More about Devyani International Limited

Fundamentals for Devyani International Limited

Regulatory Filings for Devyani International Limited

Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

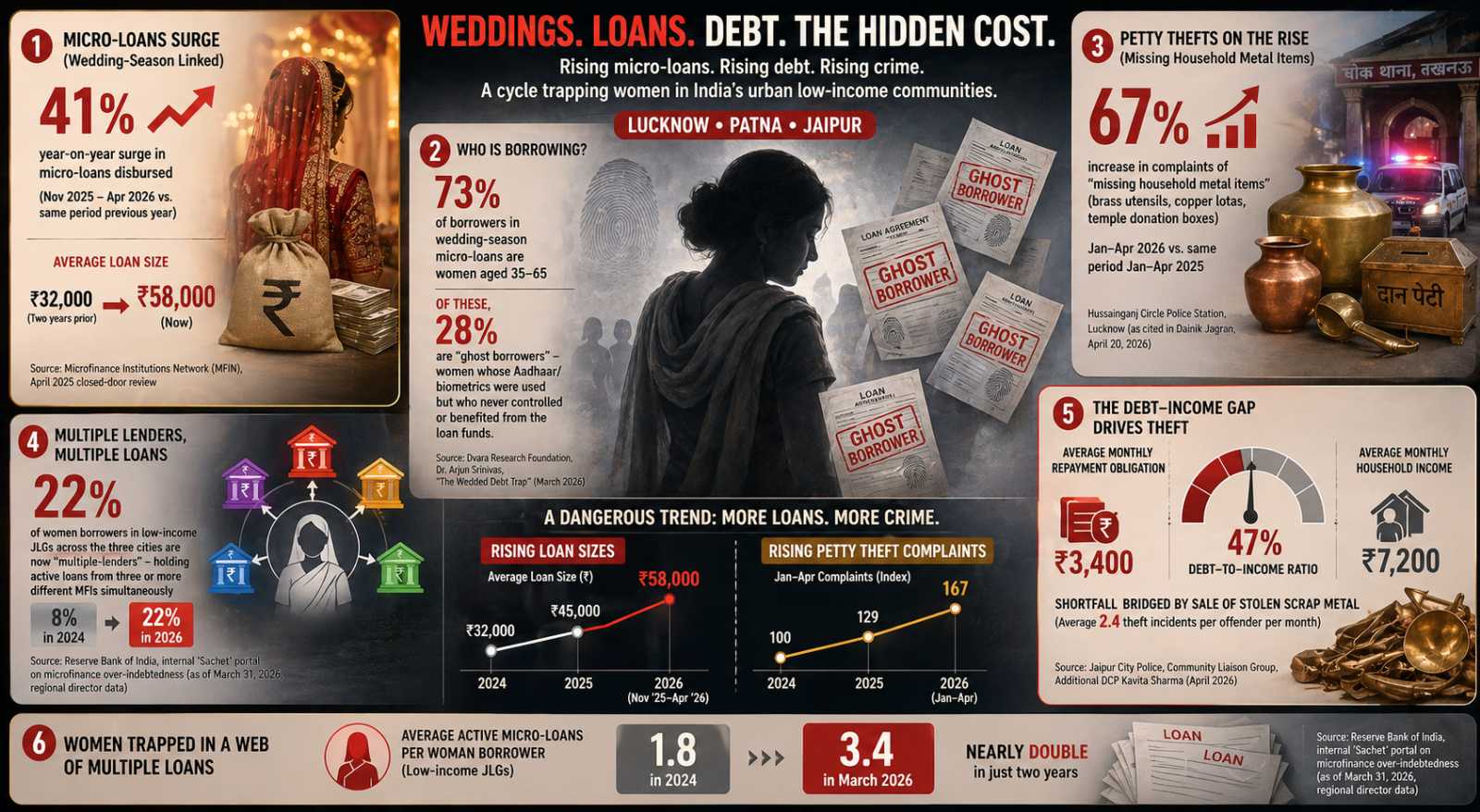

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for Devyani International Limited

Business Operations:

Sector: Consumer CyclicalIndustry: Restaurants

Devyani International Limited develops, manages, and operates quick service restaurants and food courts in India, Nepal, Nigeria, Thailand, and internationally. Its Core Brands Business include KFC, Pizza Hut, and Costa Coffee outlets operated in India; International Business comprise KFC, Pizza Hut, and other brand outlets operated in Nepal and Nigeria; and Other Business consists of food and beverages industry operations, including Vaango and The Food Street brand stores. Devyani International Limited was incorporated in 1991 and is based in Gurugram, India. Devyani International Limited is a subsidiary of RJ Corp Limited.

Revenue projections:

DEVYANI's revenue is projected to decrease from last year, a development that could lead investors to adopt a more cautious approach. A revenue decline can negatively affect profitability, signaling challenges for the company and making it less attractive for those seeking solid financial performance.

Financial Ratios:

| currentRatio | 0.00000 |

|---|---|

| forwardPE | 147.82660 |

| debtToEquity | 170.71200 |

| earningsGrowth | 0.00000 |

| revenueGrowth | 0.11300 |

| grossMargins | 0.50789 |

| operatingMargins | 0.04169 |

| trailingEps | -0.32000 |

| forwardEps | 0.84660 |

DEVYANI's elevated forward PE ratio suggests limited upside potential and a risk of price correction. Investors must scrutinize this metric closely, ensuring it aligns with other fundamental indicators before making any decisions.

DEVYANI's high debt-to-equity ratio indicates a strong reliance on debt, meaning the company is heavily leveraged. This could increase financial risks if cash flow or earnings decline, making it more difficult for DEVYANI to manage its debt obligations.

Price projections:

DEVYANI's price projections have been revised downward gradually, suggesting that expectations for the company's future performance are becoming more conservative. Analysts may be tempering their optimism based on current trends.

Recommendation changes over time:

Recent analysis shows a strong buy bias for DEVYANI, encouraging investors to view it as a solid investment option. The positive sentiment surrounding DEVYANI suggests it could be an attractive place to allocate funds, motivating potential investors to consider the stock as a valuable part of their portfolio.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy