Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

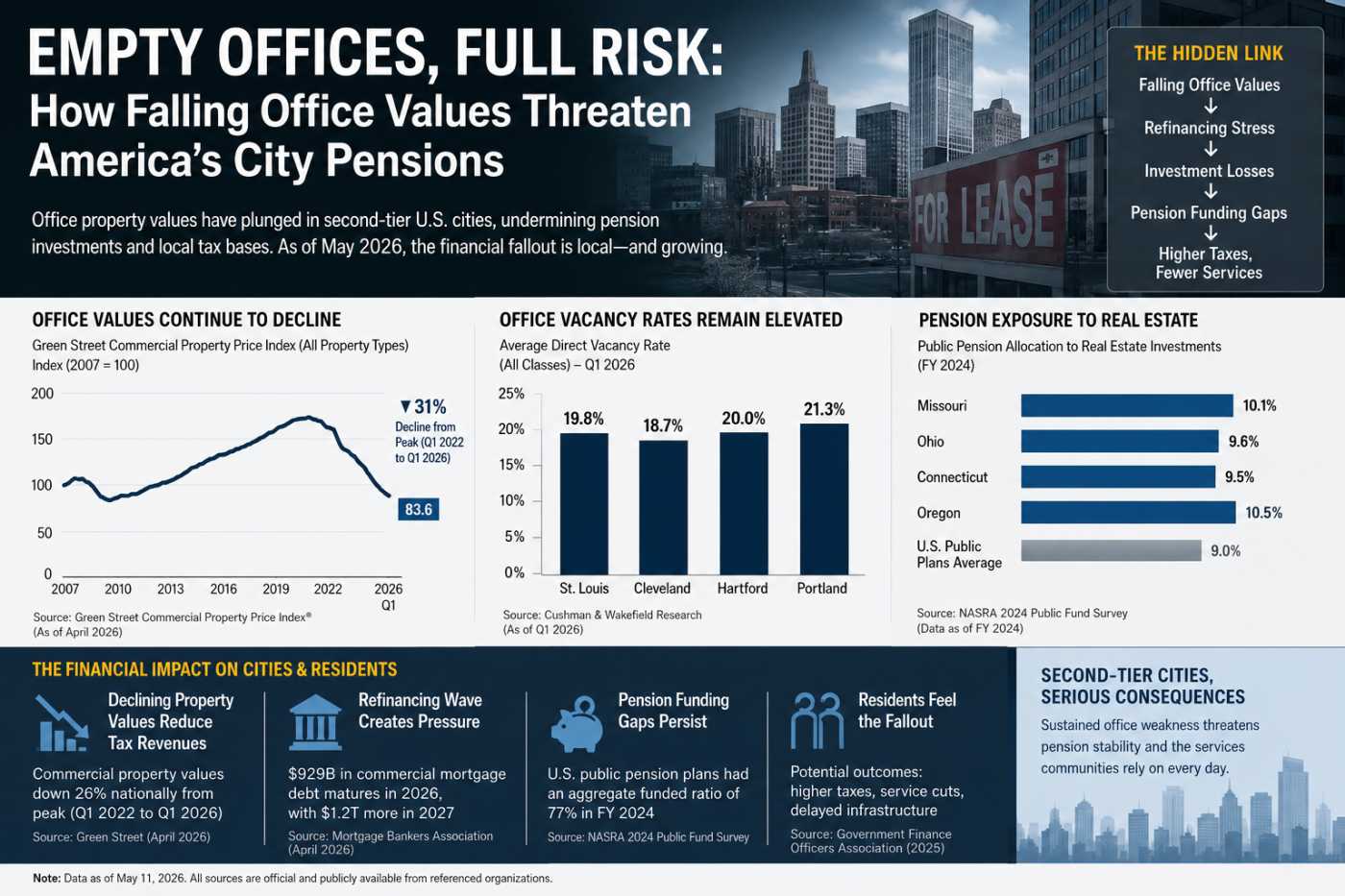

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

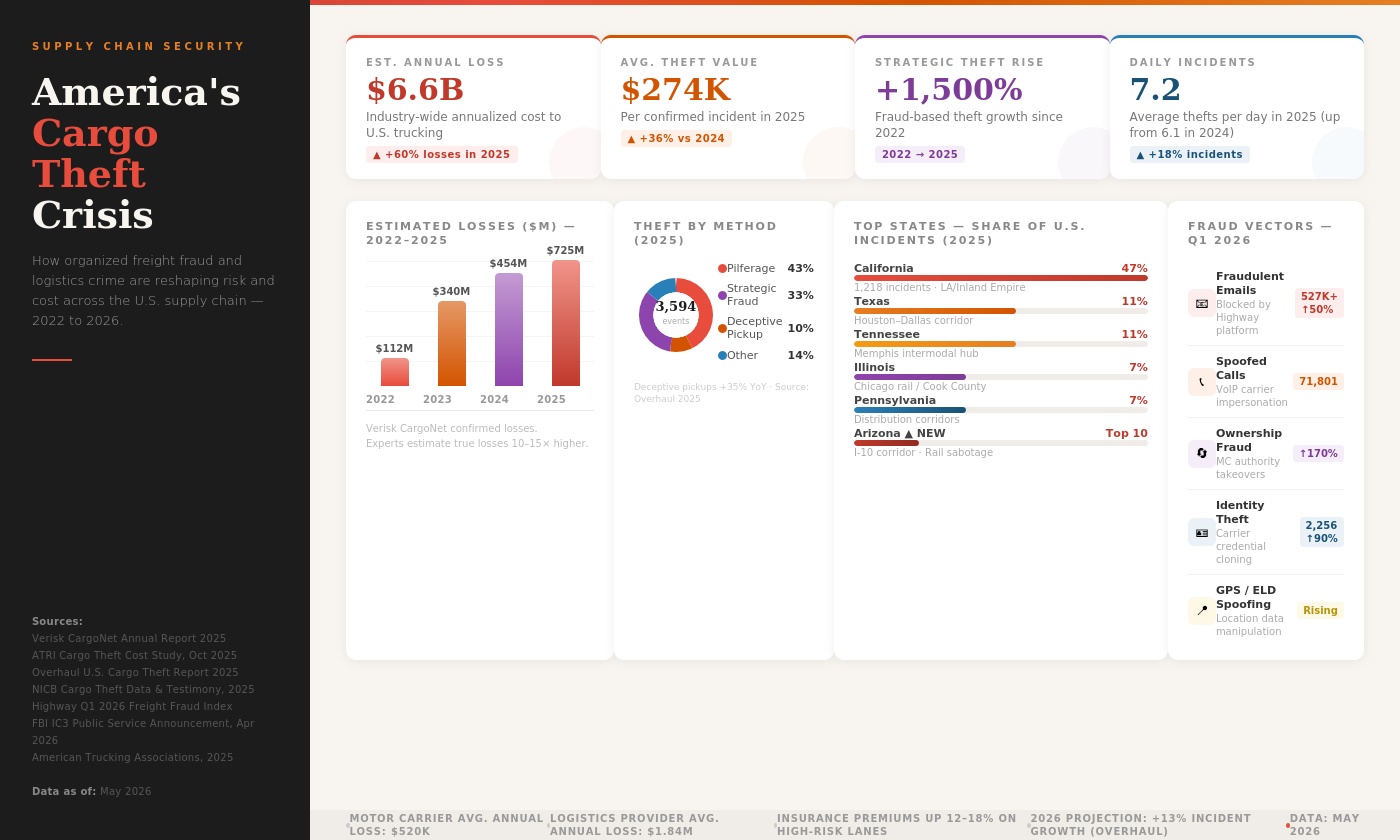

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

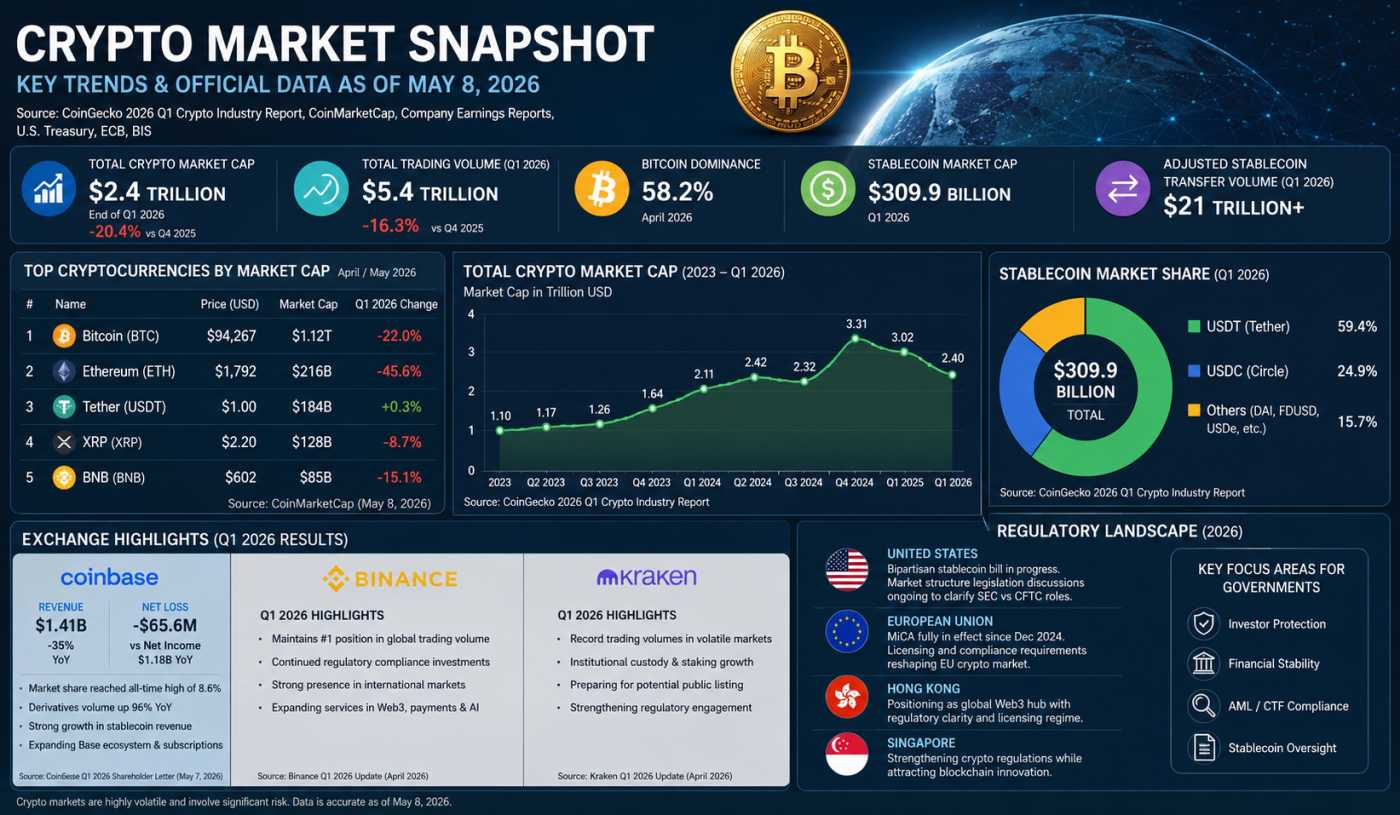

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

America's $5 Trillion Business Handoff Has Already Begun

On a Tuesday morning in February 2026, a 34-page report landed quietly on the desks of economists, small-business advocates, and community development financiers across the United States. Published by the McKinsey Institute for Economic Mobility and authored by Ken Yearwood, Nathan Marks, Shelley Stewart III, and Nick Noel, the document carried a title both clinical and seismic: The Great Ownership Transfer: A New Era of Business Stewardship. Its central finding was straightforward and staggering in equal measure: by 2035, roughly six million small and medium-sized businesses will face ownership transitions, representing up to five trillion dollars in enterprise value the largest generational handoff of private business wealth in modern American history.

The demographic machinery behind this shift has been running for years. Today, more than half of all small-business owners in the United States are over the age of 55, up from roughly 30 percent in 2002, according to U.S. Census Bureau Annual Business Survey data analyzed by McKinsey. One in four small-business owners is 65 or older. In 2005, only 12 percent of the U.S. population was of retirement age. By 2025, that figure had risen to 19 percent. By 2040, it will reach 22 percent. These numbers, taken together, describe not a slow demographic drift but an accelerating structural reality: the people who built America's neighborhood plumbing companies, corner pharmacies, auto repair shops, and HVAC contracting firms are now in the final chapters of their working lives, and the country has not yet built the systems to handle what comes next.

The Real Story Is Not the Crisis It Is the Opportunity

Much of the coverage of this demographic reality has leaned hard into alarm. The phrase "silver tsunami" has become shorthand for an implied catastrophe millions of businesses shuttering, jobs evaporating, communities hollowed out. The framing is not without basis: the McKinsey report found that today, a troubling 92 percent of small-business market exits occur through closure, with only 5 percent completed as sales and 3 percent transferred to new owners. A 2025 Gallup Pathways to Wealth Survey found that 27 percent of employer firms with owners aged 55 and older are either unsure of their long-term plan or intend to close permanently.

But the more instructive frame the one that actually generates solutions is the one that reframes this moment as the largest opportunity for democratic wealth-building the United States has seen in a generation. This is the argument made compellingly by McKinsey's Shelley Stewart III, a senior partner and chair of the McKinsey Institute for Economic Mobility, who said upon the report's release: "This is the largest ownership transition in modern US history. This is a huge opportunity but there is also a challenge the issue is that many viable businesses may not successfully transfer because the market to connect buyers, sellers, and capital is not built at scale."

The contours of that opportunity are striking. If Black, Latino, and women entrepreneurs can meaningfully increase their ownership stake in these transitioning businesses, the McKinsey report calculates this could unlock three trillion dollars in new household wealth. Ownership of a small business has historically been one of the most reliable pathways to wealth creation in the United States more accessible than stock market participation, more locally rooted than venture capital, and more community-sustaining than either. The Great Ownership Transfer, handled well, is not a funeral for the small-business economy. It is an invitation to redistribute its equity more broadly than it has ever been distributed before.

The Demographics of Who Owns and Who Could

The mismatch at the heart of this transition is demographic. Today's small-business owner base is substantially older, less diverse, and more male than the overall American population. More than 70 percent of small-business owners are White, over 60 percent are male, and more than half are over 55, according to McKinsey's analysis of U.S. Census Bureau data. Only 3 percent of U.S. business owners are Black, compared to 13 percent of the Black share of the overall population. Latino and women business owners are similarly underrepresented relative to their share of the working-age population.

This concentration of ownership among an aging, relatively homogeneous cohort means that without deliberate intervention, the default outcome of the Great Ownership Transfer will be closure not community-sustaining succession. According to the McKinsey report, only 28 percent of the ownership transfer value from baby boomer-owned businesses is likely to flow to women and Black and Latino individuals combined, under current trends. That leaves an enormous unlocked potential: a generation of younger, more diverse Americans who are capable of running these businesses, motivated to own rather than merely work, but systematically under-resourced by a succession market that was not designed with them in mind.

The U.S. Bank Small Business Succession Survey of 2025 captured the internal contradiction at the heart of many retiring owners' situations. While 85 percent of surveyed business owners originally became an owner to create something they could pass on, and 84 percent expressed a desire to create generational wealth for their family or community, only 54 percent have a formal succession plan in place. A growing number 62 percent have seen their retirement timelines accelerate over the past five years. Yet 62 percent find the succession process overwhelming, 56 percent worry they will not get a reasonable price when it is time to sell, and 53 percent report lacking the advisors they need to navigate the transition.

The Missing Middle: Where Businesses Are Most Vulnerable

Not all six million businesses facing ownership transitions are equally at risk. The McKinsey report identifies the "missing middle" as the zone of greatest vulnerability: micro and emerging middle-market businesses valued at less than two million dollars. Nearly 80 percent of projected exits fall into this category. These are precisely the businesses that are too small to attract institutional capital or traditional private equity buyers but too consequential to simply disappear. They are, in the words of the McKinsey researchers, "largely invisible to the market" viable, cash-flowing, community-embedded firms that lack neither customers nor competence, but only a pathway to transfer.

The industries most exposed to this risk are exactly the ones that form the connective tissue of American local economies. Construction, automotive services, healthcare (particularly independent pharmacies and home health agencies), food services, and personal care businesses face the highest near-term ownership transition pressure. According to Project Equity, a nonprofit focused on employee ownership, there are 2.9 million businesses in the U.S. owned by individuals aged 55 or older collectively supporting 32.1 million employees, $1.3 trillion in annual payroll, and $6.5 trillion in revenue. These are not abstract statistics. They represent the mechanic who has kept your car running for twenty years, the pharmacist who remembers your family's medication history, the plumber whose phone number you have memorized because you know he will pick up.

The Exit Planning Institute estimates that 73 percent of privately held companies in the U.S. plan to transition ownership within the next decade representing a $14 trillion opportunity in aggregate. Yet nearly two-thirds of family businesses have no documented succession plan, according to PricewaterhouseCoopers' U.S. Family Business Survey. The gap between intention and preparation is not a function of indifference. It reflects structural friction: the market for buying and selling a small business is fragmented, opaque, expensive to navigate, and built almost entirely for sellers rather than buyers.

What Is Actually Working: SBA Loans, Employee Ownership, and the Surge in Acquisitions

The gap between the scale of the problem and the existing infrastructure to address it has begun to generate real market responses. Perhaps the clearest signal of momentum is the surge in SBA-backed acquisition financing. According to Inc. Magazine's February 2026 reporting, citing the Small Business Administration directly, the use of SBA loans to buy companies increased 31 percent year-over-year to $8.8 billion during fiscal year 2025, up from $6.7 billion the prior year. Eric Daniels, who leads SBA lending at U.S. Bank, noted: "We've seen increases in our pipeline on changes of ownership and it's largely because of retirements." This is not a speculative projection. It is a documented, real-time market response to demographic pressure, and it represents a growing recognition that acquisition financing not just startup financing is infrastructure for small-business continuity.

Employee Stock Ownership Plans, or ESOPs, represent another mechanism gaining serious traction as a succession tool for businesses where the retiring owner's deepest instinct is to protect the workforce rather than simply maximize sale price. Currently, over 14 million employees across roughly 6,600 companies participate in ESOPs, with a combined asset value exceeding $1.5 trillion, according to First Bank of the Lake. Research from the National Center for Employee Ownership shows that ESOP-driven companies grow approximately 2.3 to 2.4 percent faster annually than non-ESOP businesses. Employees in ESOP-structured companies often earn 5 to 12 percent more in wages and report dramatically higher job satisfaction 94 percent of workers in ESOP-based organizations report higher satisfaction than in traditional company structures.

The appeal of the ESOP model for the Great Ownership Transfer is intuitive: it allows a retiring owner to exit at fair market value, protects the jobs of the people who built the business, and converts wage earners into wealth-holders in a single transaction. Apis and Heritage Capital Partners, an investment firm focused exclusively on employee ownership conversions, has created more than 1,500 worker-owners across six portfolio companies, with 89 percent of workers in their portfolio classified as low to moderate income at the time of ownership transition. Philip Reeves, Apis and Heritage's cofounder and managing partner, explained the model's impact in a February 2026 interview with the McKinsey Institute for Economic Mobility: "They shift from a wage-earning path to a wealth-building path because they're holding one of the most powerful things in the American economy: equity or an equity-like stake in a growing, profitable, long-standing small business."

SCORE and the Infrastructure of Mentored Succession

Alongside capital, what retiring business owners and their would-be successors consistently lack is structured guidance someone who has been through the transition themselves and can walk alongside both parties through its complexity. SCORE, the nation's largest network of volunteer business mentors and a resource partner of the U.S. Small Business Administration, has served more than 11 million current and aspiring entrepreneurs since its founding in 1964. With over 10,000 volunteers operating through more than 230 local chapters, SCORE provides free, confidential mentoring to business owners at every stage of their lifecycle including succession planning and exit. Its model is instructive precisely because it is relational: not a transaction facilitated by a platform algorithm, but a sustained human advisory relationship between someone who has built and owned a business and someone who is learning how.

The case for mentored succession where a retiring owner invests time in genuinely preparing a successor rather than simply finding the highest bidder rests on both economic and social grounds. Economically, a prepared successor is far more likely to maintain the customer relationships, operational standards, and community reputation that give a small business its value. Socially, mentored succession is the mechanism through which tacit knowledge the kind that cannot be captured in a manual or a balance sheet, the institutional memory that makes a local business indispensable is actually transmitted. When Connie and Paul Estey founded Seawalk Florals, they worked with a SCORE mentor at every step, from early financial management to expansion decisions. Stories like this, replicated across hundreds of industries and thousands of communities, represent a form of wealth transfer that balance sheets do not fully capture.

The Wealth Transfer That Does Not Make Headlines

What the numbers ultimately point toward is a kind of wealth transfer that has received far less attention than the much-discussed intergenerational financial inheritance of boomer-to-millennial household wealth. When a retiring HVAC contractor in rural New Mexico, a third-generation auto body shop owner in suburban Ohio, or an independent pharmacist in a small Mississippi town successfully transfers her business to a younger, well-prepared successor especially one who is a woman, a first-generation American, or a member of a community historically excluded from business ownership something economically significant happens. A stream of cash flow that would have evaporated in a closure is preserved. A set of customer relationships that took decades to build continues to serve the community. A local employer remains local. And a younger person who might otherwise have spent their career building equity for someone else's business begins building it for their own.

The McKinsey report is explicit about the stakes: "Ownership of a small business has long been one of the most powerful pathways to wealth creation in the United States." A coordinated transition market built on standardized financing tools, accessible advisory services, mentorship networks, and more inclusive underwriting could, the report estimates, preserve up to 12 million jobs and $250 billion in annual local spending power. These are not small numbers. They represent the difference between communities that remain economically coherent and those that hollow out when the generation that built them retires.

The good news, understated in most coverage of this issue, is that the pieces of a functioning succession market already exist. The SBA's 7(a) loan program, though imperfect and in need of modernization, is already funding billions in business acquisitions annually. ESOPs, despite administrative complexity, are creating worker-owners at a meaningful scale. SCORE's mentorship network has helped tens of millions of business owners navigate decisions exactly like this one. New online platforms BizBuySell, MicroAcquire, Baton are beginning to reduce the opacity that makes small-business transactions so hard to initiate. The question, as McKinsey's researchers put it, is whether these tools can be brought to scale in time, and whether they can be made accessible to the buyers who have the most to gain from them and the least support in reaching them.

The Great Ownership Transfer is not, at its core, a story about aging. It is a story about what kind of economy America wants to build for the next generation who gets to own it, who gets to profit from it, and whether the businesses that give local communities their character and economic resilience survive the transition or quietly close because the systems that should have caught them were not yet in place. The choice, and the urgency of making it, belongs to this moment.

If you have enjoyed reading, spread the word:

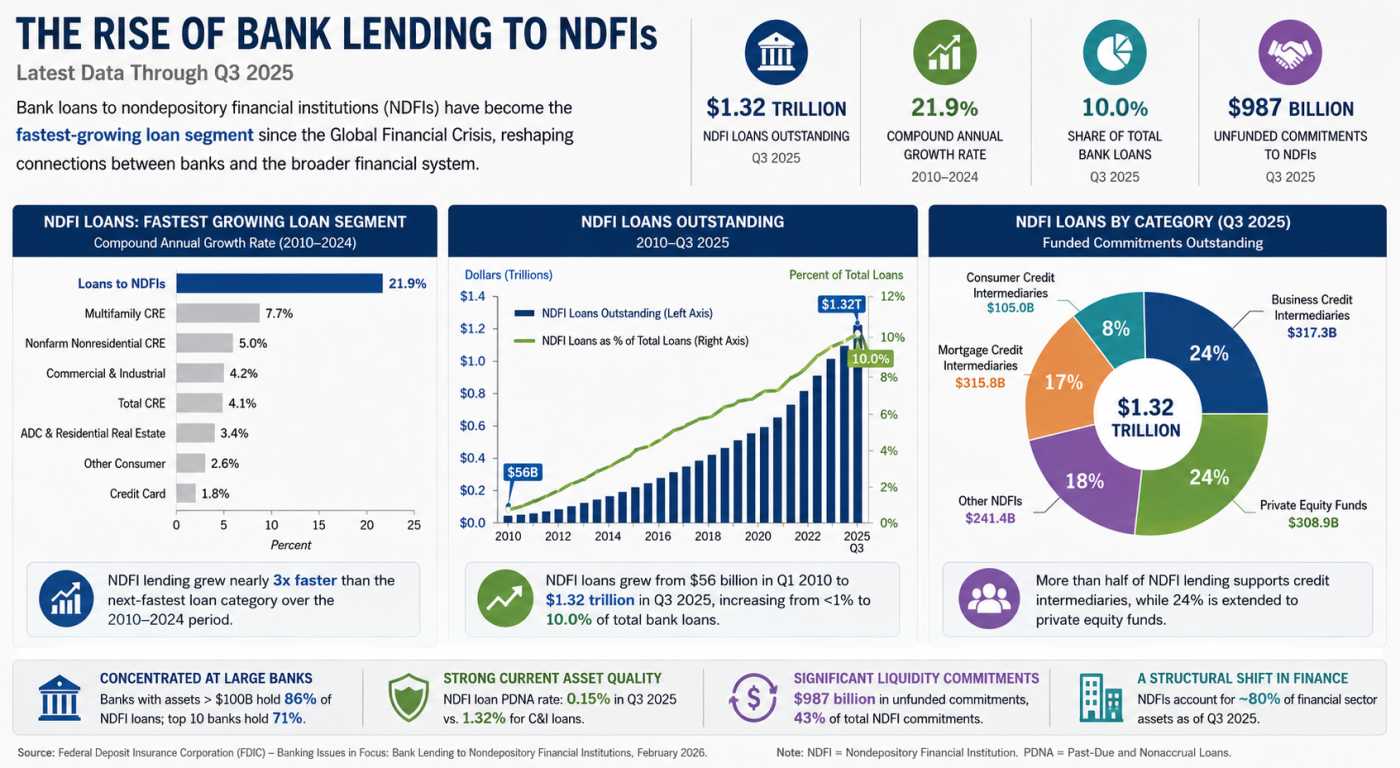

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America

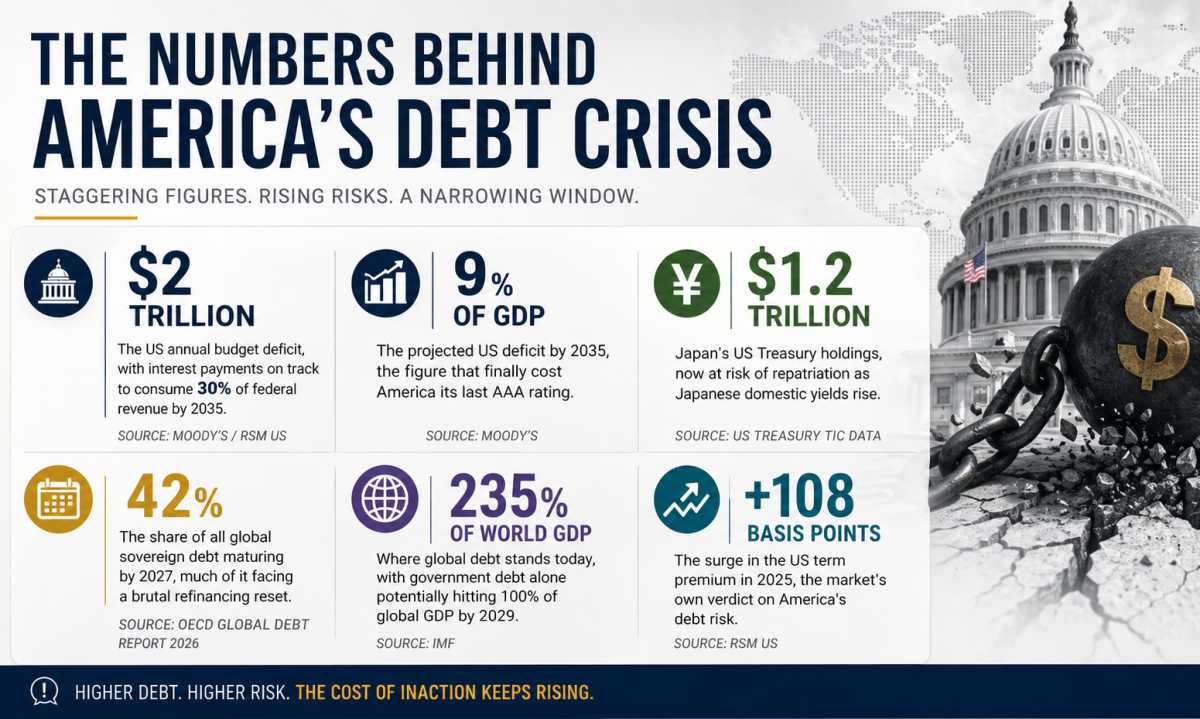

Debt, Deficits & Disaster: The Bond Market Crisis