More about DCM Shriram Limited

Fundamentals for DCM Shriram Limited

Regulatory Filings for DCM Shriram Limited

Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

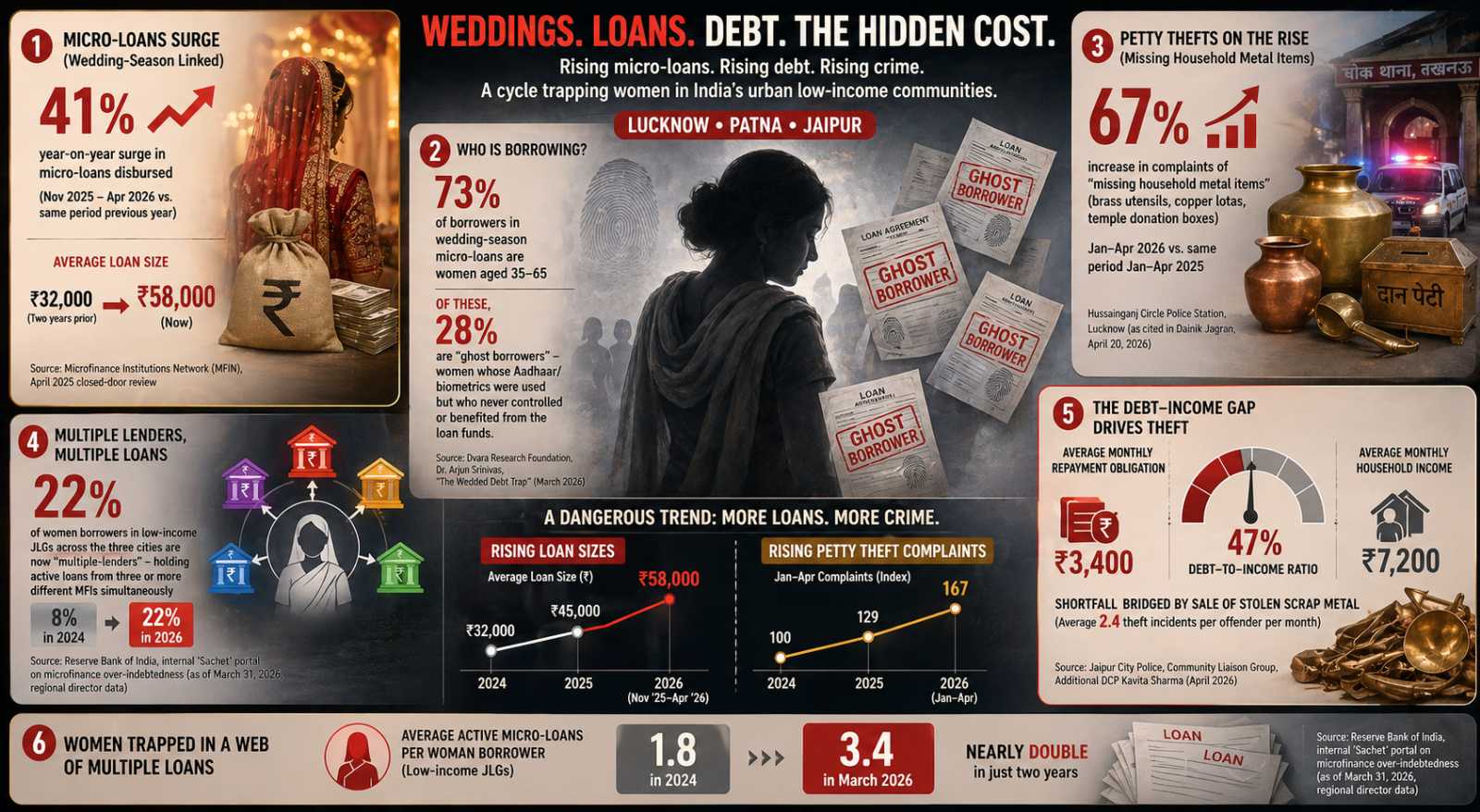

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for DCM Shriram Limited

Business Operations:

Sector: IndustrialsIndustry: Conglomerates

DCM Shriram Limited, together with its subsidiaries, engages in chloro-vinyl, sugar, agri-input, and other businesses in India and internationally. The company operates through Chloro-Vinyl, Sugar, Shriram Farm Solutions, Bioseed, Fertilisers, Fenesta Building, and Others segments. It manufactures and sells urea; caustic soda lye and flakes, and chlorine; sugar, ethanol, and Bagasse based cogen power plants; plant nutrition solutions, crop care chemicals, and hybrid seeds; caustic soda, chlorine, hydrogen, stable bleaching powder, calcium carbide, PVC resins, and aluminum chloride; and UPVC and aluminum windows and doors. In addition, the company sells fuel comprising petrol and diesel; and cement related products. Further, it provides advanced material products, including liquid epoxy resins, hardeners, solvent cuts, reactive diluents, and formulated resins for various sectors, such as wind-blades, EVs, aeronautics, electronics, fire-proofing, and light-weighting industries. The company was incorporated in 1989 and is based in New Delhi, India. DCM Shriram Limited operates as a subsidiary of Sumant Investments Pvt Ltd.

Revenue projections:

Financial Ratios:

| currentRatio | 0.000000 |

|---|---|

| forwardPE | 28.191366 |

| debtToEquity | 30.055000 |

| earningsGrowth | -0.192000 |

| revenueGrowth | 0.132000 |

| grossMargins | 0.337670 |

| operatingMargins | 0.104340 |

| trailingEps | 42.470000 |

| forwardEps | 42.850000 |

DCM Shriram Limited's Forward PE being in a good range indicates the stock is priced well relative to its earnings. It is not overvalued, leaving space for future growth, making it an appealing option for investors interested in long-term value appreciation.

DCMSHRIRAM's low growth in both earnings and revenue indicates potential profit shrinkage. This downward trend could be a sign of weakening financial health, signaling challenges for the company's future profitability.

DCMSHRIRAM's negative gross and operating margins indicate the company is operating at a loss, unable to generate profit from its core business activities. This suggests financial strain and potential challenges in maintaining profitability.

With a forward EPS greater than its trailing EPS, DCMSHRIRAM is expected to see higher profitability this year. The forecasted increase in earnings reflects optimism about the company's financial growth and potential for improved performance over the prior year.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy