Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

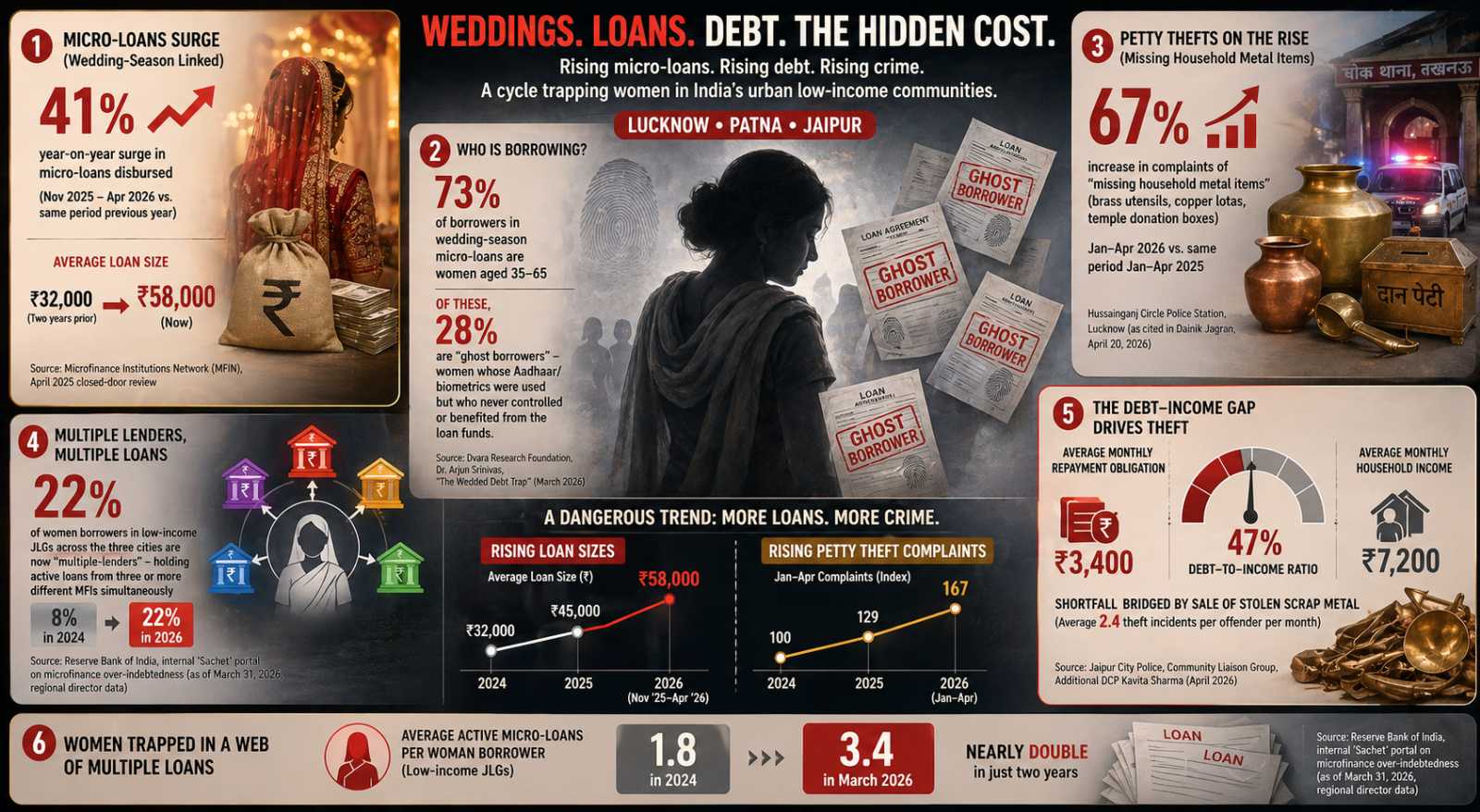

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for CESC Limited

Business Operations:

Sector: UtilitiesIndustry: Utilities - Regulated Electric

CESC Limited, an integrated electrical utility company, engages in the generation and distribution of electricity in India. It owns and operates two thermal power plants, including Budge Budge and Southern generating stations generating 1125 megawatts (MW) of power; a thermal power project with a capacity of 600 MW in Haldia, West Bengal; two thermal power projects with a capacity of 600 MW in Chandrapur, Maharashtra and 40 MW atmospheric fluidised bed combustion power plant in Asansol, West Bengal; and distributes power in Uttar Pradesh. The company also owns and operates solar power projects with a capacity of 18 MW data center in Ramanathapuram, Tamil Nadu. It serves domestic, industrial, commercial, and other users. CESC Limited was founded in 1899 and is headquartered in Kolkata, India.

Revenue projections:

With CESC's revenues forecasted to be lower than last year's, investors are expected to be cautious. A decline in revenue typically harms the company's bottom line, reducing profitability and making investors less confident about the company's ability to sustain its financial health.

Financial Ratios:

| currentRatio | 0.000000 |

|---|---|

| forwardPE | 14.974066 |

| debtToEquity | 141.107000 |

| earningsGrowth | 0.080000 |

| revenueGrowth | 0.125000 |

| grossMargins | 0.380800 |

| operatingMargins | 0.128090 |

| trailingEps | 11.140000 |

| forwardEps | 12.555040 |

CESC's Forward PE being in a good range indicates that the stock is valued appropriately based on its earnings. This suggests the stock is not overpriced and leaves room for growth, providing investors with an opportunity for potential appreciation in value.

CESC Limited's high debt-to-equity ratio indicates a high level of leverage, meaning the company relies significantly on debt for financing. This can increase financial risk, particularly in times of economic instability or reduced profitability.

CESC's forward EPS exceeding its trailing EPS means that the company is expected to increase profitability in the current financial year. This reflects improved earnings potential, signaling that CESC is likely to outperform its previous year's financial performance.

Price projections:

The price of CESC Limited has often been situated close to the lower end of projections. This consistent trend may signal difficulties for the company in achieving investor expectations for future performance.

Recommendation changes over time:

Analysts have shown a buy bias for CESC, signaling it as a strong investment choice. This positive outlook could motivate investors to allocate funds to CESC, seeing it as a reliable and potentially profitable option, especially in an environment where the stock market is highly scrutinized.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy