More about Hindustan Copper Limited

Fundamentals for Hindustan Copper Limited

Regulatory Filings for Hindustan Copper Limited

Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

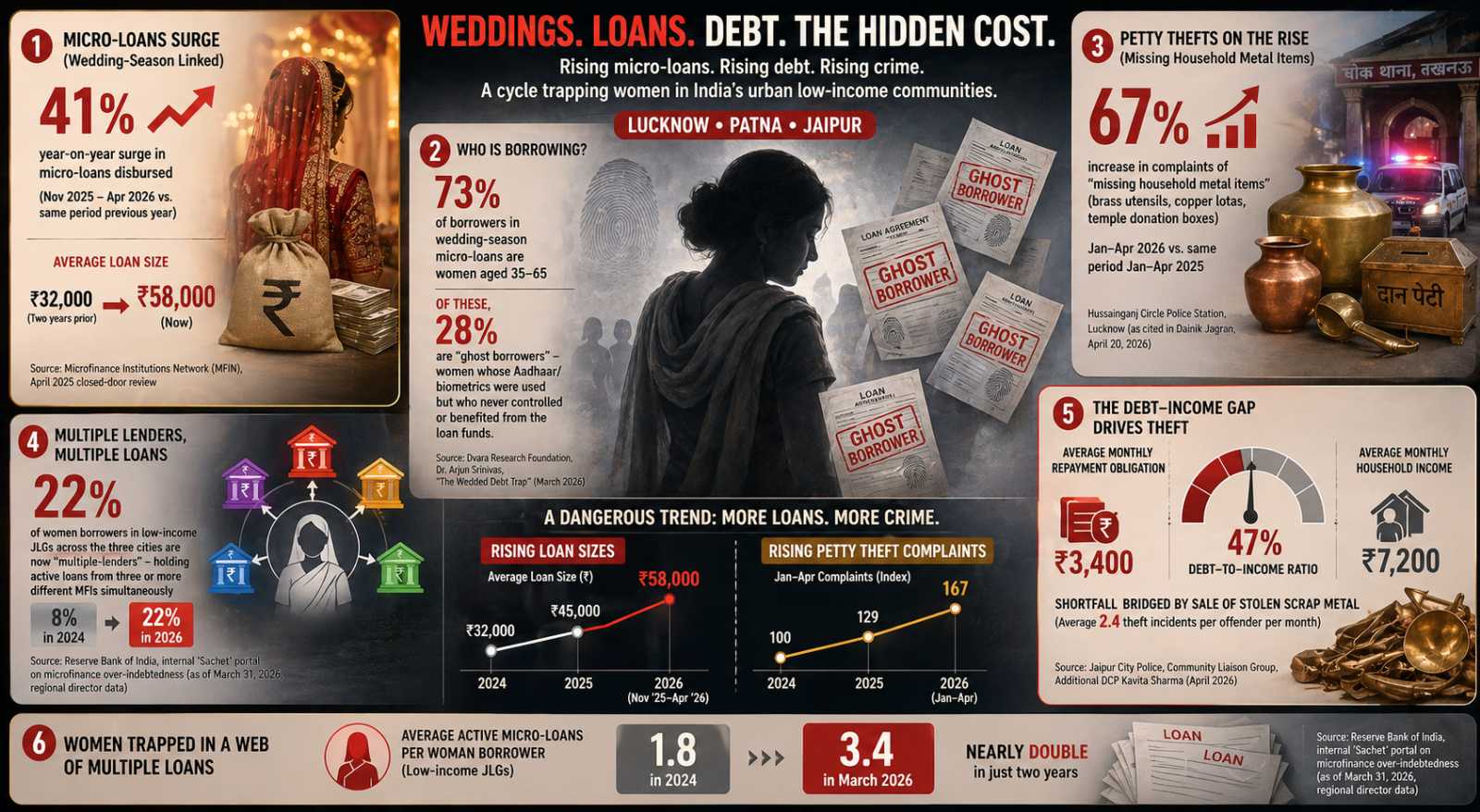

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for Hindustan Copper Limited

Business Operations:

Sector: Basic MaterialsIndustry: Copper

Hindustan Copper Limited engages in the exploration, exploitation, and mining of copper and copper ores in India. It also involved in the beneficiation, smelting, and refining of minerals. The company's flagship project is the Malanjkhand Copper project located in Madhya Pradesh. It offers continuous cast copper rods, copper cathodes, copper concentrates, copper sulfate, sulphuric acid, reverts, anode slime, and nickel cathodes. The company also exports its products. Hindustan Copper Limited was incorporated in 1967 and is based in Kolkata, India.

Revenue projections:

HINDCOPPER's revenue is forecasted to be roughly the same as last year's, suggesting a neutral financial position. This steady performance may reflect financial stability, but it lacks the excitement of potential growth, leaving investors with a balanced perspective.

Financial Ratios:

| currentRatio | 0.00000 |

|---|---|

| forwardPE | 27.49745 |

| debtToEquity | 4.77600 |

| earningsGrowth | 1.49200 |

| revenueGrowth | 1.09700 |

| grossMargins | 0.93683 |

| operatingMargins | 0.28600 |

| trailingEps | 6.85000 |

| forwardEps | 19.60000 |

HINDCOPPER's Forward PE ratio is favorable, meaning the stock price aligns well with earnings and isn't overvalued. This allows room for growth, making it an attractive investment for those seeking potential upside while ensuring the stock is not overpriced.

HINDCOPPER's positive earnings and revenue growth indicate that the company is expected to continue expanding its business. These trends reflect strong financial health, with increasing profits and sales suggesting sustained growth and success for HINDCOPPER.

Hindustan Copper Limited's positive gross and operating margins suggest strong profitability. These margins reflect effective cost management and revenue generation, indicating that the company is efficiently managing its operations and maintaining financial health.

HINDCOPPER's forward EPS surpassing its trailing EPS signals that the company is anticipated to be more profitable this year than last. This growth expectation highlights HINDCOPPER's potential for increased earnings and a stronger financial performance in the upcoming year.

Price projections:

Price projections for HINDCOPPER have gradually risen over time, signaling increased optimism about the company's future prospects. This steady upward revision reflects growing confidence in HINDCOPPER's market potential.

Recommendation changes over time:

The recent buy bias for Hindustan Copper Limited from analysts signals strong confidence in the stock's potential. This positive sentiment could encourage investors to see Hindustan Copper Limited as a smart place to invest their money, especially those looking for stable, long-term returns in a well-established company.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy