More about Darden Restaurants, Inc.

Regulatory Filings for Darden Restaurants, Inc.

Fundamentals for Darden Restaurants, Inc.

Debt, Deficits & Disaster: The Bond Market Crisis

Not Wall Street, But AI: The Real Force Democratizing Finance Across America

When Flooding Pays: A New Financial Bet

Breakfast for Life How Local Diners and Hardware Stores are Outsmarting Amazon

Fundamentals for Darden Restaurants, Inc.

Business Operations:

Sector: Consumer CyclicalIndustry: Restaurants

Darden Restaurants, Inc., together with its subsidiaries, owns and operates full-service restaurants in the United States and Canada. The company operates under Olive Garden, LongHorn Steakhouse, Cheddar's Scratch Kitchen, Chuy's, Yard House, Ruth's Chris Steak House, The Capital Grille, Seasons 52, Eddie V's Prime Seafood, Bahama Breeze, The Capital Burger, Darden and Darden Restaurants brand names. Darden Restaurants, Inc. was founded in 1938 and is based in Orlando, Florida.

Revenue projections:

With DRI's revenue expected to be lower than the previous year, investors may become cautious. Declining revenues often negatively impact the bottom line, reducing profitability and raising concerns among investors about the company's ability to maintain strong financial performance moving forward.

Financial Ratios:

| currentRatio | 0.387000 |

|---|---|

| forwardPE | 17.640022 |

| debtToEquity | 387.681000 |

| earningsGrowth | -0.033000 |

| revenueGrowth | 0.059000 |

| grossMargins | 0.215070 |

| operatingMargins | 0.131530 |

| trailingEps | 9.490000 |

| forwardEps | 11.369600 |

Darden Restaurants, Inc.'s current ratio being 0.387 suggests that its cash reserves and current assets may not fully cover its short-term debts. This points to potential liquidity problems and could indicate that the company may need to secure additional funds to meet its obligations.

With DRI's Forward PE in a favorable range, the stock appears reasonably priced compared to its earnings. This suggests that it's not overpriced and there is room for growth, providing an encouraging opportunity for investors seeking future value increases.

Darden Restaurants, Inc.'s high debt-to-equity ratio points to a heavily leveraged company, with more debt than equity in its capital structure. While this can boost growth, it increases financial vulnerability in times of economic difficulty.

DRI's low earnings and revenue growth suggest that the company's profits may shrink. This trend could indicate underlying financial struggles and pose challenges for DRI's future profitability.

DRI's negative gross and operating margins point to financial difficulties, as the company is unable to generate profit from its core operations or production. This could signal broader problems in cost management or declining sales.

DRI's forward EPS being higher than its trailing EPS signals anticipated growth in profitability for the current financial year. This suggests that DRI is on track to improve its earnings, outpacing the previous year's performance and reflecting positive market expectations.

Price projections:

DRI's price projections have been revised upward over time, suggesting that analysts are becoming more confident in the company's future. This trend points to increased optimism about DRI's ability to grow.

Insider Transactions:

24 transactions were made to sell DRI shares, with market price of 205.49644660949707.During the review period, no sell transactions were executed.DRI's current price levels are experiencing more buying activity than selling, which may point to a favorable outlook. This trend suggests investor confidence in the stock's future, potentially indicating expectations of continued growth.

Recommendation changes over time:

Analysts' buy bias for DRI signals that the stock is considered a favorable investment. This outlook might prompt investors to allocate funds to DRI, seeing it as a solid and profitable choice to park their money and potentially benefit from the company's long-term growth.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst technicals.

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

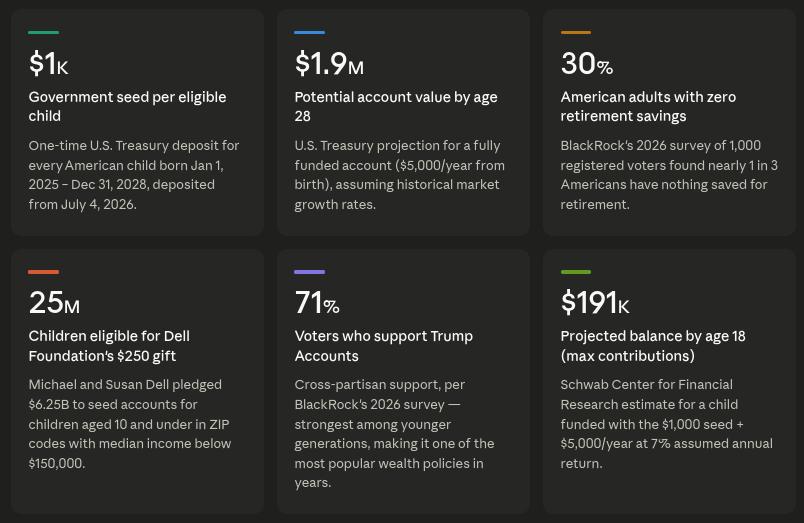

Before They Can Walk, They're Invested: How Trump Accounts Are Transforming Financial Culture

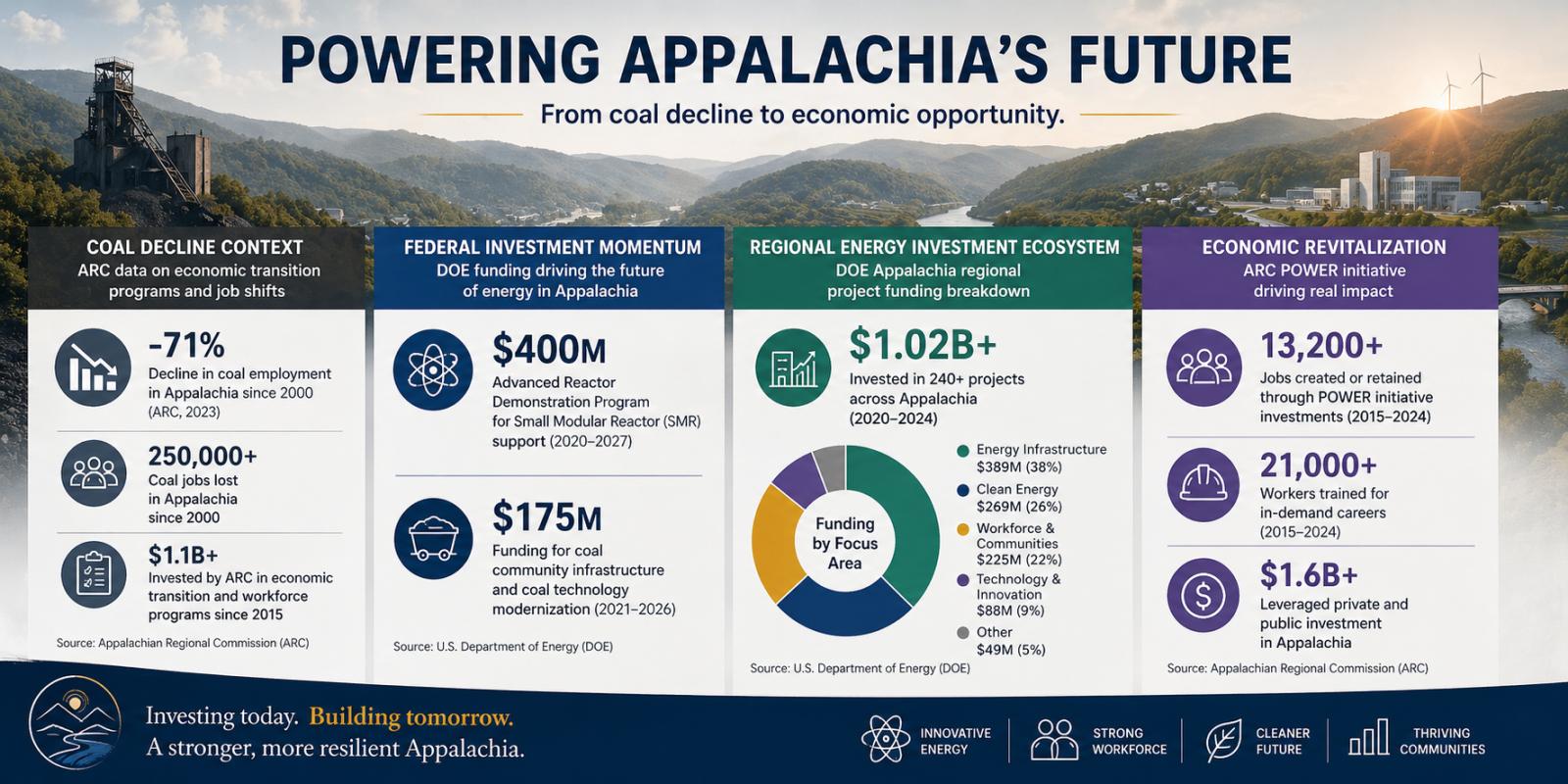

The Appalachian Energy Reboot: Inside the Unexpected Nuclear Startup Boom

Theatrical Finance: Credit Unions Use Drama to Attract Youth