Good prospects:

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

Apollo FY26: When Healthcare Becomes a Flywheel

NITI Blueprint Could Turn Brain Drain Into $135Bn Engine

RAINMUMBAI Turns Rain Into a Financial Asset

India’s IT Sector Faces a Historic Breaking Point

How Independent Directors Failed Rs 2,500 Crore in Value

Why Gujarat And Rajasthan Are Winning Big

India's Quiet Power Revolution Is Moving West

For much of the last decade, India's renewable energy story was framed around scale: record-breaking solar parks, falling tariffs, and ambitious national targets. Yet in 2026, one of the country's most consequential infrastructure shifts is unfolding with far less public attention. Across Rajasthan and Gujarat, a new generation of Firm and Dispatchable Renewable Energy (FDRE) projects is beginning to change how electricity itself is produced, stored, traded and consumed.

Unlike conventional solar farms that generate only during daylight hours, FDRE projects combine solar power, wind generation and large-scale Battery Energy Storage Systems (BESS) into integrated networks capable of delivering electricity during peak demand periods. These systems are designed not merely to generate clean power, but to behave more like dependable conventional generation.

The significance of this transition extends far beyond the renewable energy sector. Industrial electricity pricing, manufacturing competitiveness, data center economics, freight electrification, transmission infrastructure and even local employment structures are beginning to shift around these projects. In states such as Rajasthan and Gujarat, which already dominate India's renewable energy landscape, FDRE infrastructure is rapidly becoming a foundational economic asset.

According to data published by the Union Ministry of New and Renewable Energy and reported by The Times of India in May 2026, Gujarat overtook Rajasthan in overall renewable energy capacity with more than 47 GW installed. Rajasthan, however, continues to lead in solar generation capacity with over 41 GW installed. Together, the two states have become the core geography for India's next-generation renewable transition.

Why FDRE Matters More Than Traditional Solar

India's first wave of renewable expansion successfully reduced generation costs, but it also exposed structural weaknesses. Solar output peaks during midday hours, while electricity demand in India often surges during evenings due to air-conditioning loads, industrial shifts and urban consumption patterns. Wind generation, meanwhile, remains seasonal and variable.

FDRE systems are intended to solve this mismatch.

In April 2026, Juniper Green Energy began commissioning India's first operational FDRE project under the Ministry of Power's 2023 guidelines. According to reporting by pv magazine India and SolarQuarter, the project combines 259 MWp of solar capacity, 280 MW of wind power and a 200 MWh battery storage system distributed across Rajasthan and Gujarat.

The project is notable not only for its size, but for what it represents operationally. The integrated system is designed to provide scheduled renewable electricity aligned with grid demand rather than merely injecting variable power whenever generation conditions are favorable.

The Ministry of Power's FDRE framework effectively signals that India's renewable market is transitioning from a pure generation race into a reliability-driven market. This is a critical distinction because industrial consumers increasingly care less about the lowest theoretical tariff and more about predictability, uninterrupted supply and hedging against volatile energy prices.

Industrial Electricity Economics Are Changing

For energy-intensive industries, electricity volatility has become a growing operational risk. Sectors such as ceramics, aluminum processing, specialty chemicals, steel rolling, textiles and semiconductor fabrication depend on highly stable power quality. Even brief fluctuations can damage equipment or disrupt production cycles.

Historically, many industrial clusters in western India relied on a combination of grid electricity, diesel backup generation and captive thermal power. That model is becoming increasingly expensive.

Battery-integrated renewable systems are now starting to alter the economics of industrial electricity procurement. By combining solar generation during daylight hours with stored battery power during evening peaks, FDRE projects allow large consumers to reduce exposure to expensive peak-time grid tariffs.

This has particular implications for Gujarat's industrial economy. The state's chemical manufacturing clusters, refinery operations, pharmaceutical parks and ceramics industry collectively represent some of India's most electricity-intensive manufacturing activity.

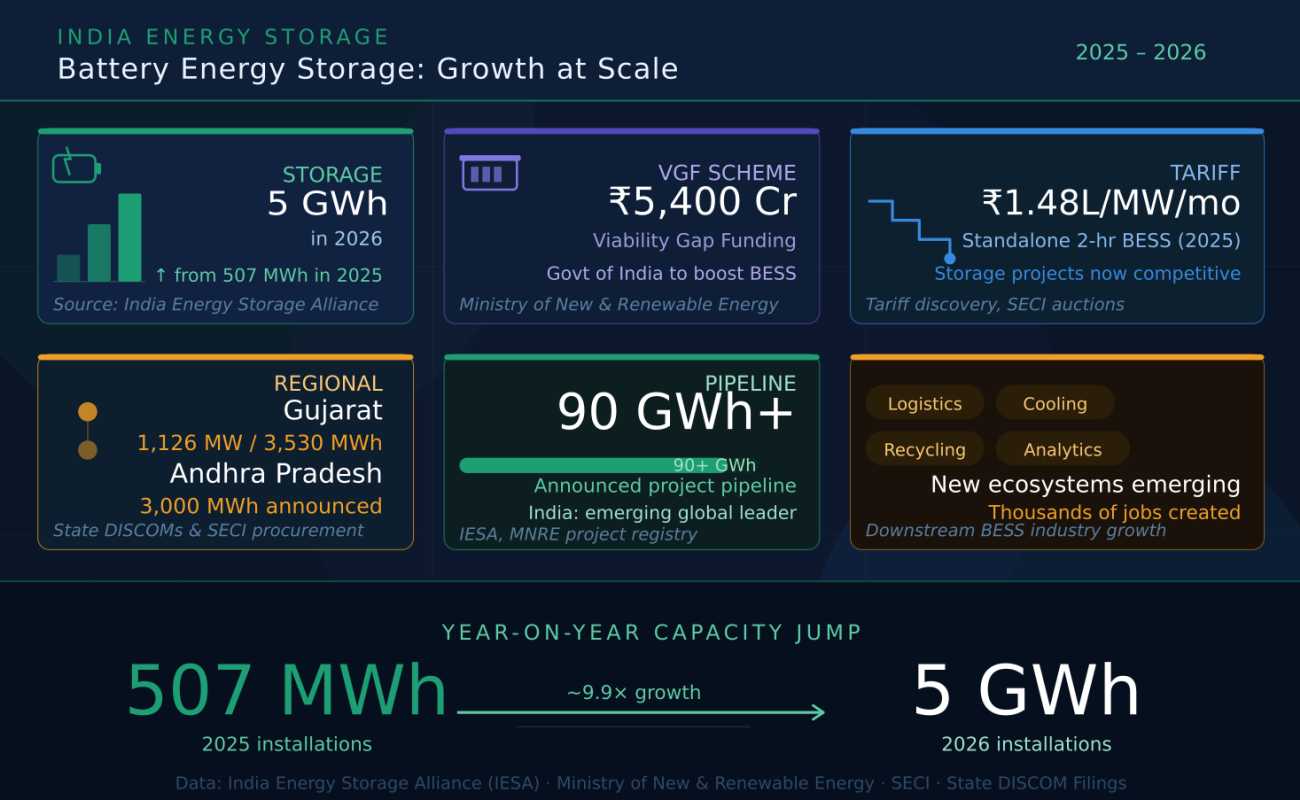

The Gujarat Electricity Regulatory Commission recently approved a large standalone BESS allocation pipeline through Gujarat Urja Vikas Nigam Limited (GUVNL). According to EnergyStorage Pro, Gujarat's Phase VIII standalone battery storage auction alone covered 335 MW and 670 MWh of storage capacity, while the state has approved a broader 2,000 MW and 4,000 MWh pipeline.

Industry analysts increasingly view these storage assets not as emergency backup systems, but as long-duration economic infrastructure capable of reducing marginal power costs over time.

There is also a growing realization among industrial buyers that renewable-plus-storage systems can act as an inflation hedge. Coal price volatility, imported LNG fluctuations and transmission bottlenecks have repeatedly affected industrial electricity costs over the past several years. Long-duration renewable procurement contracts paired with storage offer manufacturers greater visibility over future energy expenses.

Data Centers Are Becoming Major Drivers of Dispatchable Renewables

India's AI and cloud computing expansion is creating another powerful demand center for FDRE infrastructure. Data centers require uninterrupted electricity availability with extremely low tolerance for outages or voltage instability.

In March 2026, the Gujarat government signed a memorandum of understanding with L&T Vyom for a 250 MW green AI-ready data center campus in Dholera Special Investment Region. According to reporting by The Times of India, the proposed investment could exceed Rs 25,000 crore.

Projects of this scale fundamentally change local electricity demand patterns. AI-focused data centers consume large amounts of continuous electricity, particularly during cooling-intensive periods. Traditional intermittent renewables are insufficient for these requirements unless paired with storage or balancing systems.

This is where FDRE architecture becomes commercially important. Solar generation can provide low-cost daytime electricity, wind can support nighttime supply, and batteries can smooth frequency fluctuations while ensuring reliability during high-demand intervals.

India's data center expansion is therefore becoming tightly linked to western India's renewable infrastructure buildout. Dholera, Khavda, Mundra and neighboring industrial corridors are increasingly being positioned as integrated ecosystems combining renewable generation, storage capacity, transmission infrastructure and digital infrastructure.

This convergence is significant because it turns renewable energy from a climate policy initiative into a core industrial competitiveness strategy.

Rail Electrification and Peak Power Management

India's railway electrification program is another underappreciated driver behind dispatchable renewable energy demand. Indian Railways has been aggressively pursuing renewable procurement agreements as part of its decarbonization targets.

Unlike urban residential demand, railway power consumption follows predictable operational cycles. This creates favorable conditions for dispatchable renewable supply contracts. FDRE systems can theoretically align battery discharge windows with freight movement peaks and high-demand operational corridors.

Large-scale storage deployment could also help stabilize grid conditions in regions where electrified rail corridors intersect with renewable-heavy generation zones.

For Rajasthan and Gujarat, which already host major freight and industrial corridors linked to ports, logistics hubs and manufacturing zones, this integration could create long-term infrastructure advantages.

The Transmission Infrastructure Challenge

Despite the optimism surrounding FDRE projects, the transition is not without significant structural risks.

Transmission remains one of the biggest bottlenecks in India's renewable expansion. Rajasthan and Gujarat possess vast solar and wind resources, but generation capacity alone does not guarantee reliable electricity delivery to industrial demand centers.

Battery storage partly addresses this problem by reducing immediate evacuation pressure and enabling load shifting. However, long-term growth still depends on transmission expansion.

The scale of upcoming projects illustrates the challenge. In February 2026, ACME Solar secured a 301 MW FDRE project integrated with 1,204 MWh of storage under SECI's FDRE-VII tender. Serentica Renewables separately won a massive 600 MW allocation involving 2,400 MWh of daily peak power delivery obligations.

These projects are significantly more complex than traditional solar parks because they require coordination across multiple generation sources, storage assets and transmission nodes simultaneously.

Grid balancing itself is becoming a more technologically sophisticated activity. Advanced forecasting systems, AI-driven energy management software and predictive dispatch modeling are now increasingly important components of renewable infrastructure.

This creates new opportunities for Indian software firms, industrial automation companies and energy analytics startups.

Battery Manufacturing Is Emerging as a Strategic Industrial Layer

India's FDRE expansion is also accelerating the country's battery manufacturing ambitions.

Battery storage is rapidly shifting from a niche energy technology into a strategic industrial sector with implications for automotive manufacturing, defense electronics, power infrastructure and export competitiveness.

Several companies are now scaling local manufacturing plans in response to India's storage demand growth. According to reporting by The Times of India in April 2026, Shanghai-based Sigenergy is evaluating investments between $150 million and $200 million for battery and inverter manufacturing facilities in India, with Gujarat among the states under consideration.

Meanwhile, domestic players including Adani, Waaree and Tata Group-linked battery ventures are expanding storage-related operations across western India.

This matters because battery storage deployment creates a broader industrial ecosystem extending far beyond cell manufacturing. Cooling systems, thermal management equipment, inverter manufacturing, battery management software, recycling infrastructure and specialty chemicals all become part of the supply chain.

For Rajasthan and Gujarat, this creates opportunities for localized industrial clustering similar to what China achieved in solar manufacturing over the previous decade.

The transition also aligns with India's broader production-linked incentive strategies and import substitution goals. Although India remains heavily dependent on imported lithium and several battery minerals, policymakers increasingly see integrated battery manufacturing as essential to long-term energy security.

Local Employment Patterns Are Quietly Changing

FDRE projects are also beginning to alter employment dynamics in western India's rural districts.

Traditional solar parks generated substantial construction employment but relatively limited long-term operational jobs. Battery-integrated renewable systems, however, are more operationally intensive.

Storage systems require continuous monitoring, software optimization, thermal management and predictive maintenance. This creates demand for higher-skilled technical labor across districts that historically depended on agriculture or low-productivity informal employment.

Districts near Khavda, Barmer, Jaisalmer and Kutch are increasingly attracting engineering contractors, logistics operators, industrial service providers and energy technology specialists.

Battery storage also changes land economics. Unlike purely seasonal renewable generation, dispatchable systems increase the strategic value of land connected to high-capacity transmission infrastructure. This is already influencing industrial planning decisions around western India's renewable corridors.

At the same time, concerns remain regarding land acquisition, ecological impacts in desert ecosystems and water usage associated with industrial expansion.

Still, the broader trend is clear: renewable infrastructure is evolving from isolated generation assets into integrated industrial ecosystems.

India's Green Manufacturing Ambition Is Becoming More Realistic

Perhaps the most important implication of Rajasthan and Gujarat's FDRE expansion is geopolitical rather than purely domestic.

Global manufacturers increasingly want low-carbon industrial supply chains. European carbon border adjustment mechanisms, sustainability reporting requirements and investor pressure are steadily changing sourcing behavior across industries.

For India, reliable renewable electricity is no longer simply an environmental target. It is becoming a prerequisite for competing in future manufacturing supply chains.

Dispatchable renewable infrastructure improves India's ability to attract energy-intensive industries including semiconductor assembly, green hydrogen production, specialty chemicals, AI infrastructure and export-oriented manufacturing.

Western India's combination of renewable resources, port connectivity, industrial corridors and large-scale storage deployment is therefore creating conditions for a potentially powerful manufacturing advantage.

The infrastructure story unfolding across Rajasthan and Gujarat in 2026 may ultimately matter less because of climate symbolism and more because it is quietly reshaping the economics of industrial India itself.

If you have enjoyed reading, spread the word:

India’s Stock Market May Be Sitting on a Trap

Beyond Sugar: India's Bio-Economy Bets Big on Biofuel

MSMEs & Corridors: India's New Economic Engine

India's Grid-Scale Storage Revolution 2026