Good prospects:

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

How Independent Directors Failed Rs 2,500 Crore in Value

India’s Stock Market May Be Sitting on a Trap

Beyond Sugar: India's Bio-Economy Bets Big on Biofuel

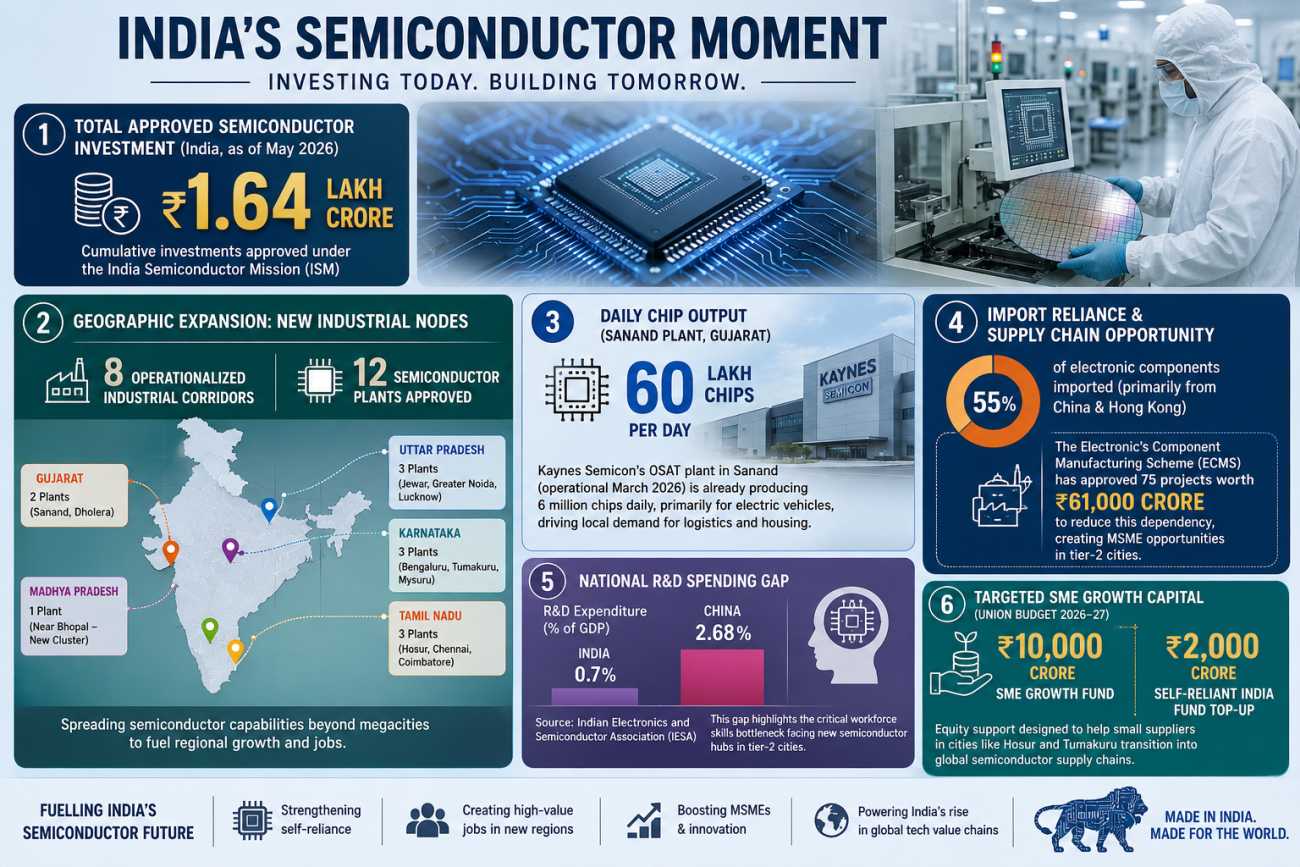

MSMEs & Corridors: India's New Economic Engine

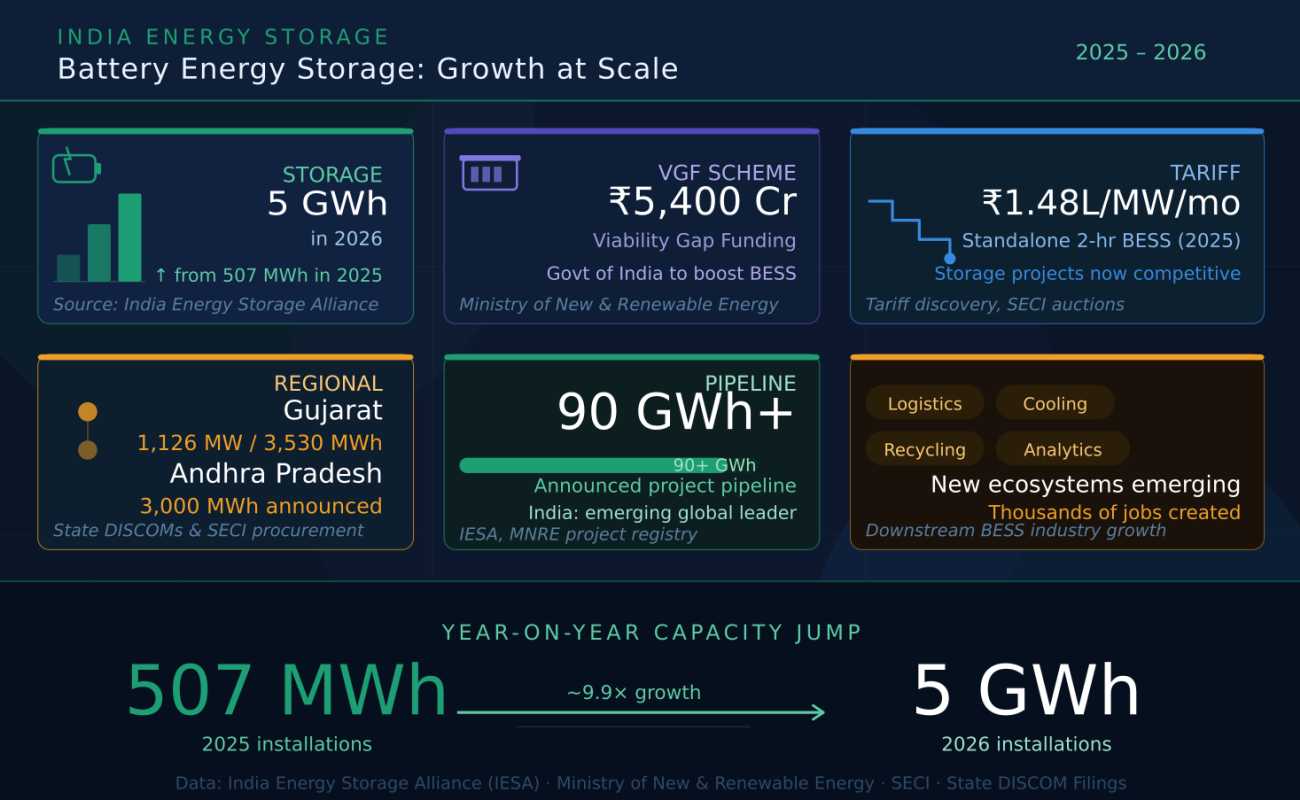

India's Grid-Scale Storage Revolution 2026

India’s IT Sector Faces a Historic Breaking Point

India’s Software Export Machine Faces Its Hardest Structural Shock Yet

For nearly three decades, India’s information technology and business process outsourcing sector functioned as the country’s most reliable economic escalator. It absorbed millions of graduates, stabilized the rupee through software exports, created urban middle-class wealth, and turned Bengaluru, Hyderabad, Pune, Chennai, and Gurugram into globally recognized technology hubs. By 2026, however, the sector is confronting what may be its deepest structural crisis since liberalization.

The problem is not a cyclical slowdown. Nor is it merely a delayed Western enterprise spending recovery. Instead, India’s IT-services model is being squeezed simultaneously by two external shocks that reinforce each other: rapid Generative AI-driven labor compression and a severe energy-import disruption tied to instability around the Strait of Hormuz.

Unlike East Asian economies such as Taiwan and South Korea, which are benefiting from the hardware-intensive side of the AI boom through semiconductor fabrication, memory manufacturing, and advanced packaging, India remains disproportionately dependent on labor-arbitrage software exports. The global AI investment cycle is increasingly rewarding capital-intensive compute infrastructure, chips, and automation platforms rather than large pools of repetitive white-collar labor.

This distinction matters enormously. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, SK Hynix, and other hardware-linked firms are experiencing a surge in AI-driven demand for high-bandwidth memory, GPUs, and advanced fabrication capacity. India, by contrast, built its outsourcing empire around scalable human labor performing software maintenance, QA testing, enterprise support, application management, and back-office business processing. These are precisely the categories now most vulnerable to AI automation.

The consequences are beginning to show up in employment and valuation data. According to reporting by The Times of India, India’s top five IT firms TCS, Infosys, Wipro, HCLTech, and Tech Mahindra collectively shed 6,981 employees in FY26 after modest hiring growth the previous year. TCS alone reportedly reduced headcount by more than 23,000 employees. The article summarized the shift bluntly: “Headcount is passé; outcomes are the new currency.”

That phrase captures the heart of the crisis. India’s traditional IT-services model depended on continuously adding engineers and support workers to grow revenue. Generative AI breaks that equation.

The Collapse of the Pyramid Model

India’s outsourcing industry historically relied on a workforce pyramid. Large numbers of relatively inexpensive junior engineers handled repetitive coding, testing, ticket resolution, infrastructure management, and process operations under the supervision of a smaller layer of senior architects and managers. Profitability depended on scale.

Generative AI systems are rapidly eroding the economic rationale for that pyramid. Enterprise clients are increasingly demanding AI-assisted productivity gains before approving contract renewals. Internal automation initiatives now allow firms to complete maintenance tasks, generate boilerplate code, automate testing workflows, and manage Level-1 support with significantly fewer workers.

Infosys CEO Salil Parekh has repeatedly emphasized the company’s shift toward AI-enabled delivery models. TCS has similarly discussed deploying AI agents internally to improve productivity metrics. The issue for India is not whether AI can replace all engineers immediately. The issue is that even partial automation dramatically weakens the labor-volume model that sustained India’s export machine.

A March 2026 academic paper titled The AI Layoff Trap by Brett Hemenway Falk and Gerry Tsoukalas warned that competitive AI adoption can force firms into labor displacement faster than economies can absorb workers elsewhere. The authors argued that automation pressures may become self-reinforcing because firms fear losing competitiveness if rivals automate first.

The pressure is especially acute in India because much of the country’s IT export success came from low-to-mid complexity execution work rather than proprietary product innovation. AI tools are already highly effective at precisely these repetitive, rules-based tasks.

Even optimistic voices inside the industry acknowledge the compression underway. NVIDIA CEO Jensen Huang stated in May 2026 that software engineers are “busier than ever,” arguing that AI changes work rather than eliminating it entirely. Yet the underlying arithmetic remains uncomfortable for India: if the same project now requires three engineers instead of ten, aggregate employment growth weakens dramatically even if productivity rises.

The result is a structural decoupling between software demand and labor demand.

The Hormuz Shock Turns an Employment Problem Into a Cost Crisis

Ordinarily, India’s IT majors might have cushioned automation pressure through margin management and currency benefits. Instead, a second shock is hitting simultaneously: energy insecurity.

The ongoing disruption around the Strait of Hormuz has exposed India’s extraordinary vulnerability to imported hydrocarbons. According to Business Standard’s March 2026 analysis titled Datanomics: India’s crude flows via Hormuz at risk amid West Asia crisis, approximately 41 percent of India’s crude imports in early 2025 still transited through the Strait of Hormuz despite diversification efforts.

Reuters reported on May 16, 2026, that Iraqi exports through the Strait had collapsed from 93 million barrels per month before the conflict to just 10 million barrels in April 2026. Insurance disruptions, tanker risks, and military instability have sharply constrained Gulf energy flows.

India remains one of the world’s most import-dependent major energy economies. Analysis published by India Briefing in March 2026 estimated that India still imports nearly 90 percent of its crude requirements and that roughly 2.5 to 2.7 million barrels per day are linked to Gulf supply chains.

The macroeconomic implications are severe. Every sustained rise in oil prices worsens India’s current-account deficit, pressures the rupee, and raises imported inflation. But the impact on India’s IT-services ecosystem is more specific and less appreciated.

Modern white-collar outsourcing operations are extraordinarily energy-intensive. Massive office campuses require uninterrupted power for air conditioning, cloud connectivity, backup systems, workstation clusters, and networking infrastructure. Data centers supporting AI workloads consume even larger amounts of electricity.

India’s software industry grew during an era of relatively stable global energy markets. The current environment is very different. As imported LNG costs rise and fuel shortages intensify, Indian corporations are facing elevated operational costs precisely when pricing power is weakening due to AI-driven productivity expectations.

This creates a brutal squeeze on margins.

Reverse Migration and the Fracturing of India’s Urban Tech Economy

One of the most under-discussed consequences of the dual AI-energy shock is the re-emergence of reverse migration pressures.

During the pandemic years, millions of white-collar workers temporarily relocated from India’s major urban centers back to smaller towns and semi-rural districts. By 2024 and 2025, much of the corporate world attempted to restore centralized office operations. The 2026 energy shock is now disrupting that reversal.

As diesel prices rise, electricity reliability weakens, and urban living costs accelerate, companies are once again experimenting with distributed workforces. Smaller Tier-2 and Tier-3 locations with lower living costs are becoming economically attractive for both employers and employees.

However, this is not a healthy decentralization story. It reflects defensive cost-cutting.

The urban consumption engine built around India’s tech workforce is beginning to weaken. Housing demand in premium IT corridors is slowing. Discretionary spending is softening. Recruitment pipelines for fresh engineering graduates are deteriorating. Many mid-level workers increasingly fear becoming stranded between rising living costs and declining long-term employability.

The psychological shift is significant. For decades, India’s IT sector represented upward mobility and economic stability. By mid-2026, it increasingly resembles a sector trapped between automation deflation and imported energy inflation.

Why Corporate Tax Cuts Are Failing to Stabilize Sentiment

The Indian government has continued emphasizing supply-side growth measures, including earlier corporate tax reforms designed to improve competitiveness. Yet these tools appear increasingly ineffective against the current crisis.

The problem is not simply taxation. It is capital allocation.

Global investors are rewarding economies positioned to dominate the physical infrastructure of the AI era: semiconductors, power systems, advanced manufacturing, robotics, and compute infrastructure. India’s comparative advantage remains concentrated in labor-intensive services.

Corporate tax reductions cannot offset a structural repricing of labor itself.

Even profitable Indian IT firms are seeing valuation pressure because markets increasingly question whether traditional outsourcing revenue models can sustain historical growth rates in an AI-native world. Investors are asking difficult questions:

- How much human labor will enterprise clients need five years from now?

- Can billing models based on workforce scale survive agentic automation?

- Will AI compress pricing faster than firms can create higher-value services?

- Can India compete meaningfully in semiconductor manufacturing and compute infrastructure before automation weakens its labor-cost advantage?

These concerns help explain why market sentiment toward large IT exporters has become increasingly cautious despite continued profitability.

The Hardware Divide Between India and East Asia

The contrast with East Asia is stark.

Taiwan and South Korea are deeply embedded in the hardware backbone of the AI revolution. TSMC controls advanced-node semiconductor fabrication critical for NVIDIA and AMD AI accelerators. Samsung and SK Hynix dominate memory technologies essential for high-performance AI systems.

AI adoption globally is therefore driving capital expenditure toward fabs, advanced packaging plants, energy infrastructure, and chip manufacturing ecosystems.

India participates only marginally in these layers today.

The Indian government has launched ambitious semiconductor incentive programs under the India Semiconductor Mission. Yet fabrication ecosystems require years of infrastructure buildup, massive electricity reliability, water availability, supply-chain integration, and highly specialized engineering talent.

The uncomfortable timing problem for India is that its traditional software-services labor model may weaken faster than its semiconductor ambitions mature.

This leaves India unusually exposed compared with economies participating directly in AI hardware monetization.

The New White-Collar Fragility

The deepest implication of the 2026 crisis may be sociological rather than technological.

India’s economic rise over the last quarter-century depended heavily on the assumption that educated white-collar labor represented a stable pathway into the middle class. Engineering degrees, software jobs, outsourcing contracts, and multinational service centers became the foundation of aspirational India.

Generative AI is challenging that assumption at scale.

The vulnerability is particularly severe because many of the tasks historically performed by India’s outsourcing workforce are highly structured, process-driven, and digitally standardized exactly the conditions under which AI systems perform best.

The sector is therefore confronting an uncomfortable paradox. The same digital standardization that allowed India to dominate global outsourcing is now accelerating automation exposure.

Energy insecurity compounds the problem further by raising the cost base of the very urban ecosystems that supported India’s white-collar expansion.

The result is not a conventional recession. It is a structural collision between automation economics and import-dependent energy vulnerability.

For years, India’s software-services boom insulated the country from deeper industrial weaknesses. By mid-2026, that insulation is beginning to fracture.

If you have enjoyed reading, spread the word:

Why Gujarat And Rajasthan Are Winning Big

Tier-2 Cities Are Now India's Financial Powerhouses

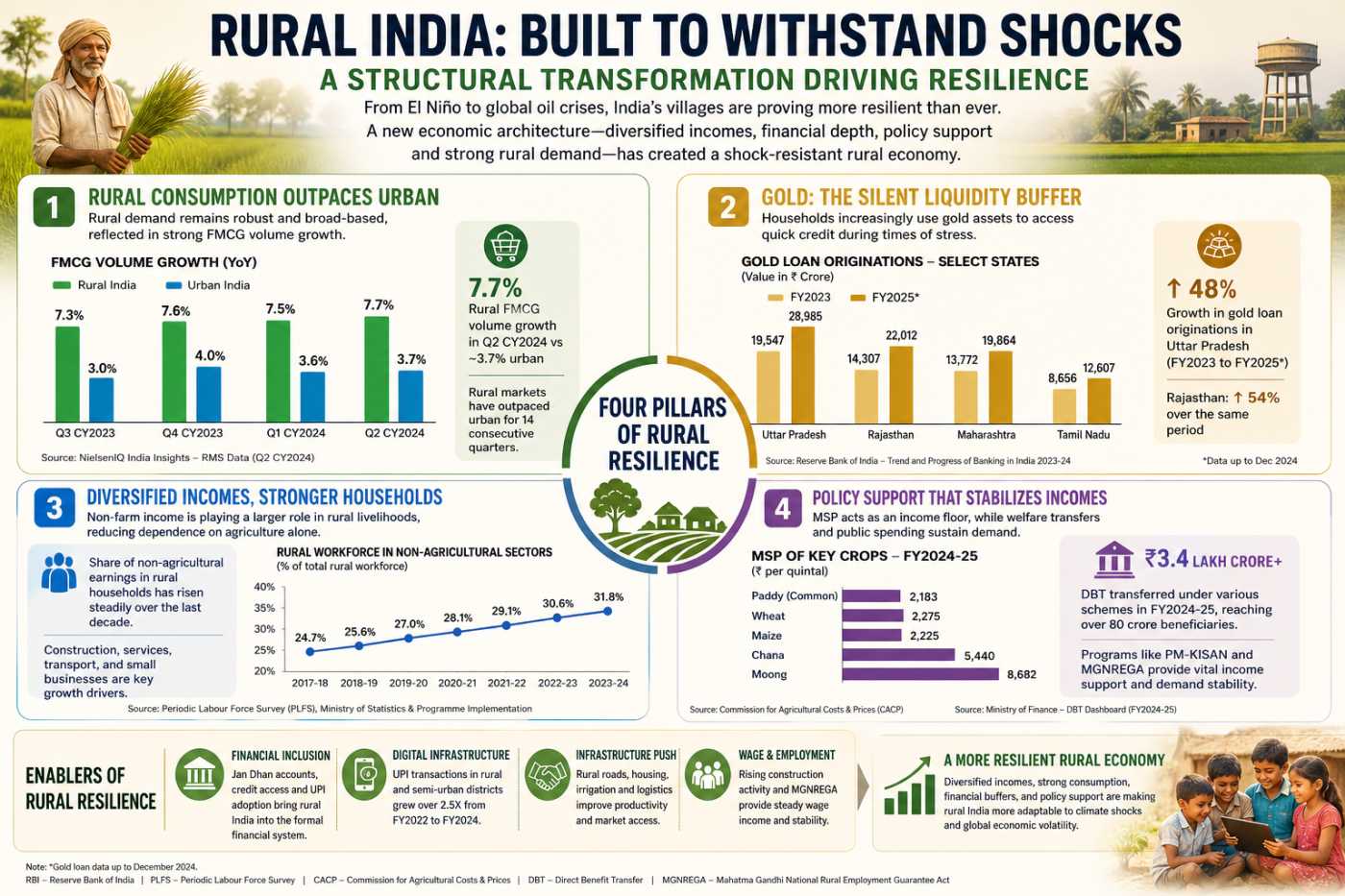

How Rural India Outsmarted El Niño Risks

MUDRA’s Unseen Women Army