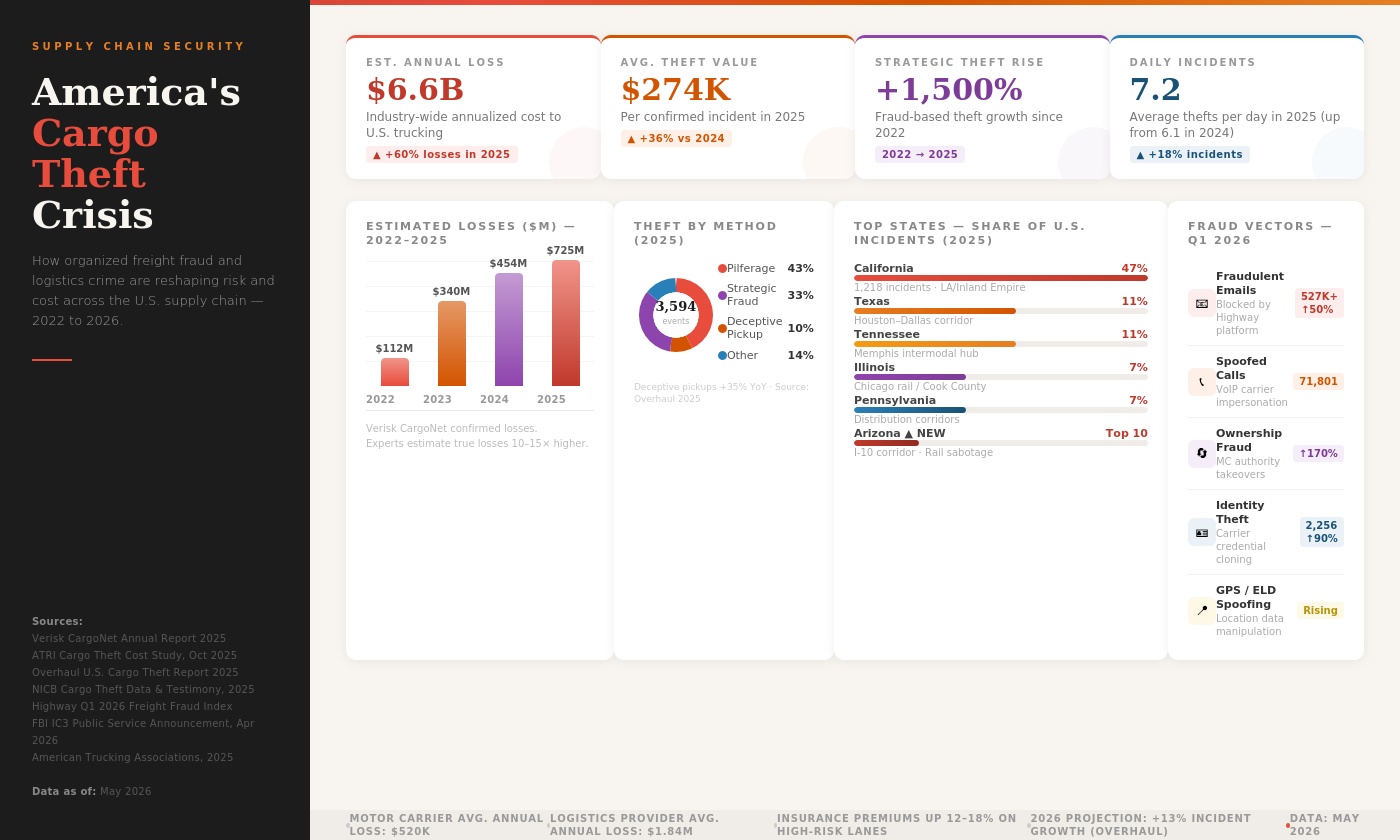

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

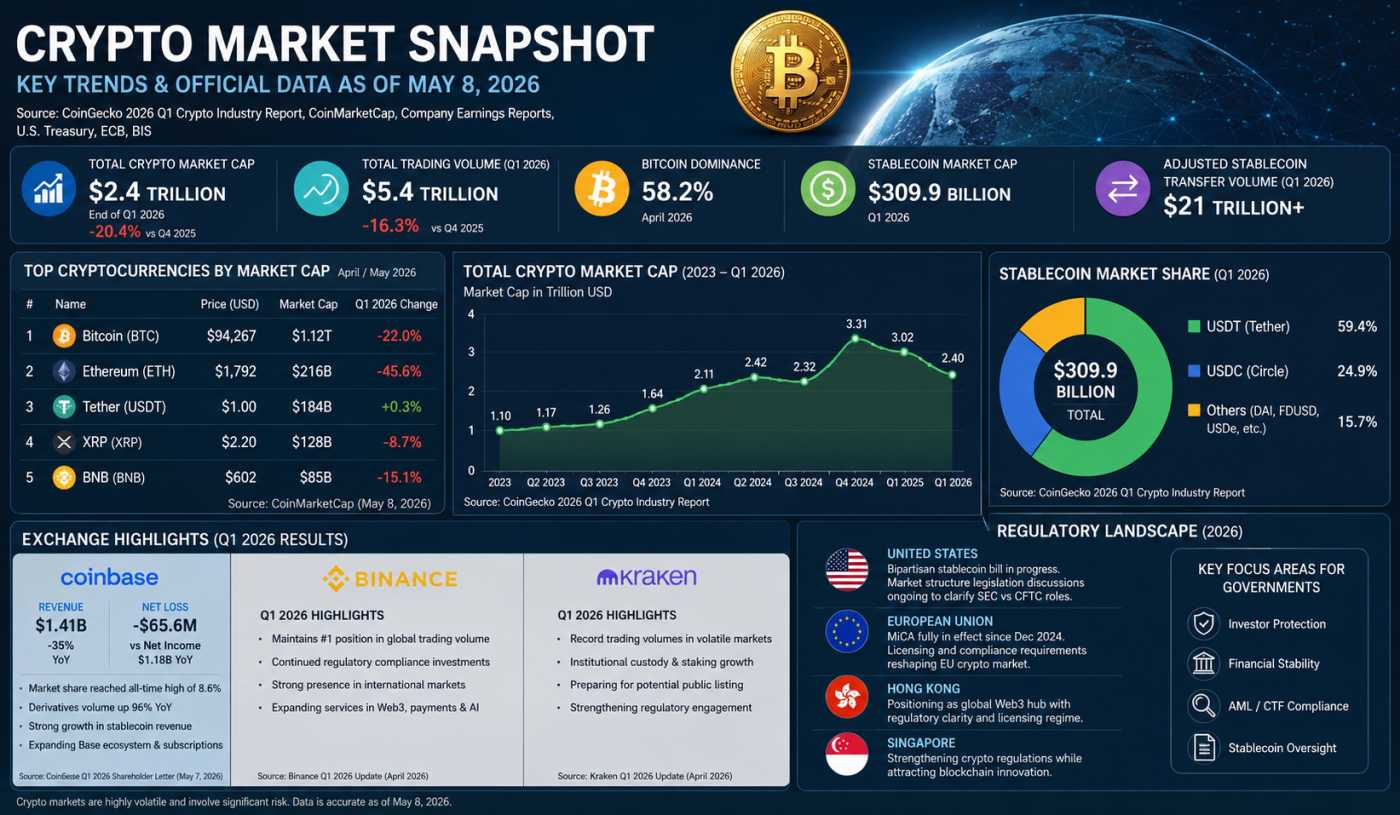

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

Crypto’s $2.4T Reality Check in 2026

The Crypto Market in 2026: Between Institutional Acceptance and Structural Uncertainty

As of May 8, 2026, the global cryptocurrency market is navigating one of its most complex phases since the sector emerged into mainstream finance. The industry is no longer driven purely by speculative retail enthusiasm. Instead, it is increasingly shaped by institutional capital flows, government regulation, stablecoin infrastructure, exchange consolidation, and macroeconomic conditions including interest rates, geopolitical tensions, and liquidity cycles.

According to CoinGecko’s 2026 Q1 Crypto Industry Report published in April 2026, the total cryptocurrency market capitalization stood at approximately $2.4 trillion at the end of the first quarter of 2026, down roughly 20.4% from the previous quarter and nearly 45% below the market peak reached in October 2025. The report highlighted falling trading volumes, weaker risk appetite, and macroeconomic stress tied to elevated oil prices and global geopolitical instability.

Despite this downturn, the market remains dramatically larger and more institutionally integrated than it was during earlier crypto cycles. Bitcoin, Ethereum, stablecoins, tokenized financial products, and decentralized finance applications are now deeply connected to global capital markets, payment systems, and even government policy debates.

The current state of crypto reflects a paradox: the infrastructure and legitimacy of the sector have strengthened significantly, even as prices and investor sentiment remain volatile.

Bitcoin Remains the Core Institutional Asset

Bitcoin continues to dominate the cryptocurrency ecosystem in 2026. Although its price has fluctuated sharply throughout the year, the asset still commands the largest share of total crypto market capitalization. Market data from early April 2026 showed Bitcoin dominance exceeding 58% of the overall crypto market, underscoring investor preference for perceived safety within digital assets.

Bitcoin experienced a difficult first quarter. CoinGecko reported that Bitcoin fell approximately 22% during Q1 2026, underperforming even major equity indices such as the Nasdaq and S&P 500 during the same period. Much of the weakness stemmed from tighter monetary expectations in the United States, geopolitical instability linked to Middle East tensions, and reduced speculative appetite across global financial markets.

Nevertheless, institutional participation has not disappeared. Spot Bitcoin exchange-traded funds in the United States continue to attract strategic long-term investors, even amid volatility. Analysts across multiple research firms noted that ETF-related inflows turned positive again in late Q1 after several weeks of heavy outflows.

Institutional adoption has also evolved beyond simple price exposure. Pension funds, family offices, and hedge funds increasingly view Bitcoin as a macroeconomic hedge against long-term currency debasement and sovereign debt instability. However, unlike earlier years, these investors are now more valuation-sensitive and macro-aware, reducing the extreme momentum-driven behavior that characterized prior crypto bull runs.

Ethereum Faces a Defining Period

Ethereum remains the second-largest cryptocurrency by market capitalization, but the network faces a more nuanced outlook than Bitcoin. Ethereum continues to dominate large sections of decentralized finance, tokenization, and smart contract infrastructure, yet it is confronting growing competition from alternative blockchain ecosystems including Solana, Avalanche, and Layer-2 scaling platforms.

Ethereum prices have declined substantially from the highs reached during the 2025 rally. Market participants have become increasingly concerned about transaction fee economics, slower decentralized finance growth, and fragmentation of developer activity across competing chains.

However, Ethereum still retains enormous strategic importance. Stablecoin settlement volumes on Ethereum-related ecosystems remain massive, and many tokenized financial products continue to rely on Ethereum-compatible infrastructure. Major financial institutions experimenting with blockchain-based settlement systems have largely focused on Ethereum or Ethereum-derived technologies.

The broader investment narrative around Ethereum has shifted away from speculative meme activity toward infrastructure utility. Investors are now evaluating Ethereum more like a technology platform than a purely speculative asset.

Stablecoins Are Quietly Becoming Crypto’s Most Important Sector

One of the most important developments in 2026 is the continued growth of stablecoins. While speculative crypto assets experienced sharp declines during Q1, the stablecoin market remained relatively resilient.

CoinGecko reported that the stablecoin sector maintained a market capitalization of approximately $309.9 billion during Q1 2026. Tether’s USDT remained the dominant stablecoin with roughly $184 billion in circulation, while Circle’s USDC grew to over $77 billion.

The importance of stablecoins now extends far beyond crypto trading. Stablecoins are increasingly used for cross-border payments, settlement infrastructure, decentralized finance applications, and business-to-business transfers. Some analysts estimate that adjusted stablecoin transfer volumes exceeded $21 trillion during Q1 2026, illustrating the scale of activity occurring outside traditional banking rails.

This growth has attracted significant government attention. Policymakers in the United States, Europe, and Asia increasingly view stablecoins as a bridge between traditional finance and blockchain infrastructure. The regulatory focus has shifted toward reserve transparency, consumer protection, anti-money laundering compliance, and systemic financial risk.

At the same time, stablecoins introduce new concentration risks. A handful of companies now control a large portion of digital dollar liquidity worldwide. Regulators remain concerned about reserve quality, redemption mechanisms, and the potential for stablecoin runs during periods of financial stress.

Coinbase, Binance, and the Battle for Exchange Dominance

The exchange sector remains central to the crypto industry’s financial health. In 2026, exchanges are navigating a difficult balance between regulatory compliance, declining trading volumes, and the need to diversify revenue streams beyond transaction fees.

Coinbase reported mixed Q1 2026 results. According to company disclosures released on May 7, 2026, revenue fell approximately 35% year-over-year to around $1.41 billion, while transaction revenue declined sharply due to lower trading activity. The company also reported a quarterly net loss amid weaker market conditions.

Yet the same report revealed important structural strengths. Coinbase stated that its crypto trading market share reached an all-time high of 8.6%, while derivatives trading volume increased substantially. The company also highlighted rapid growth in stablecoin activity and decentralized exchange integration through its Base blockchain ecosystem.

Perhaps most importantly, Coinbase emphasized that it now generates meaningful revenue from multiple business segments including custody, derivatives, subscriptions, stablecoins, and prediction markets. This diversification reflects a major strategic shift occurring across the exchange industry.

Binance remains the world’s largest crypto exchange by trading volume, though it continues to operate under heavy regulatory scrutiny in multiple jurisdictions. The company has spent the past two years restructuring compliance systems, tightening customer verification procedures, and adapting to stricter global regulatory standards.

Despite these pressures, Binance continues to dominate international retail trading activity and remains highly influential in crypto liquidity formation. However, its long-term outlook increasingly depends on its ability to secure regulatory licenses in key markets including the European Union and the United Kingdom.

Kraken has also gained attention in 2026 amid reports of potential public listing plans. Investors increasingly view regulated crypto infrastructure firms as a new category of fintech investment rather than purely speculative businesses.

Regulation Is No Longer a Peripheral Issue

Regulation has become the defining factor shaping the future of the cryptocurrency industry. Governments are no longer debating whether crypto should exist; instead, they are debating how it should integrate into existing financial systems.

In the United States, lawmakers continue working on comprehensive digital asset legislation that would clarify jurisdiction between the Securities and Exchange Commission and the Commodity Futures Trading Commission. Stablecoin legislation has emerged as a particular area of bipartisan interest.

The broader regulatory environment has become more constructive compared to the aggressive enforcement-focused period of 2022 through 2024. Nevertheless, uncertainty remains significant. Exchanges and token issuers still face ambiguity regarding securities classification, consumer protections, and capital requirements.

Europe is moving forward with the Markets in Crypto-Assets framework, commonly known as MiCA. The regulations are expected to significantly reshape how crypto firms operate across the European Union. Firms lacking proper licenses may lose access to EU customers, accelerating consolidation among larger compliant exchanges.

Meanwhile, several Asian governments continue pursuing differing strategies. Singapore and Hong Kong have positioned themselves as regulated crypto hubs, while China maintains its restrictive stance on most retail crypto activities despite ongoing blockchain development initiatives.

Government attitudes toward crypto have therefore become increasingly pragmatic rather than ideological. Authorities recognize that blockchain technology and digital assets are unlikely to disappear, but they also remain concerned about fraud, financial stability risks, and illicit finance.

The Industry Still Faces Major Structural Risks

Despite growing institutional legitimacy, the cryptocurrency market continues to face serious risks.

One of the biggest concerns remains leverage. Crypto derivatives markets remain highly speculative, and excessive leverage continues to amplify volatility during periods of market stress. Sharp liquidations regularly trigger cascading price movements that exceed volatility levels seen in traditional financial markets.

Cybersecurity risks also remain substantial. Major hacking incidents, phishing attacks, and state-linked cybercrime operations continue to target crypto exchanges and decentralized finance platforms. Regulatory agencies increasingly view operational security as a systemic issue rather than a niche technical concern.

Another challenge is market concentration. Bitcoin and a small number of large exchanges account for a disproportionately large share of market activity. Stablecoin concentration further increases systemic dependence on a few infrastructure providers.

The decentralized finance sector has also experienced slower growth compared to earlier expectations. While decentralized exchanges and lending protocols remain active, total value locked across many DeFi ecosystems remains below previous cycle highs.

Macroeconomic conditions represent an additional challenge. Crypto assets continue to behave largely as high-risk liquidity-sensitive investments rather than fully independent alternative assets. Rising real interest rates, tighter central bank policy, and slowing global growth have reduced speculative capital inflows.

Why Institutional Investors Still Remain Interested

Despite volatility and regulatory challenges, institutional interest in crypto remains significant because the sector now offers more than speculative trading.

Tokenization of real-world assets has emerged as one of the most closely watched areas of development. Financial institutions are increasingly experimenting with blockchain-based settlement systems for bonds, money market products, and private assets.

Stablecoin infrastructure is also becoming integrated into payment systems and international transfers. Some analysts believe blockchain-based settlement rails could eventually reduce costs for global remittances and cross-border corporate payments.

Additionally, major financial firms increasingly view digital assets as part of broader financial infrastructure modernization rather than a standalone speculative niche. Custody services, tokenized securities, programmable payments, and blockchain-based collateral systems continue attracting investment.

The growing presence of regulated crypto ETFs, publicly traded custody firms, and institutional-grade exchanges has further normalized the sector within global finance.

The Outlook for Crypto Investors in 2026

The cryptocurrency market in 2026 presents both substantial opportunity and considerable uncertainty. The speculative excesses of earlier cycles have diminished, but so has the easy momentum-driven optimism that once defined the industry.

Crypto is increasingly becoming a mature, infrastructure-oriented sector shaped by regulation, institutional participation, and macroeconomic forces. This evolution may reduce some of the explosive upside associated with earlier bull markets, but it also strengthens the long-term durability of the ecosystem.

Bitcoin remains the dominant institutional asset within crypto, stablecoins are becoming systemically important financial tools, and blockchain infrastructure continues attracting corporate and government interest. At the same time, regulatory complexity, cybersecurity threats, leverage-driven volatility, and macroeconomic sensitivity remain major risks.

The coming years will likely determine whether cryptocurrencies evolve into a deeply integrated layer of global finance or remain primarily speculative digital assets operating alongside traditional systems. Current evidence suggests that elements of both outcomes are already unfolding simultaneously.

If you have enjoyed reading, spread the word:

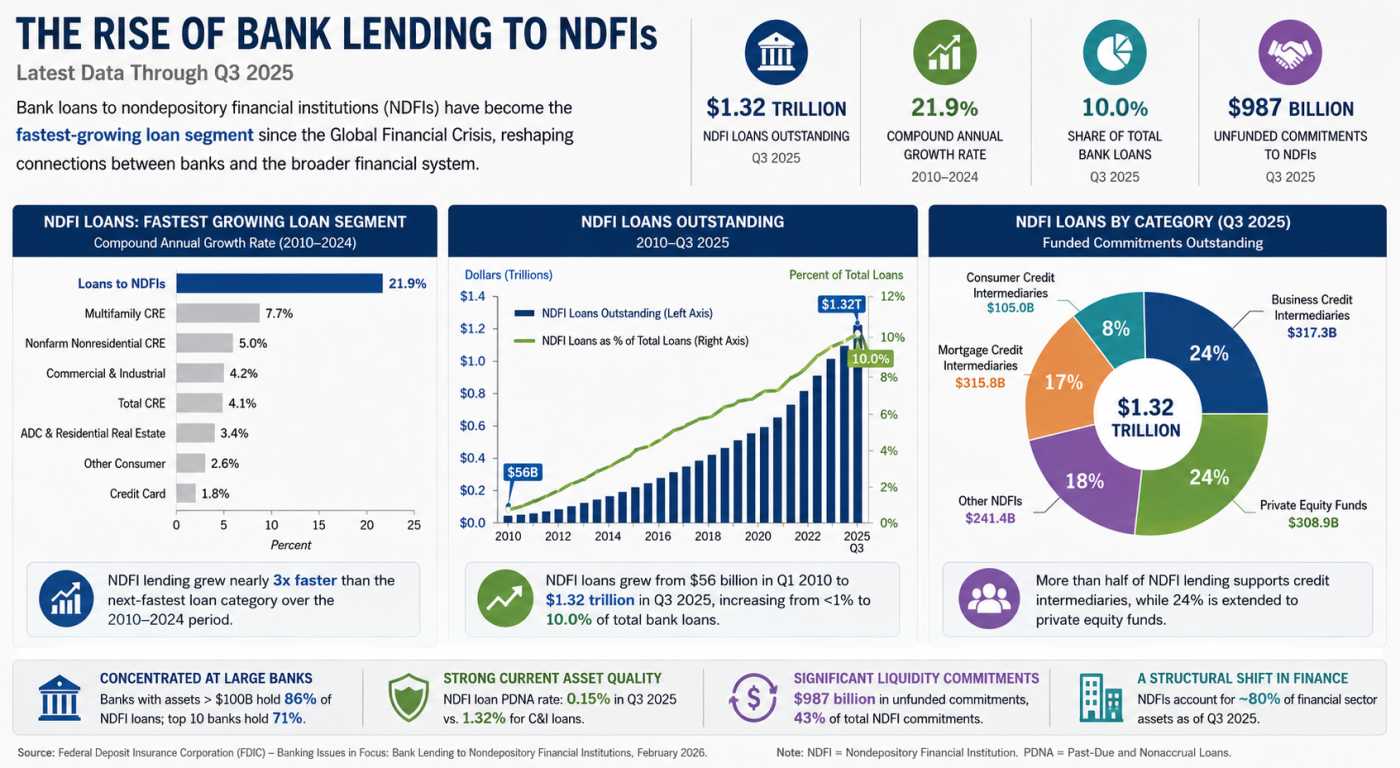

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America

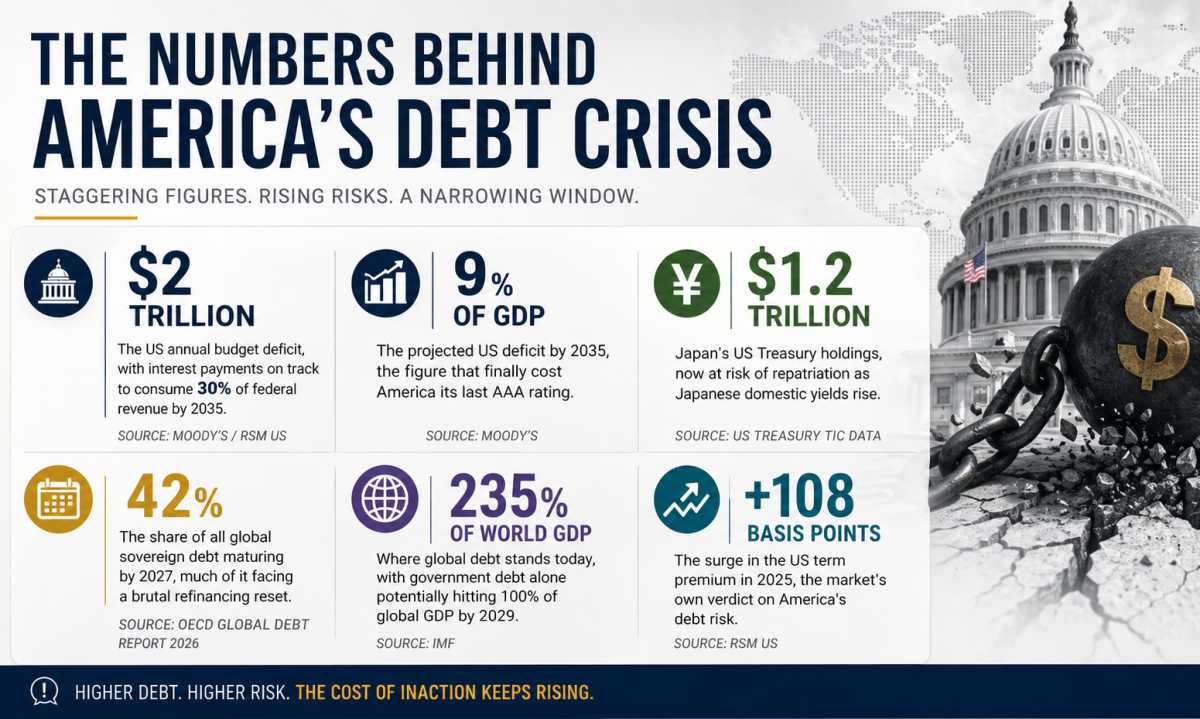

Debt, Deficits & Disaster: The Bond Market Crisis