Defence Profits Reach Dharavi's Machinists

From COVID Debt to Green Despair: Industrial Discharge Is Destroying India’s Last Prawn Nurseries

The Hidden Cost of India's Electronics Assembly Push: A 40% E-Waste Surge and the Death of Affordable Repair

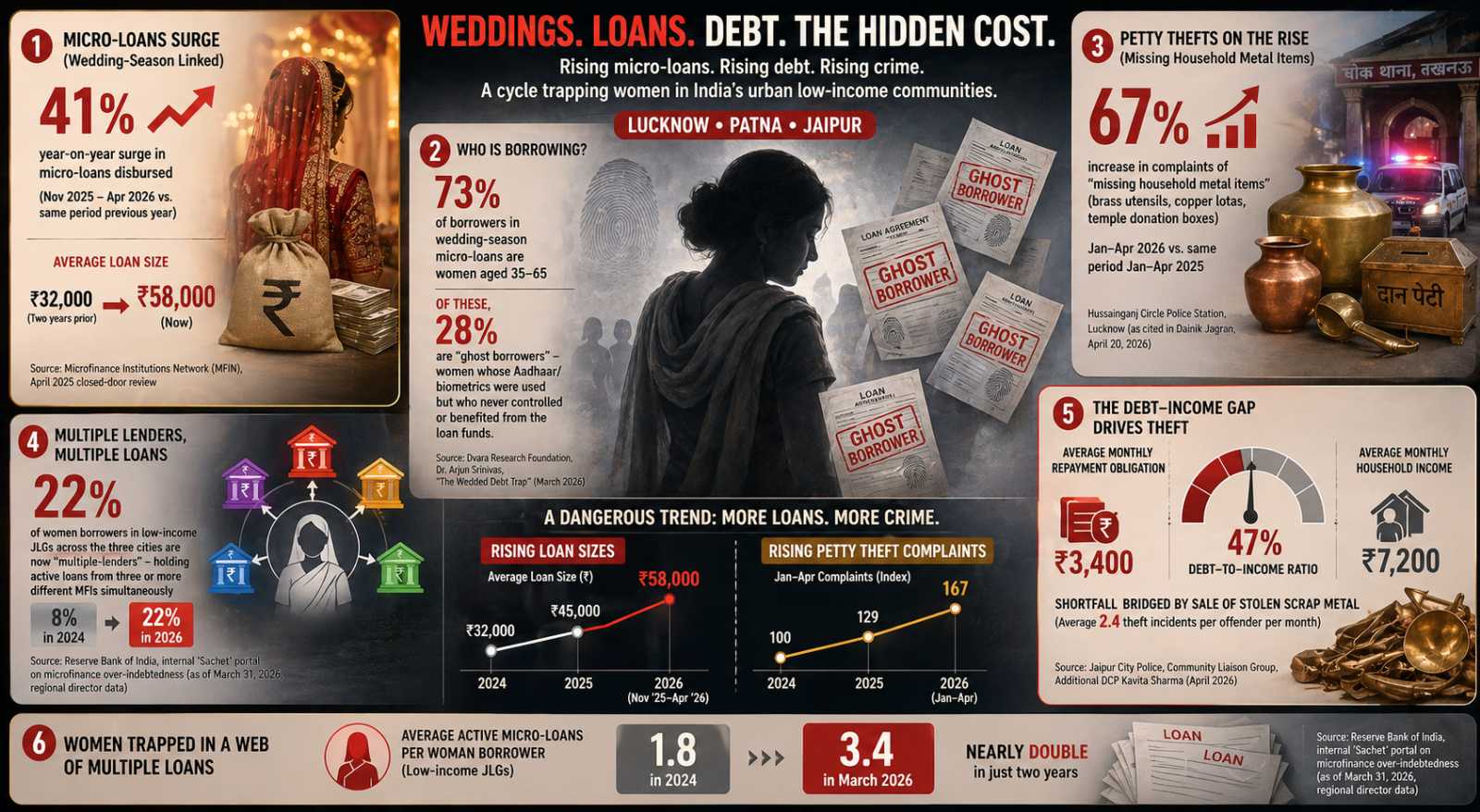

The Wedding Loan Trap: How India’s Microfinance Boom Turned Housewives Into Ghost Borrowers and Temple Brass Into EMI Cash

Fundamentals for Biocon Limited

Business Operations:

Sector: HealthcareIndustry: Biotechnology

Biocon Limited, together with its subsidiaries, engages in the manufacture and sale of biotechnology products and research services in India, Brazil, Singapore, and internationally. It operates through four segments: Generics, Novel Biologics, Biosimilars, and Research Services. The company offers generic formulations and API products, including anti-diabetics, immunosuppressants, multiple sclerosis, anti-cancer/oncology, and other products; novel biologics products, such as head and neck cancer molecule; novel pipeline products comprising psoriasis molecules; and biosimilars products consisting of insulins, trastuzumab, pegfilgrastim, and bevacizumab. It also provides integrated discovery, development, and manufacturing services to pharmaceutical, biotechnology, animal healthcare, consumer good, and agrochemical companies. Biocon Limited was incorporated in 1978 and is headquartered in Bengaluru, India.

Revenue projections:

BIOCON is projected to see lower revenues than in the previous year, a trend that usually concerns investors. Declining revenues often harm a company's profitability, leading investors to exercise caution as they weigh the potential risks of continued financial downturns.

Financial Ratios:

| currentRatio | 0.000000 |

|---|---|

| forwardPE | 39.532597 |

| debtToEquity | 50.024000 |

| earningsGrowth | 4.095000 |

| revenueGrowth | 0.092000 |

| grossMargins | 0.608710 |

| operatingMargins | 0.076250 |

| trailingEps | 4.890000 |

| forwardEps | 9.072260 |

BIOCON's forward EPS surpassing its trailing EPS signals that the company is anticipated to be more profitable this year than last. This growth expectation highlights BIOCON's potential for increased earnings and a stronger financial performance in the upcoming year.

Price projections:

BIOCON's price has continuously remained near the lower end of analysts' projections, indicating that it may be facing challenges in meeting market expectations. This trend raises concerns about the company's future growth trajectory.

Recommendation changes over time:

Analysts have maintained a buy bias for BIOCON, which could prompt investors to consider the stock as a viable investment. With this positive outlook, BIOCON is positioned as an attractive option for those looking to park their money in a stable and potentially lucrative company.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

From Lifesaving Drugs to Sick Units: The Hidden Energy Crisis Inside India’s Pharma Clusters

From Price Pressures to Profit Power: The MSME Playbook Redefining India’s Economy

₹90 Crore Bet Signals a Massive Shift in India’s Rural Economy