Good prospects:

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

India’s IT Sector Faces a Historic Breaking Point

How Independent Directors Failed Rs 2,500 Crore in Value

India’s Stock Market May Be Sitting on a Trap

Beyond Sugar: India's Bio-Economy Bets Big on Biofuel

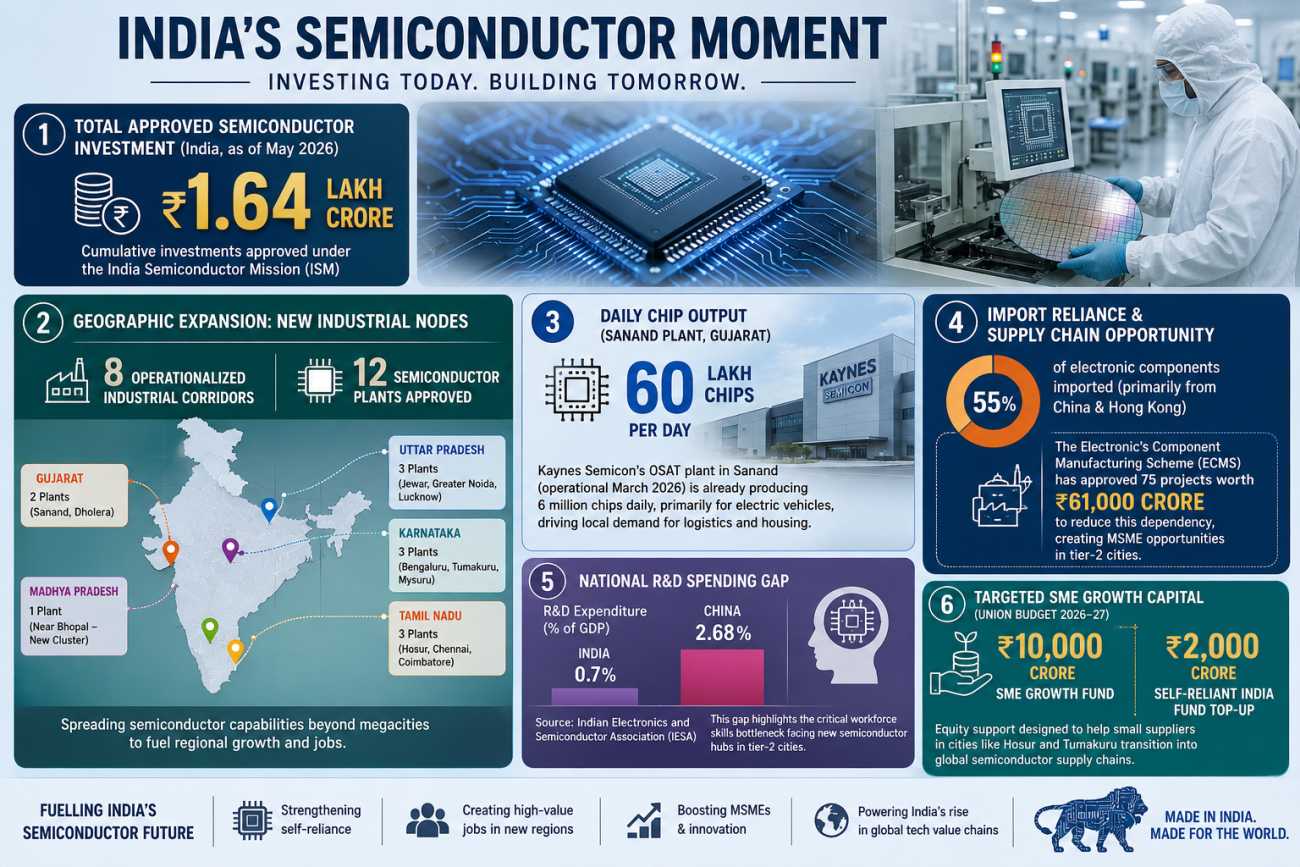

MSMEs & Corridors: India's New Economic Engine

RAINMUMBAI Turns Rain Into a Financial Asset

The Monsoon Is Becoming a Tradable Asset

For generations, India’s economy has depended on the monsoon in ways few other major economies depend on a single climatic event. Nearly half of India’s farmland remains rain-fed, hydroelectric output fluctuates with reservoir levels, food inflation rises and falls with rainfall patterns, and urban infrastructure systems in cities like Mumbai can be crippled within hours by unusually heavy precipitation. Yet despite this enormous economic exposure, India has historically lacked a regulated financial instrument capable of converting rainfall uncertainty into hedgeable market risk.

That is about to change.

On June 1, 2026, the National Commodity & Derivatives Exchange (NCDEX) will launch RAINMUMBAI, India’s first SEBI-approved exchange-traded weather derivatives contract. Developed in partnership with IIT Bombay and built using more than 30 years of rainfall data from the India Meteorological Department (IMD), the product represents far more than another futures contract. It is effectively the birth of a climate-linked financial asset class for India’s economy.

The timing is unusually significant. India’s meteorological authorities have projected the country’s first below-average monsoon in three years, raising concerns around agricultural output, food inflation, power generation and rural demand. Reuters reported on May 20, 2026 that the contract is specifically designed to help businesses hedge against financial disruptions linked to rainfall variability in Mumbai’s monsoon season.[1]

NCDEX Managing Director and CEO Arun Raste described the development succinctly when announcing the launch: “India has lived with monsoon uncertainty for centuries. RAINMUMBAI provides every stakeholder with a regulated, scientific tool to manage this uncertainty.”

In practical terms, India is beginning to financialize weather risk.

How the RAINMUMBAI Contract Actually Works

Unlike traditional commodity futures tied to wheat, crude oil or gold, RAINMUMBAI does not represent ownership of a physical asset. Instead, it tracks deviations in rainfall from a historical norm.

The contract is based on a metric called the Cumulative Deviation Rainfall (CDR) index. The model measures how actual rainfall diverges from the long-term historical average over the monsoon season. Using decades of IMD rainfall observations, IIT Bombay helped design a framework capable of standardizing monsoon variability into an index suitable for derivatives trading.

The contract is cash-settled, meaning no physical delivery occurs. Traders do not receive water or rainfall rights. Instead, payouts occur based on whether cumulative rainfall deviates above or below predetermined benchmarks.

At its core, the product transforms weather from an uncontrollable operational hazard into a measurable financial variable.

That distinction matters because India’s existing climate risk tools remain fragmented and reactive. Crop insurance schemes often suffer from delayed claim settlements, complex verification procedures and inadequate coverage. Government relief packages typically arrive after damage has already occurred. RAINMUMBAI instead introduces continuous price discovery for climate risk itself.

In effect, the market begins assigning a tradable value to rainfall uncertainty.

Why Mumbai Was Chosen First

Mumbai may initially appear like an unusual starting point for a weather derivative in an agriculture-heavy economy. But from a financial engineering perspective, the city makes strategic sense.

Mumbai experiences one of the world’s most economically disruptive monsoon systems. Flooding routinely halts transportation, construction, logistics operations and commercial activity. Localized rainfall shocks can create immediate financial losses across multiple sectors simultaneously.

Unlike broader nationwide rainfall data, Mumbai’s weather patterns are relatively concentrated, data-rich and continuously monitored. This creates a more stable foundation for a benchmark index.

There is also symbolic significance. By anchoring India’s first weather derivative to Mumbai the country’s financial capital NCDEX is effectively signaling that climate risk is now part of mainstream financial infrastructure rather than merely an agricultural concern.

According to NCDEX’s product communication, the contract is intended for industries ranging from logistics and infrastructure to banking and power generation. This broad applicability may ultimately matter more than the agricultural angle itself.

The Real Beneficiaries Extend Far Beyond Farmers

Public discussion around weather derivatives often focuses almost exclusively on farmers. While agriculture is an obvious beneficiary, the more transformative impact may occur elsewhere in India’s financial system.

Consider construction companies operating in western India. Heavy monsoon variability can delay projects by weeks or months, raising labor costs, financing expenses and penalty liabilities. A rainfall hedge allows firms to partially offset these disruptions through financial gains on weather positions.

Power utilities face another major exposure. Hydropower generation depends heavily on reservoir inflows, while thermal utilities simultaneously experience fluctuating electricity demand due to weather-related cooling requirements. Monsoon weakness can also increase reliance on expensive imported coal or LNG.

Logistics firms operating across ports, highways and urban delivery networks similarly encounter major monsoon-linked disruptions. Excess rainfall can slow freight movement, damage infrastructure and increase fuel consumption.

Retail businesses are also more exposed than commonly understood. Weak monsoons often depress rural incomes, affecting everything from two-wheeler sales to consumer goods demand. Weather derivatives provide a mechanism to hedge macroeconomic spillovers previously considered impossible to insure directly.

Even tourism and hospitality operators may eventually participate in weather-linked markets as contracts expand geographically.

In advanced financial systems, weather derivatives have historically been used by airlines, energy traders and utilities. India’s version could evolve into something broader because of the economy’s unusually deep dependence on monsoon behavior.

Banks May Become the Biggest Long-Term Users

Perhaps the most underappreciated implication of RAINMUMBAI lies in banking and credit markets.

Indian banks collectively carry enormous indirect exposure to rainfall variability through agricultural and rural lending portfolios. A deficient monsoon does not merely reduce crop output; it affects repayment capacity, rural consumption and non-performing asset trends across entire regions.

Historically, banks have managed this risk crudely through provisioning buffers and government restructuring programs. Weather derivatives introduce the possibility of dynamic balance-sheet hedging.

A bank heavily exposed to agricultural lending in a rainfall-sensitive region could theoretically use weather futures to offset part of the credit deterioration caused by weak monsoons.

This matters because climate volatility is increasingly becoming a systemic banking risk rather than a localized agricultural problem.

If the market deepens, derivatives pricing could eventually influence how banks assess agricultural creditworthiness itself. Regions with high rainfall volatility may face different lending spreads, collateral requirements or insurance costs.

That creates a potentially profound shift: climate variability begins entering financial pricing mechanisms directly.

Insurance companies may also use weather futures to hedge exposure arising from crop insurance payouts. Instead of bearing purely actuarial risk, insurers gain access to tradable climate-linked instruments that improve capital efficiency.

Over time, this could help create secondary markets for climate-linked risk transfer in India.

The Emergence of a Climate Economy Asset Class

Globally, weather derivatives are not new. The Chicago Mercantile Exchange (CME) has long offered temperature and weather-linked products tied to heating degree days, cooling degree days and snowfall measurements.

But India’s case is structurally different because monsoon variability sits at the center of national economic performance.

The southwest monsoon influences food inflation, rural demand, GDP growth, water security and fiscal spending. According to multiple Reserve Bank of India studies over the years, monsoon shocks have historically transmitted directly into inflationary pressures and consumption trends.

What NCDEX is effectively doing is creating a mechanism through which investors can express views on climate-linked economic outcomes.

That opens the door to an entirely new category of financial products.

Future weather derivatives could potentially expand beyond Mumbai into regional rainfall contracts tied to agricultural belts, reservoir levels or even heatwave intensity. Eventually, India could see climate-linked structured products, insurance-linked securities or ESG-oriented investment vehicles built atop weather indexes.

In developed markets, carbon markets became a major financial asset class over the past two decades. India may now be taking early steps toward building a parallel climate-risk derivatives ecosystem.

The implications for institutional finance are substantial.

Why the Timing Is Especially Critical in 2026

The launch would have attracted attention under any circumstances. But 2026’s monsoon outlook makes the debut particularly consequential.

India recently projected below-average monsoon rainfall for the first time in three years, intensifying concerns around food prices and rural growth. Reuters noted that the weaker monsoon forecast has already raised concerns regarding farm output and broader economic momentum in Asia’s third-largest economy.[1]

This comes at a delicate moment for India’s macroeconomy.

Food inflation remains politically sensitive. Reservoir levels in several regions have shown volatility over recent years due to uneven precipitation patterns. Power demand continues rising as industrialization and urban cooling needs accelerate. Meanwhile, climate change is increasing the frequency of extreme rainfall events even when aggregate seasonal rainfall appears normal.

Traditional risk-management frameworks are struggling to keep pace with these nonlinear climate shocks.

RAINMUMBAI therefore arrives not merely as a financial innovation, but as an institutional adaptation to climate uncertainty.

There is also a deeper strategic logic at work. India’s financial regulators and exchanges are increasingly attempting to broaden domestic market sophistication beyond conventional equity and commodity products.

NCDEX itself has been positioning for expansion into broader financial infrastructure initiatives. Earlier in 2026, the exchange announced plans involving equity-market technology development and mutual fund transaction infrastructure, signaling ambitions beyond agricultural commodities.

Weather derivatives fit neatly into this larger institutional evolution.

The Challenge: Liquidity and Market Education

The biggest immediate risk is not regulatory approval or technology execution. It is liquidity.

Weather derivatives globally have historically struggled when participation remains too narrow. For a climate-risk market to function efficiently, it requires a mix of hedgers, speculators, institutions and arbitrage participants.

If participation remains limited primarily to agricultural users, pricing may remain inefficient and volumes thin.

India also faces a major financial literacy hurdle. Many businesses exposed to monsoon volatility may not yet fully understand how weather-linked hedging instruments work. Smaller firms especially may lack treasury expertise needed to integrate derivatives into operational risk management.

There is also basis risk. A Mumbai rainfall index may not perfectly correlate with specific operational losses experienced by individual firms. That gap between index performance and real-world exposure can limit hedging effectiveness.

Still, these are normal challenges for any emerging derivatives market.

More importantly, the institutional architecture now exists.

For the first time, India’s financial system has a regulated exchange-traded instrument explicitly designed to convert climate variability into tradable market risk.

That changes the conversation entirely.

As climate volatility intensifies over the coming decades, the ability to price, hedge and transfer weather risk may become as economically important as interest-rate hedging or currency management.

India’s economy has always depended on the monsoon. Beginning June 2026, the monsoon will also have a futures market.

Sources:

Reuters report on RAINMUMBAI launch, reporting by Rajendra Jadhav

Economic Times coverage of NCDEX weather derivatives, reporting by Veer Sharma and Sutanuka Ghosal

PTI and Upstox summary of product details

If you have enjoyed reading, spread the word:

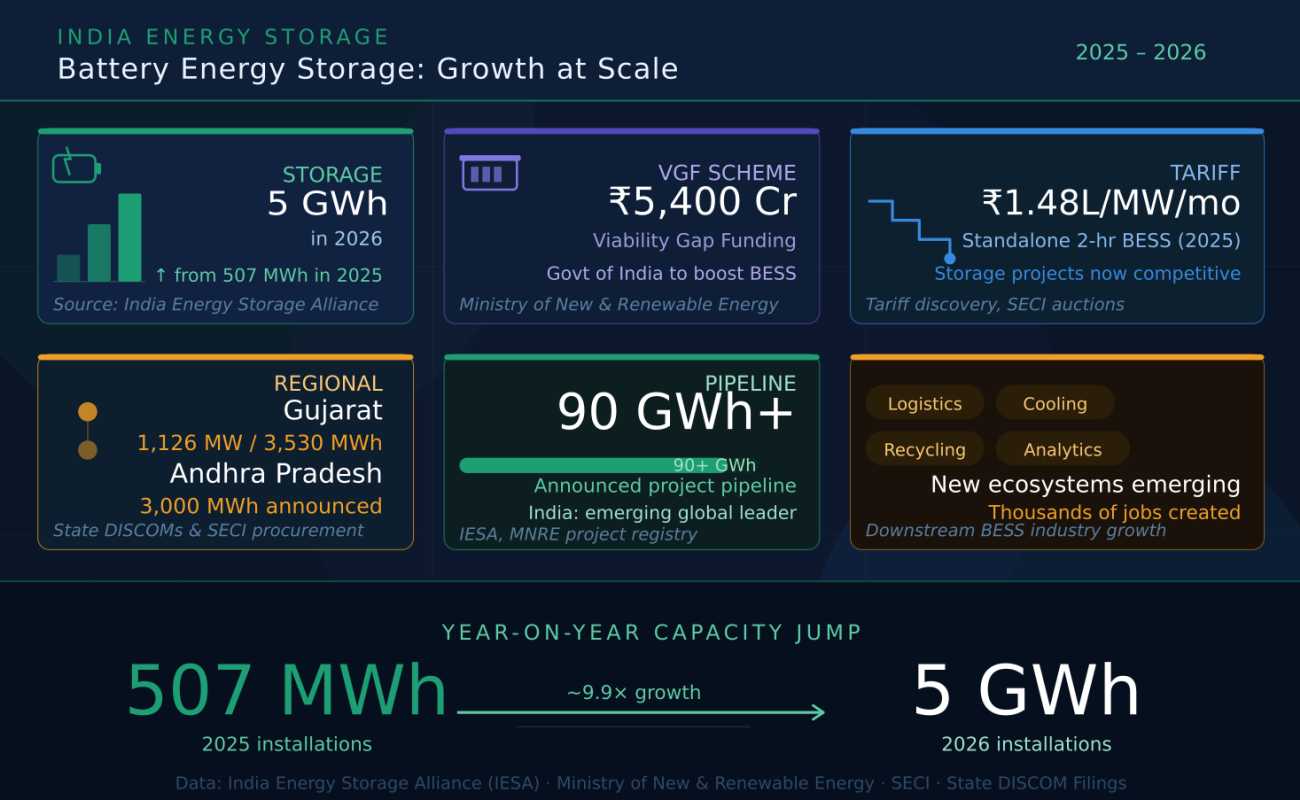

India's Grid-Scale Storage Revolution 2026

Why Gujarat And Rajasthan Are Winning Big

Tier-2 Cities Are Now India's Financial Powerhouses

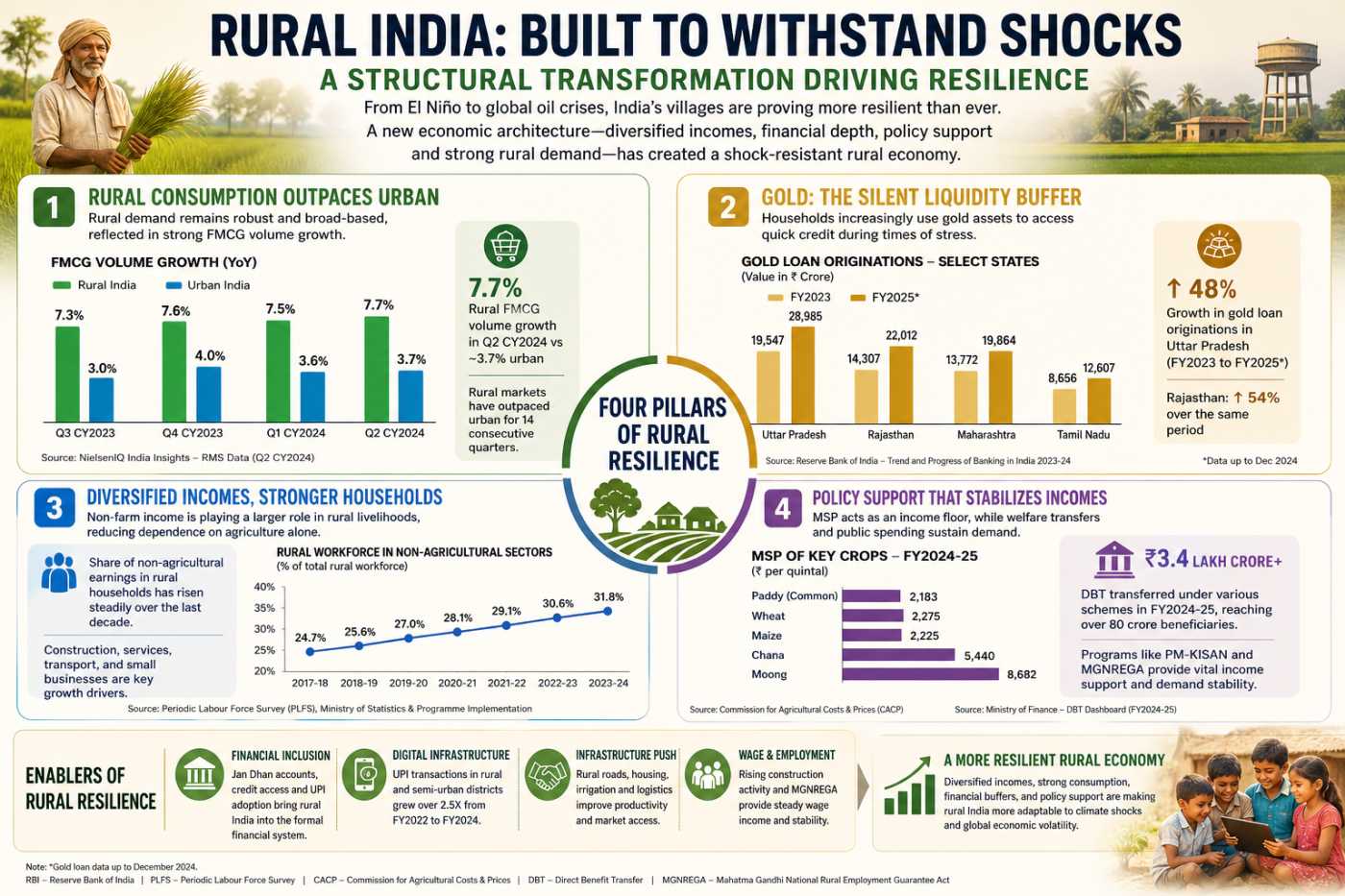

How Rural India Outsmarted El Niño Risks