More about Hindalco Industries Limited

Fundamentals for Hindalco Industries Limited

Regulatory Filings for Hindalco Industries Limited

Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

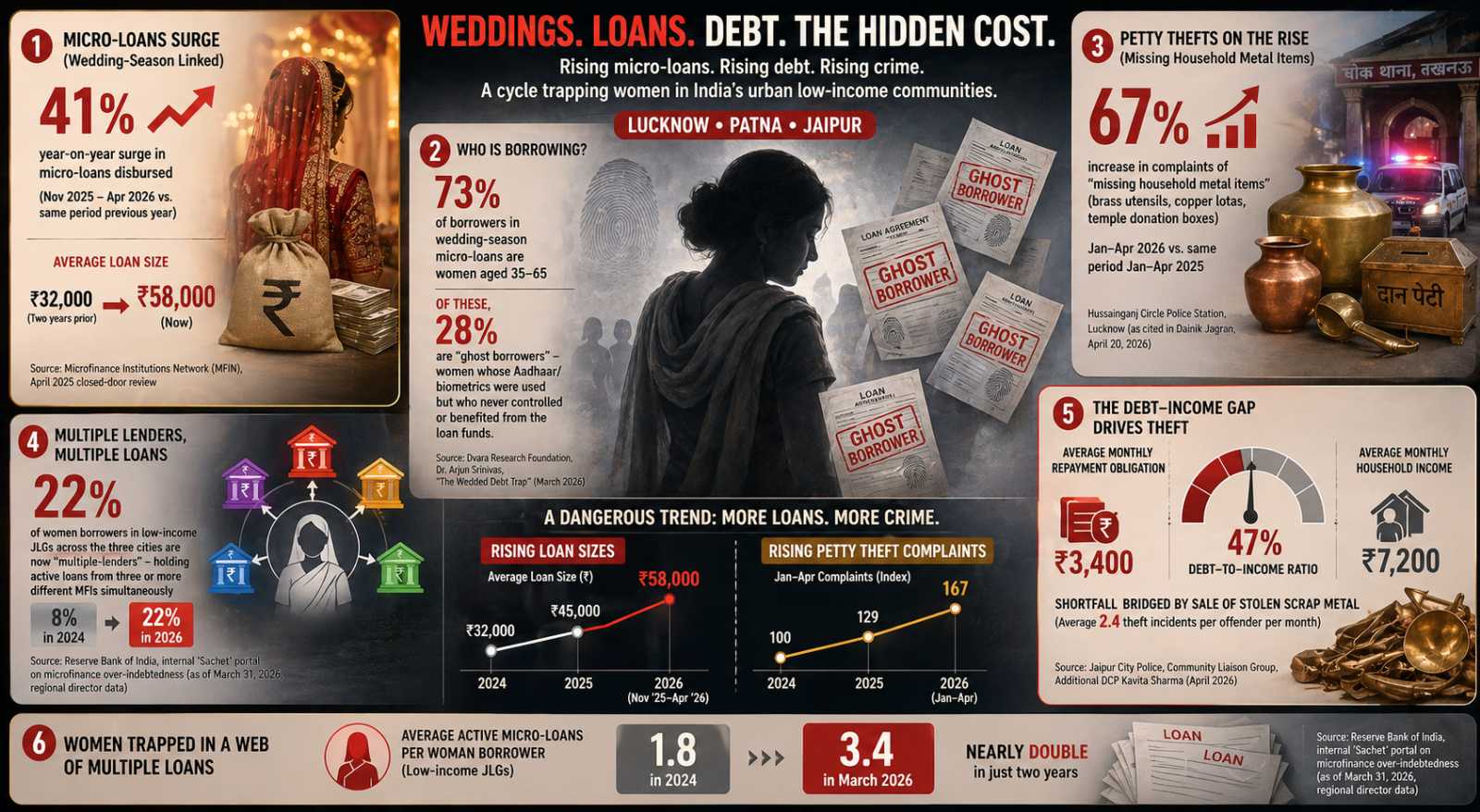

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for Hindalco Industries Limited

Business Operations:

Sector: Basic MaterialsIndustry: Aluminum

Hindalco Industries Limited, together with its subsidiaries, produces and sells aluminum and copper products in India and internationally. The company operates through Novelis, Aluminium Upstream, Aluminium Downstream, and Copper segments. It offers fine and reactive alumina; primary aluminum in the form of ingots, billets, and wire rods; aluminum flat rolled products (FRP), including sheets, stocks, plates, coils, and circles; aluminum extrusions; and aluminum foil and packaging solutions for use in the automotive and transport, building and construction, aerospace and defense, electrical and electronics, pharmaceuticals and packaging, consumer durables and kitchenware, and white goods industries, as well as industrial applications. The company also provides coarse alumina hydrate for use in alum, poly aluminum chloride, zeolites, aluminum fluoride, sodium aluminate, glass, catalysts, and aluminum hydroxide gel; fine alumina hydrates; and calcined alumina for use in ceramics, refractories, polishing, and flame retardants. In addition, it offers copper products, including copper cathodes and continuous cast copper rods that are used in the agrochemical, automotive and transport, consumer durable, electrical equipment, railway, wire and cable, and electric vehicle and renewables industries; and precious metals comprising gold and silver bars, as well as selenium powder. Further, the company operates an all-weather jetty in the Gulf of Khambhat on the west coast of India; produces di-ammonium phosphate and nitrogen phosphorus potassium complexes; and offers phosphoric acid, phosphogypsum, sulfuric acid, copper slag, and aluminum fluoride. It offers its aluminum extrusion products under the Hindalco extrusions, Maxloader, Eternia, and Totalis brands; aluminum FRP under the Everlast brand; aluminum foils under the Freshwrapp and Superwrap brands; and copper products under the Birla Balwan brand. The company was incorporated in 1958 and is based in Mumbai, India.

Revenue projections:

With HINDALCO's revenue expected to be lower than the previous year, investors may become cautious. Declining revenues often negatively impact the bottom line, reducing profitability and raising concerns among investors about the company's ability to maintain strong financial performance moving forward.

Financial Ratios:

| currentRatio | 0.000000 |

|---|---|

| forwardPE | 11.784091 |

| debtToEquity | 57.571000 |

| earningsGrowth | -0.451000 |

| revenueGrowth | 0.139000 |

| grossMargins | 0.318290 |

| operatingMargins | 0.086800 |

| trailingEps | 72.240000 |

| forwardEps | 88.000000 |

HINDALCO's Forward PE is within a good range, showing that the stock price compares well to its earnings. This suggests it isn't overpriced and leaves room for growth, making the stock appealing to investors looking for value and growth opportunities.

HINDALCO's low earnings and revenue growth highlight a potential decline in profitability. This suggests that the company's financial health may be weakening, and profits could shrink as a result.

Hindalco Industries Limited's negative gross and operating margins signal that the company is not profitable, struggling to cover costs associated with production and operations. This could be a red flag for its financial performance moving forward.

HINDALCO's forward EPS is higher than its trailing EPS, suggesting the company is expected to see an increase in profitability this year. This points to positive growth, indicating that HINDALCO is projected to improve its financial performance compared to the previous year.

Price projections:

HINDALCO's price projections have been gradually revised upward, reflecting increased confidence in the company's future performance. This trend suggests analysts expect HINDALCO to achieve greater success in the coming periods.

Recommendation changes over time:

HINDALCO has been receiving a buy bias from analysts, signaling strong confidence in the stock's future performance. This positive outlook might drive investors to view HINDALCO as an attractive option for their portfolios, positioning the company as a stable and profitable investment choice.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy