More about Hero MotoCorp Limited

Fundamentals for Hero MotoCorp Limited

Regulatory Filings for Hero MotoCorp Limited

Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

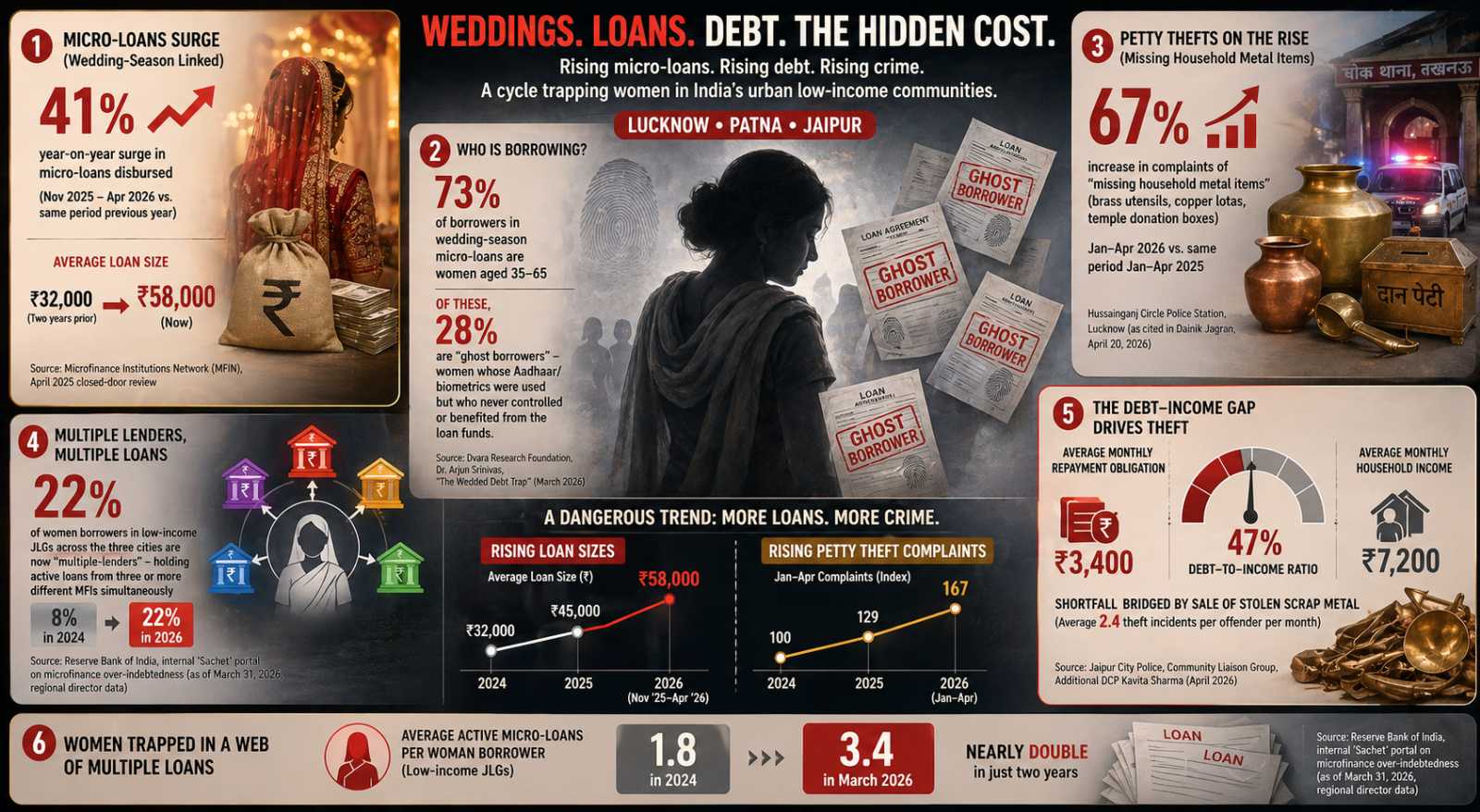

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for Hero MotoCorp Limited

Business Operations:

Sector: Consumer CyclicalIndustry: Auto Manufacturers

Hero MotoCorp Limited primarily engages in the manufacture and sale of motorized two wheelers in India, Asia, Central and Latin America, Africa, and the Middle East. The company offers motorcycles and scooters, as well as electric scooters. It provides engines, parts, and accessories, as well as related services. The company was formerly known as Hero Honda Motors Ltd. and changed its name to Hero MotoCorp Limited in July 2011. Hero MotoCorp Limited was incorporated in 1984 and is based in New Delhi, India.

Revenue projections:

Revenues for HEROMOTOCO are expected to drop compared to the previous year, which could be a cause for concern for investors. A decline in earnings may negatively impact the company's profitability, leading cautious investors to reconsider their positions, as it often signals challenges in overall financial health.

Financial Ratios:

| currentRatio | 0.000000 |

|---|---|

| forwardPE | 17.589071 |

| debtToEquity | 3.395000 |

| earningsGrowth | 0.144000 |

| revenueGrowth | 0.217000 |

| grossMargins | 0.335980 |

| operatingMargins | 0.130350 |

| trailingEps | 271.780000 |

| forwardEps | 290.521300 |

Hero MotoCorp Limited's Forward PE ratio suggests that the stock is priced appropriately in relation to its earnings. Not being overpriced, it offers room for growth, signaling potential upside for investors looking for a stock with reasonable valuation and growth potential.

With earnings and revenue growth in positive territory, HEROMOTOCO is projected to expand its business. This strong financial performance suggests the company will continue to grow, as increased profitability and sales drive future success.

HEROMOTOCO's forward EPS surpassing its trailing EPS signals that the company is anticipated to be more profitable this year than last. This growth expectation highlights HEROMOTOCO's potential for increased earnings and a stronger financial performance in the upcoming year.

Price projections:

Over time, HEROMOTOCO's price projections have been revised higher, signaling growing confidence in the company's future. This upward trend suggests analysts anticipate strong performance and increased market value for HEROMOTOCO.

Recommendation changes over time:

With analysts showing a buy bias for HEROMOTOCO, investors may be more inclined to see the stock as an attractive investment. The favorable outlook could spur increased interest, positioning HEROMOTOCO as a safe and profitable place for investors to allocate their funds and seek growth.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy