More about Laxmi Organic Industries Limited

Fundamentals for Laxmi Organic Industries Limited

Regulatory Filings for Laxmi Organic Industries Limited

Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

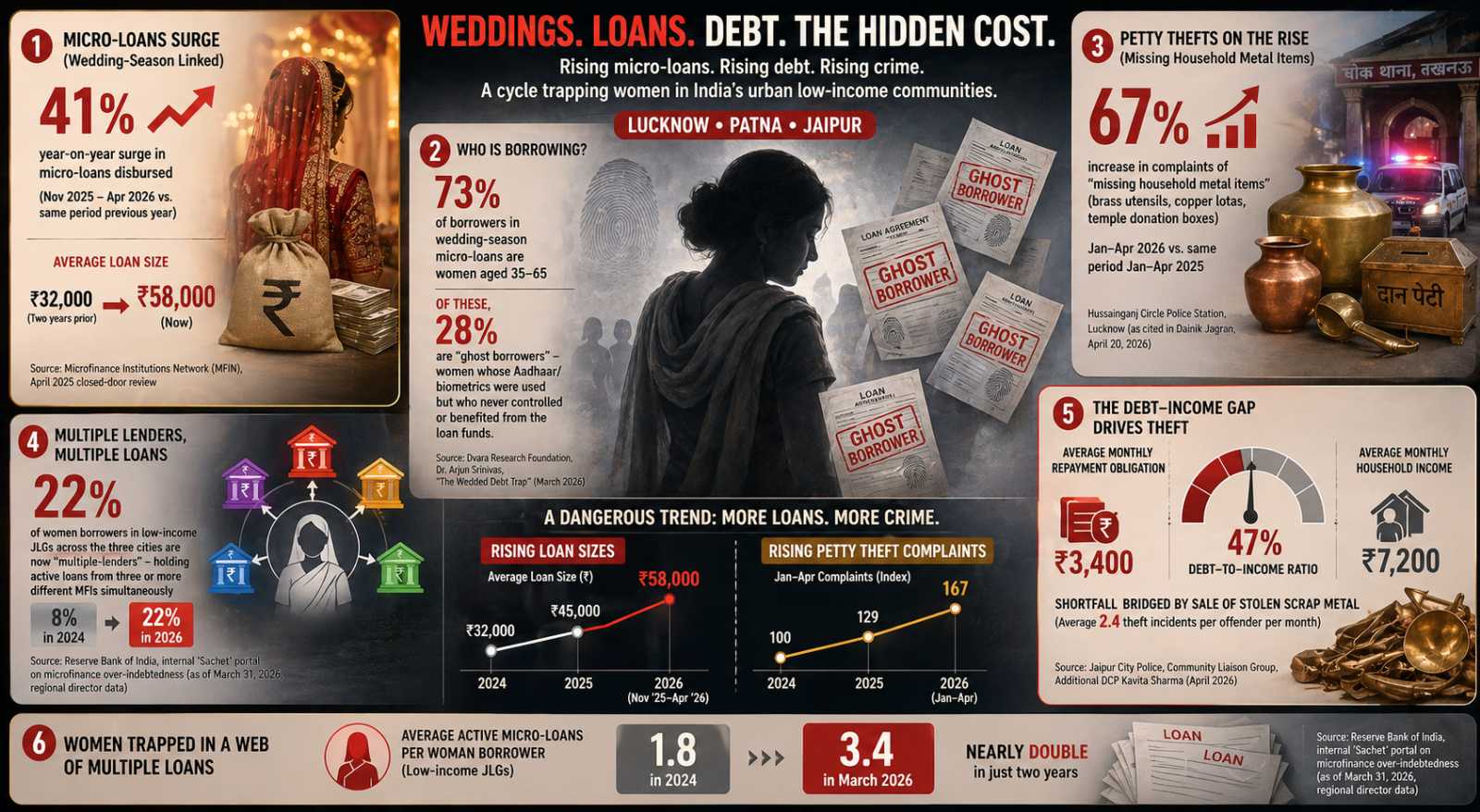

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for Laxmi Organic Industries Limited

Business Operations:

Sector: Basic MaterialsIndustry: Specialty Chemicals

Laxmi Organic Industries Limited provides acetyl and specialty intermediate products in India and internationally. The company's acetyl intermediates include ethyl acetate, acetaldehyde, fuel-grade ethanol, acetic anhydride, and other proprietary solvents; and specialty intermediates comprise ketene and diketene derivatives, esters, amides, arylides, and fluorospeciality Intermediates. Its products are used in pharmaceuticals, agrochemicals, flexible packaging, auto coatings, printing inks, personal care, cosmetics, and other industrial applications. Laxmi Organic Industries Limited was incorporated in 1989 and is based in Mumbai, India. Laxmi Organic Industries Limited is a subsidiary of Yellow Stone Trust.

Revenue projections:

LXCHEM is projected to experience a revenue decline compared to last year, a development that often leads to investor caution. The drop could negatively impact the company's bottom line, as lower revenues typically signal reduced profitability, prompting more conservative investment strategies.

Financial Ratios:

| currentRatio | 0.00000 |

|---|---|

| forwardPE | 28.96200 |

| debtToEquity | 17.29000 |

| earningsGrowth | -0.12400 |

| revenueGrowth | -0.08600 |

| grossMargins | 0.24048 |

| operatingMargins | 0.04099 |

| trailingEps | 2.87000 |

| forwardEps | 5.00000 |

LXCHEM's Forward PE ratio is favorable, meaning the stock price aligns well with earnings and isn't overvalued. This allows room for growth, making it an attractive investment for those seeking potential upside while ensuring the stock is not overpriced.

Laxmi Organic Industries Limited's low Debt-to-Equity ratio indicates that the company isn't over-leveraged, suggesting it maintains a healthy balance between debt and equity. This lowers financial risk and points to a stable financial foundation, reassuring investors of the company's financial health.

LXCHEM's low growth in both earnings and revenue signals a potential profit decline. This could be a sign of financial trouble, suggesting that the company's profitability might shrink in the near future.

LXCHEM's negative gross and operating margins point to financial difficulties, as the company is unable to generate profit from its core operations or production. This could signal broader problems in cost management or declining sales.

LXCHEM's forward EPS exceeds its trailing EPS, indicating that the company is projected to be more profitable in the current financial year compared to the previous one. This suggests positive growth and improved earnings, signaling an optimistic outlook for LXCHEM's financial performance.

Price projections:

Price projections for LXCHEM have been revised lower over time, signaling a more cautious outlook from analysts. The gradual downward trend indicates that expectations for the company's growth may be softening.

Recommendation changes over time:

The analysts' sell bias for Laxmi Organic Industries Limited suggests caution for investors, but it's essential to make decisions based on a wide array of market indicators. This approach ensures a comprehensive view of Laxmi Organic Industries Limited's position, helping to navigate any potential risks more effectively.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy