Debt, Deficits & Disaster: The Bond Market Crisis

Not Wall Street, But AI: The Real Force Democratizing Finance Across America

When Flooding Pays: A New Financial Bet

Breakfast for Life How Local Diners and Hardware Stores are Outsmarting Amazon

Fundamentals for UDR, Inc.

*UDR makes the list of companies with the worst fundamentals at present.

Business Operations:

Sector: Real EstateIndustry: REIT - Residential

UDR, Inc. is a S&P 500 company, is a leading multifamily real estate investment trust with a demonstrated performance history of delivering superior and dependable returns by successfully managing, buying, selling, developing and redeveloping attractive real estate properties in targeted U.S. markets. As of December 31, 2025, UDR owned or had an ownership position in 60,941 apartment homes, including 300 apartment homes under development. For over 53 years, UDR has delivered long-term value to shareholders, the best standard of service to residents and the highest quality experience for associates.

Revenue projections:

UDR's projected revenue decline from last year is likely to make investors cautious. Lower revenues often hurt a company's bottom line, leading investors to be concerned about the company's ability to maintain profitability and deliver strong financial results in the future.

Financial Ratios:

| currentRatio | 0.583000 |

|---|---|

| forwardPE | 60.649998 |

| debtToEquity | 142.368000 |

| earningsGrowth | 1.496000 |

| revenueGrowth | -0.004000 |

| grossMargins | 0.663550 |

| operatingMargins | 0.183440 |

| trailingEps | 1.470000 |

| forwardEps | 0.600000 |

UDR, Inc.'s current ratio 0.583 indicates the company may struggle to cover its short-term liabilities with available cash reserves and current assets. This points to potential liquidity challenges, signaling that UDR, Inc. might need additional funds to meet its near-term obligations.

UDR's high forward PE suggests the stock may be overvalued, which could prevent further price gains and lead to a correction. This parameter should be carefully evaluated in context with other fundamental data to ensure a balanced view.

UDR's elevated debt-to-equity ratio shows that the company is relying heavily on debt to fund its activities. This high leverage can amplify returns but also heightens financial risks if cash flow becomes constrained.

With UDR's forward EPS lower than its trailing EPS, the company is expected to experience a drop in profitability. This suggests a potential slowdown in financial performance compared to the previous year.

Price projections:

Over time, UDR, Inc.'s price projections have steadily declined, reflecting reduced confidence in the company's future performance. The downward revisions suggest analysts are becoming more conservative in their assessments.

Recommendation changes over time:

Analysts have maintained a buy bias for UDR, which could prompt investors to consider the stock as a viable investment. With this positive outlook, UDR is positioned as an attractive option for those looking to park their money in a stable and potentially lucrative company.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst technicals.

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

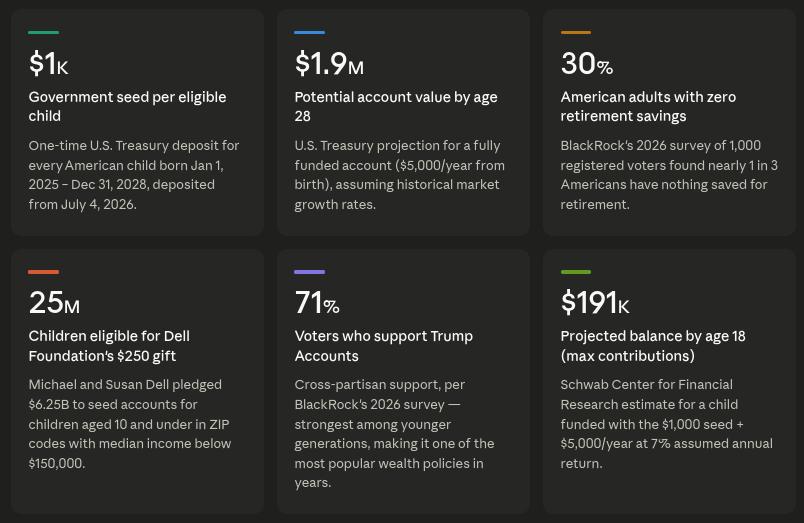

Before They Can Walk, They're Invested: How Trump Accounts Are Transforming Financial Culture

The Appalachian Energy Reboot: Inside the Unexpected Nuclear Startup Boom

Theatrical Finance: Credit Unions Use Drama to Attract Youth